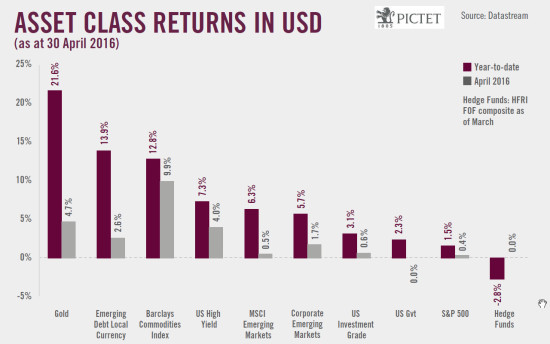

We retain our above-consensus forecast for the euro area this year, but weak first quarter leads to small cut in outlook for the US The conditions that we identified at the start of the year for a market rebound all subsequently fell into place: support from major central banks was forthcoming, the Chinese economy and the oil price stabilised, the US dollar bull trend paused, and systemic risk declined. Valuations have duly recovered. Now, banks need to start performing for markets to have another leg-up. Meanwhile, Brexit remains a major risk. Our central scenario remains unchanged. We continue to believe a serious downturn in the US economy is unlikely this year. However, following the weak Q1 GDP data, we now forecast real GDP growth for the US of 1.8% in 2016 (down from 2% previously). We now expect the Fed to wait until September before raising rates again, and only one rate rise in 2016 (two previously). We maintain our above-consensus forecast for euro area GDP growth in 2016, at 1.8%. However, activity could lose some momentum in the short term while political uncertainty continues to weigh. The ECB’s next meeting in June poses some concerns: markets are pricing in QE beyond 2017, but inflation may pose a risk. Meanwhile, the outcome of the UK’s Brexit referendum on June 23 is highly uncertain. Recent data for China support our forecast for real GDP growth of 6.

Topics:

Perspectives Pictet considers the following as important: Chinese growth, euro growth, growth forecast 2016, Macroview, US growth

This could be interesting, too:

Cesar Perez Ruiz writes Weekly View – Big Splits

Cesar Perez Ruiz writes Weekly View – Central Bank Halloween

Cesar Perez Ruiz writes Weekly View – Widening bottlenecks

Cesar Perez Ruiz writes Weekly View – Debt ceiling deadline postponed

We retain our above-consensus forecast for the euro area this year, but weak first quarter leads to small cut in outlook for the US

The conditions that we identified at the start of the year for a market rebound all subsequently fell into place: support from major central banks was forthcoming, the Chinese economy and the oil price stabilised, the US dollar bull trend paused, and systemic risk declined. Valuations have duly recovered. Now, banks need to start performing for markets to have another leg-up. Meanwhile, Brexit remains a major risk.

Our central scenario remains unchanged. We continue to believe a serious downturn in the US economy is unlikely this year. However, following the weak Q1 GDP data, we now forecast real GDP growth for the US of 1.8% in 2016 (down from 2% previously). We now expect the Fed to wait until September before raising rates again, and only one rate rise in 2016 (two previously).

We maintain our above-consensus forecast for euro area GDP growth in 2016, at 1.8%. However, activity could lose some momentum in the short term while political uncertainty continues to weigh. The ECB’s next meeting in June poses some concerns: markets are pricing in QE beyond 2017, but inflation may pose a risk. Meanwhile, the outcome of the UK’s Brexit referendum on June 23 is highly uncertain.

Recent data for China support our forecast for real GDP growth of 6.5% in 2016 and may even suggest some upside risk. However, the economy’s deep structural problems remain far from resolved, even if good recent headline data mean markets are enjoying a breather from China concerns.