You would never have guessed it reading many of the op-eds and pundits pronouncing the end to globalization or the West, or liberalism. Global equities have rallied. Of course, stock prices are not the end all and be all, but it stands in stark contrast to the cries that the sky is falling. The MSCI World Index of developed markets advanced for the second consecutive week adding 2.2%. The US S&P 500 moved above 2800 to reach a five-month high, and the NASDAQ 100 is at record highs. The MSCI Emerging Market Index snapped a four-week slide and to close 1.3% higher. China’s Shanghai Composite ended a seven-week, almost 15% drop with its biggest advance in two years (3%). Some investors see the tariffs and the yen and

Topics:

Marc Chandler considers the following as important: 4) FX Trends, Bank of England, Brexit, China, Featured, Japan, newslettersent, trade, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

You would never have guessed it reading many of the op-eds and pundits pronouncing the end to globalization or the West, or liberalism. Global equities have rallied. Of course, stock prices are not the end all and be all, but it stands in stark contrast to the cries that the sky is falling.

The MSCI World Index of developed markets advanced for the second consecutive week adding 2.2%. The US S&P 500 moved above 2800 to reach a five-month high, and the NASDAQ 100 is at record highs. The MSCI Emerging Market Index snapped a four-week slide and to close 1.3% higher. China’s Shanghai Composite ended a seven-week, almost 15% drop with its biggest advance in two years (3%).

Some investors see the tariffs and the yen and Swiss franc sell-off and want to talk about the loss of safe-haven status. Leaving aside the possibility of the US auto tariffs on national security grounds, which would be aimed more at Europe, Canada, and Mexico, countries the US used to regard as allies, what is happening is still quite low on an escalation ladder of commercial conflict. A small amount of world trade is being affected. The economic impact is expected to be modest overall.

It will disrupt some commercial relationships and trade patterns, and now Brazil will buy the discounted US soybeans, and China reduced its tariff schedule for several Asian countries covering a wide range of products that have been provided by American producers. Drawing on reports in the press, we have noted that both the US and China have listed as subject to tariffs goods that do not even trade. There is much posturing, but neither side has yet to really hurt the other. Europe, Canada, and Japan seem to be more taken aback that the US would claim that their steel and aluminum, and possibly car exports, were a threat to its national security than the cost of the tariffs themselves.

Many find the trajectory worrisome, but the multilateral system is holding under strain. The US has not pulled out of NATO, the WTO, or NAFTA. The Trump Administration agreed to the IMF’s aid to Argentina and did not appear to demand fresh concessions. That said, anecdotal reports, including by several Fed officials, cautioned that there is already an impact on sentiment that could affect capital investment decisions. Powell’s testimony before Congress in the coming days will cover this, but Fed views have been clear and consistent. Yes, what has been an evolving liberal multilateral order, is being tested, but it is stronger and more resilient than so many of its self-proclaimed friends seem to think. One practical and actionable implication is for investors to focus on the economic fundamentals and value and not be distracted by what is still little more than political theater. Of course, the situation is fluid and could change in either direction.

