The weekend strike by the US, British and French forces against Syria appear to have been conducted in ways that minimize the risks of escalation by Russia. The limited nature of the strike and objectives suggest that the impact on the constellation of forces in Syria will be minimal. There is unlikely to be much of an impact in the global capital markets, though thin markets in early Asia could see a knee-jerk effect. The fact that strike took place may lift some uncertainty seen ahead of the weekend. US President Trump warned a strike was coming. The deployment of forces demonstrated the capability. There may be unpredictable asymmetrical responses, but at least initially, investors will look past. Trade tensions

Topics:

Marc Chandler considers the following as important: $INR, 4) FX Trends, CAD, EUR, Featured, GBP, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The weekend strike by the US, British and French forces against Syria appear to have been conducted in ways that minimize the risks of escalation by Russia. The limited nature of the strike and objectives suggest that the impact on the constellation of forces in Syria will be minimal.

There is unlikely to be much of an impact in the global capital markets, though thin markets in early Asia could see a knee-jerk effect. The fact that strike took place may lift some uncertainty seen ahead of the weekend. US President Trump warned a strike was coming. The deployment of forces demonstrated the capability. There may be unpredictable asymmetrical responses, but at least initially, investors will look past.

Trade tensions remain high but have been given a respite. Trump has chosen to hear a conciliatory tone by President Xi last week and went as far as suggesting that perhaps tariffs might not be implemented. NAFTA negotiations are proceeding. Trump also instructed his top economic and trade advisers to look into possibly joining the Trans-Pacific Partnership, which the 11 remaining members signed an agreement last month.

Late Friday the US Treasury issued its biannual report on foreign exchange and international economic policy. No country met the legislative definition of currency manipulation. The Treasury provides a watch-list. In addition to China, Germany, Japan, Korea, and Switzerland, the US added India.

It concerns about India seemed a bit reluctant and largely on strict definitional grounds. India has intervened in the first part of 2017, but not so much in Q4. Still, intervention passed the two percent threshold. India also enjoys a bilateral trade surplus with the US of $23 bln, just above the threshold. The Treasury Department acknowledges that the rupee is not undervalued according to the IMF and that India runs an overall current account deficit of 1.5% of GDP.

There was little acknowledgment in the report that the large fiscal stimulus that is being provided will likely to widen the US external deficit, all else being equal, as it is fond of saying. There is a slight hint of why. Consider that the US recorded a current account deficit of $466 bln in 2017. Yet, the Treasury’s report indicates that the US net international investment position improved by $470 bln. Despite the US living 2.4% beyond its means (investment in excess of savings, which is the current account deficit as a percent of GDP), its net indebtedness to the world fell.

The US Treasury reckons that US investors own $27.6 trillion of foreign assets. Foreign investors own $35.5 trillion of US assets. The net result is that the US owes the world $7.8 trillion. The key to the changing net position is not new flows. The accumulation of past flows swamps the new funds being deployed. Instead, valuation swings, including foreign exchange and stock and bond prices are the drivers.

Investors appear convinced of the outlook for monetary policy for the coming months. The Fed’s balance sheet is shrinking on its pre-determined course, with no perceptible impact, though dealers are absorbing a greater of the new supply at recent auctions. The Fed is committed to hiking rates gradually, and whether there are three hikes or four delivered this year is not such an urgent or critical issue yet. The bias is clear, four hikes are considerably more likely than two, and in our probabilistic world that is important.

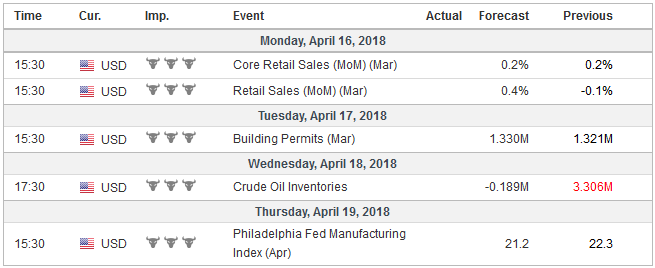

United StatesThe economic confidence expressed in the FOMC minutes will not be deterred by the recent string of data, which prompted the Atlanta Fed GDP tracker to fall to 2.0%. The tax cuts have not spurred stronger consumption growth in Q1, though this week’s March retail sales are likely to have bounced back from three consecutive months of declines. Industrial output likely remained strong, but manufacturing itself is expanding at a somewhat slower pace. |

Economic Events: United States, Week April 16 - Click to enlarge |

EurozoneThe European Central Bank will continue buying 30 bln euros of assets a month through September. Its other policy tools are also open-spigot, which includes a negative 40 bp deposit rate and zero fixed rate refi operations. Over the summer, we expect the ECB to announce that it will further taper its purchase in Q4, completing them by the end of the year. This ostensibly suggests a rate hike is possible toward the middle of 2019, and it would most likely begin by lifting reducing the negative deposit rate. Sufficiently parsed, there does appear to be some upward pressure on eurozone prices, though the final March CPI report in the middle of the week is unlikely to provide much more detail. The poorer than usual winter in Europe may also contribute to some upward pressure on prices, even as it may be partly responsible for some loss of economic momentum in Q1. Some bounce back in Q2 seems likely even if not evident in the April ZEW survey for Germany (Tuesday), though the equity market has rallied nearly 7% from the one-year lows set in late March and a new government is in place. |

