The IMF reports the most authoritative currency allocation of global reserves at the end of every quarter with a quarter delay. Invariably, an economist, strategist, or journalist is inspired to write why some data nugget confirms the demise of the dollar as the dominant currency. Given the unorthodox US President, his criticism of Fed policy, and desire for a weaker dollar, the protectionism, and trillion-dollar deficits, many may be predisposed to see a loss of prestige and status. Alas, the IMF’s COFER data provides no such evidence. Let’s begin at the highest level and drill down. The first thing to note is that the reserve assets at reported in US dollars and the movement of exchange rates often as a significant

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, AUD, CAD, COFER, EUR, Featured, GBP, JPY, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The IMF reports the most authoritative currency allocation of global reserves at the end of every quarter with a quarter delay. Invariably, an economist, strategist, or journalist is inspired to write why some data nugget confirms the demise of the dollar as the dominant currency. Given the unorthodox US President, his criticism of Fed policy, and desire for a weaker dollar, the protectionism, and trillion-dollar deficits, many may be predisposed to see a loss of prestige and status. Alas, the IMF’s COFER data provides no such evidence.

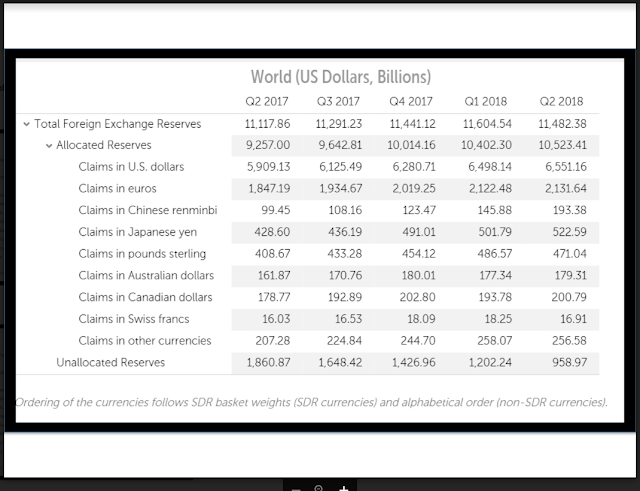

Let’s begin at the highest level and drill down. The first thing to note is that the reserve assets at reported in US dollars and the movement of exchange rates often as a significant impact. Overall, the value of reserves was estimated at $11.482 trillion at the end of Q2. That was a decline of $122.2 bln. Some emerging market countries experiencing downside pressure on their currencies may have intervened and experienced a decline in reserves. However, the dollar rose against all reserve currencies in Q2 (GBP -5.8%, CNY -5.2%, Euro -5%, JPY -4%, AUD -3.6%, and CAD -1.8%) and the valuation rather than quantities seems a more compelling explanation. The IMF has two broad categories of reserves: allocated and unallocated. Not all central banks report their allocation to the IMF. Some regard this as a national secret. Other central banks are fairly transparent. One of the under-reported developments has been the dramatic decline in unallocated reserves. Consider that as of Q5 15, unallocated reserves were $4.1 trillion, roughly 40% of the overall reserves (~$10.92 trillion). By Q2 18, the unallocated reserves had fallen to $960 bln or less than 8.5% of overall reserves ($11.48 trillion). |

US Dollars in Billions, Q2 2017 - Q2 2018 - Click to enlarge |

What is happening? China is slowly reporting the allocation of its reserves as it adopts IMF best practices, perhaps linked to the Q4 2016 decision to include the yuan in the SDR and for the COFER data to break out the use of the yuan as a reserve asset. Previously, the yuan was included with the “other currencies.” Consider that PBOC reserves were reported at $3.33 trillion at the end of 2015. The dollar value of unallocated reserves has fallen by about $3.1 trillion. This suggests that Chinese reserves have nearly been fully allocated.

The US dollar’s share of global allocated reserves had fallen steadily since the end of 2016 when it was 65.4% to 62.25% at the end of Q2 18. This does not reflect that the dollar has been shunned. To the contrary, since the end of 2016, dollar holdings have increased by a little more than $1 trillion. In Q2, when allocated reserves rose by $121.1 bln (even though overall reserves fell), the dollar in reserves rose by $53 bln.

Observers often seem to exaggerate small movement in currency shares to draw some grand conclusion. The real take away ought to be the stability of the dollar’s and euro’s share at a little more than 60% and around 20% respectively. There is some variability among the currencies that account for the residual.

One of the notable developments has been the increase in the yuan as a reserve currency. When the IMF first introduced it in the COFER data, it accounted for 1.08% of allocated reserves of $93 bln. In Q2 18, the yuan’s share had increased to 1.84% or $193.4 bln. Of the $121 bln increase in allocated reserves in Q2 18, the yuan accounted for $47.5 bln. Its share surpassed the Australian dollar’s (1.70%) for the first time and is set to overtake the Canadian dollar (1.91%).

The yen’s share of allocated reserves has increased from 3.83% in Q1 15 to 4.97% in Q2 18. This likely partly reflects that the PBOC had more yen in reserves than other countries on average. Another consideration is the Swiss National Bank, which accumulated several hundred billion dollars in reserves and publishes that it keeps 8% in yen.

The yen’s share has eclipsed sterling’s share which has edged to 4.53% in Q2 18 from 3.83% in Q1 15. Sterling’s share is virtually flat since mid-2016 when the UK voted to leave the EU in a referendum. Central banks have not diversified as much as some had expected into the Australian and Canadian dollars. Their shares hover around 1.70%-2.0%.

The dollar valuation of all the reserve currencies rose between Q1 15 and Q2 18. The exception to this generalization is the Swiss franc. At the end of Q1 15, the dollar value of franc reserves was $17.77 bln. At the end of Q2 18, the dollar value was $16.91 bln. This probably reflects valuation adjustment over the period rather than a change in quantities.

Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,COFER,Featured,newsletter