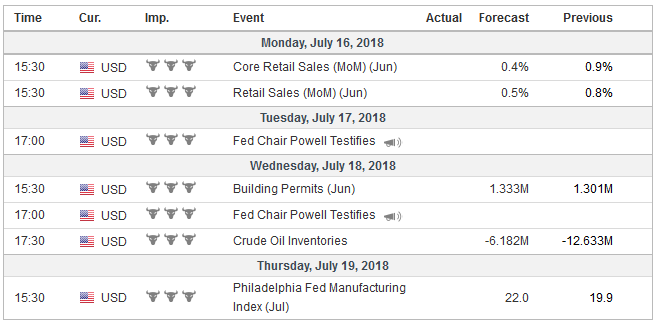

United StatesRather than the end of the world as we know it, investors should be prepared for another batch of strong US economic data next week. Real hourly earnings (year-over-year) ground to a halt in May and June, but be careful about extrapolating this to consumption. Real consumer spending is accelerating this quarter. The personal consumption component of GDP rose 0.9% in Q1 18 and the pace likely more than doubled Q2 despite the slower hourly earnings growth. There are many reasons for a more complicated relationship between real hourly earnings and consumption. For example, real hourly earnings do not capture all job-related income, like commissions and bonuses. There are other sources of income, such as that which accrues sole proprietorships. And we cannot forget credit. Consumer credit, reported last week, jumped $24.5 bln in May, which is largest this year and is the second biggest since the start of last year. The 12-month average stood near $14.2 bln, and the 24-month average was nearly $16 bln, to provide more context. The loose link between real hourly earnings and consumption will likely be borne out in the June retail sales on July 16. Retail sales account for about 40% of personal consumption expenditures and are likely to remain firm (0.4%-0.5%) even if not as strong as May (0.8%-0.9%). The components used for GDP purposes are expected to be up 0.4% after 0.5% in May. If so, it would have the Q2 average is more than twice the Q1 average. Industrial output also likely rebounded after a weak May. Manufacturing had fallen 0.7% in May and is expected to have rebounded nearly fully in June. Industrial production slipped less than 0.1% in May and probably rose 0.5% in June. If so, capacity utilization rates are likely to edge higher to push above 78% for the first time in three years. |

Economic Events: United States, Week July 16 - Click to enlarge |

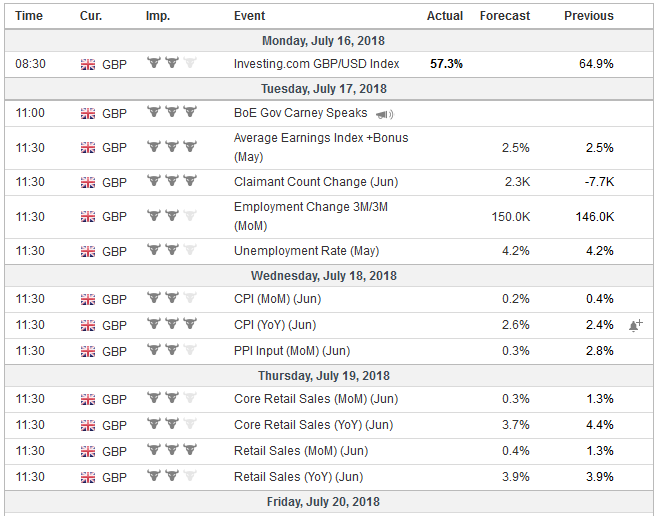

United KingdomUK economic data is also likely to be sufficiently strong to keep investors thinking that this time, at the next meeting in August, Carney and the MPC will deliver the rate hike that has been dangled and withdrawn. We expect next week’s economic data, which may show a tick up in CPI and a better than expected retail sales (thank you World Cup), even if softer the heady 1.3% rise in May. Wage gains may slow a touch, while the unemployment rate may be steady at 4.2%. Outside of the dollar’s general direction, sterling has two main drivers: Brexit developments and monetary policy. In part, given the seeming fragility of May’s hold on power, and a sense that if she is replaced, the next Tory leader is likely to seek a harder Brexit, some European officials appear to be softening their rhetoric. The UK may be forced to make additional compromises, but there may be a subtle change in EC that investors will want to verify. |

Economic Events: United Kingdom, Week July 16 - Click to enlarge |

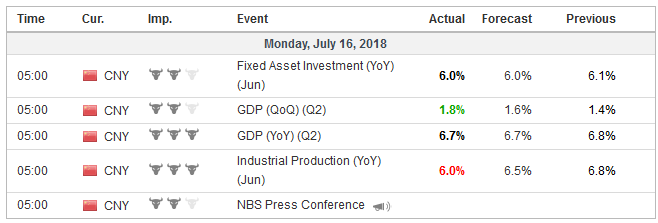

ChinaChina provides fresh insight into its economy. Here two weeks after the end of the quarter, the world’s second-largest economy will provide an estimate of its GDP. Two things can be said about China’s GDP calculation. First, it is broadly in line with other approaches and is consistent with other data, and second, it is amazingly stable. Quarterly growth may have ticked up (1.6% vs. 1.4% in Q1), but the year-over-year pace may slow to 6.7% from 6.8%. Retail sales are expected to have rebounded from the sharp slowdown in May (from 9.4% to 8.5%), while industrial output is expected to have slowed for the second consecutive month (6.5% vs. 6.8%). Fixed investment appears to have slowed for a fourth consecutive month. A 6.0% year-over-year pace would be the lowest since at least 1999 for which data is readily available. Consider that between 2002 and 2013 it never slowed below 20%. |