Economic Events: Eurozone, Week April 16 - Click to enlarge |

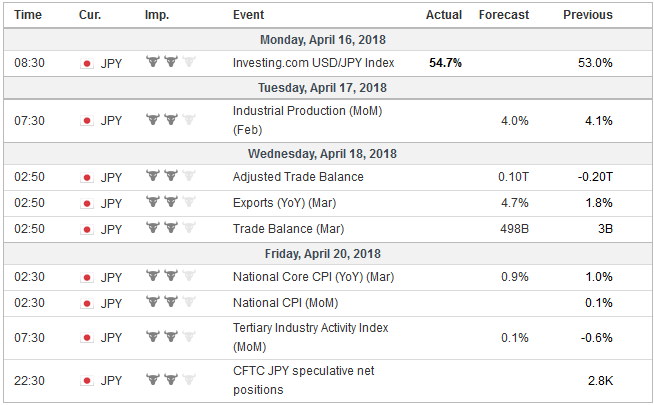

JapanThe Bank of Japan remains on its combined Qualitative and Quantitative Easing (QQE) and Yield Curve Control (YCC) course. Under these initiatives, the BOJ does not have to buy as many government bonds as it did under the pure QQE effort. It continues to buy other assets, including ETFs, where last month’s purchases were a record. Later this month, the BOJ will update its forecasts and include fiscal 2020 for the first time. It must address the economic impact of the sales tax increase that is slated for October 2019. A two percent inflation forecast when the effect of the sales tax is excluded will be understood confirmation of the timing of the BOJ’s exit. While the eurozone economy has lost momentum, the UK has not lost a step. Many question the validity of the Philipps Curve construct, but it appears alive and well in the UK, where wage growth, as investors will be reminded this week, remain firm. Average weekly earnings (excluding bonuses) are expected to have risen 2.8% (three-months year-over-year) in February compared with a 2.0% increase in February 2017. |

Economic Events: Japan, Week April 16 - Click to enlarge |

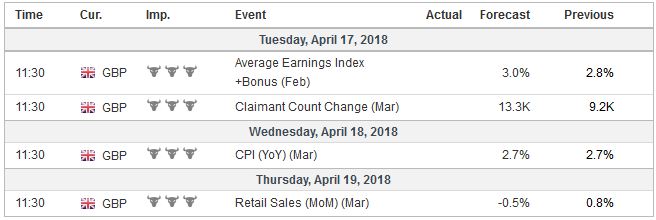

United KingdomThe Bank of England is widely expected to raise interest rates in May. Consumer prices pressures may have peaked last year, but the April 18 March CPI report is expected to underscore their stickiness. It is forecast to be unchanged at 2.7%, which is what it averaged last year. The three-month average in February was 2.9%. The market leans toward a second hike in Q4. On a trade-weighted basis, sterling has appreciated by 3.5% in the last six weeks and now is at its strongest since the referendum. The FTSE 100 is usually sensitive to the exchange rate given the international exposure. However, over the past month, it has outperformed broader measures like the FTSE 250 and 350 (1.40% vs. 0.2% and 1.2% respectively). |

Economic Events: United Kingdom, Week April 16 - Click to enlarge |

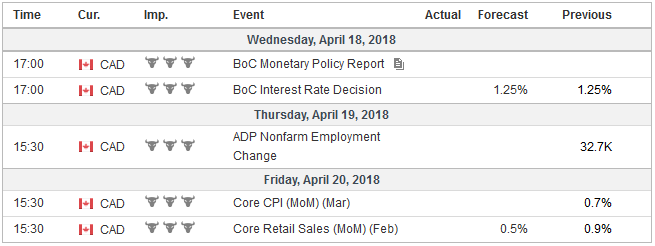

CanadaThe Bank of Canada is the only G10 central bank that has a policy meeting in the week ahead. The uncertainties, largely emanating from the United States, seems to be the major deterrence to a rate hike now. However, the Bank of Canada does want to remove additional accommodation, and a move in Q3 remains a likely scenario. |

Economic Events: Canada, Week April 16 - Click to enlarge |

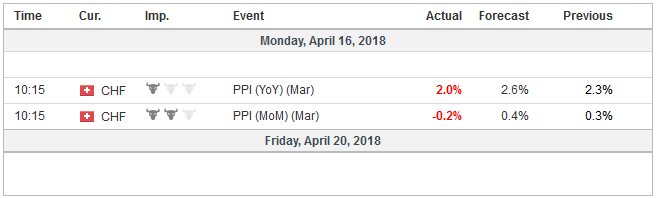

Switzerland |

Economic Events: Switzerland, Week April 16 - Click to enlarge |

Tags: #GBP,#USD,$CAD,$EUR,$INR,Featured,newsletter