Swiss Economicblogs.org

Swiss Economicblogs.org

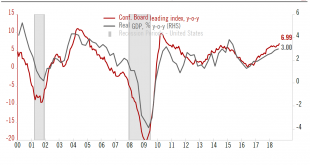

Investment and consumption remain the twin engines of US growth.The first estimate for Q3 GDP (3.5% quarter-on-quarter annualised) confirmed that the US business cycle remains solid. Whereas consumption was stronger than in previous quarters, investment was softer than in Q3—but the underlying story is that solid investment continues to support US growth.This data confirms our annual GDP forecast of 3.0%. This remains above the post-financial crisis average growth rate of 2.3%, and above the...

Read More »US economy continues to chug along, with no slowdown in sight