Economic Events: China, Week July 16 - Click to enlarge |

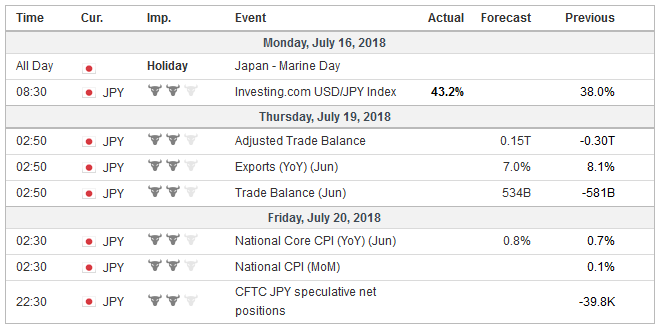

JapanThree reports from Japan that will interest investors. First are the June trade figures. Japanese trade is very seasonal. Almost every June for a couple of decades has seen improvement over May, which typically is worse than April. This year the pattern should hold, which implies a jump back to surplus from deficit. Japan’s export growth is likely to slow, but before seeing the signs of globalization going into reverse, put the say 7.0% year-over-year pace in perspective. Over the past 36 months, average export growth has been 2.6% and 5.4% over the past 24 months. The 12-month average through May of 10.6% is simply unsustainable. Second, Japan reports June CPI figures. The headline rate and the core rate, which excludes fresh food, may have edged higher (to 0.8% from 0.7%) but it is mostly a reflection of energy prices. Excluding energy and fresh food, prices may have risen 0.4% instead of 0.3%. This keeps the BOJ’s extraordinary monetary policy well entrenched. If the weak-yen encouraged gains in the stock market are extended, maybe the BOJ will have less opportunity to buy Japanese equities (mostly on dips in the morning according to media accounts), it could provide the BOJ with cover to slow its equity purchases as it has with its bond-buying program. Third, as we noted last week, Japanese investors have stepped up the pace of exporting their savings. Over the past four weeks, Japan’s purchases of foreign bonds (~JPY2.06 trillion) is the most since last August. Japanese investors have bought more foreign equities (~JPY1.78 trillion) than they have in three years. Weekly MOF data will show whether the trend continued. |

Economic Events: Japan, Week July 16 - Click to enlarge |

With US gasoline prices up more than a quarter over the past year to close in on the psychological $3 a gallon level, there is increased talk that the Trump Administration is considering tapping the Strategic Petroleum Reserves. Around 600 mln barrel of oil is stored in old salt mines. Although ostensibly for emergencies, it has been used to for budget purposes, such as the 11 mln barrel release that Congress has authorized for the beginning of October. It was also used last year in the aftermath of Hurricane Harvey that shut down some refining capacity.

It is clear from Trump’s tweets that the high price of oil and gasoline is on his radar screen. He has harangued OPEC, though the immediate boost to oil prices seems to at least be partly related to geopolitical developments in which the US plays an important role, such as potential loss of Iranian output, the collapse of the Venezuelan economy, and the civil war in Libya. Poor investment decisions, corruption, and other local homegrown problems also bear significant responsibility.

Reports suggest at least three possible strategies are under consideration, but a decision may not imminent. It may take some time for the Administration to conclude that neither OPEC nor non-OPEC countries are going to boost output much more than has already been agreed. That is to say, despite the US encouragement, defections from OPEC/non-OPEC are unlikely. There has been some suggestion that a further 10% rise in oil or gasoline prices could serve as the trigger.

The three strategies include a small token release to send a signal and impact psychology, a larger draw to have a material impact, and an effort coordinated with other countries, as took place most recently during the “Arab Spring” in 2011. The latter may be the most effective and would flummox those that are mourning the passing of globalization. A release of US strategic holdings could also be used to coax other countries into participating in the embargo of Iranian oil starting in early November.

The ultimate impact on oil and gasoline prices depends on size, timing, duration, and a host of imponderables. There is no guarantee that it will have a sustained material impact. Trump had seemed to suggest that the Saudi Arabia’s 2 mln barrel a day spare capacity is sufficient to bring down oil prices. Under those conditions, a release of say 30 mln barrels from the US SPR is two weeks worth of extra supply. That said, the psychological impact could be greater than the material impact.

Tags: #USD,Bank of England,Brexit,China,Featured,Japan,newslettersent,Trade