Frederik Ducrozet and Nadia Gharbi

January 24, 2018

Perspectives Pictet

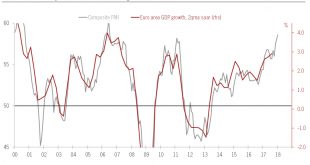

The euro area Flash PMI index surged well above expectations in January. The ECB’s communication could turn more hawkish.The flash composite Purchasing Managers’ index for the euro area increased to 58.6 in January from 58.1 in December, above consensus expectations (57.9). The services sector index rose, offsetting the decline in the manufacturing index . Companies also expressed growing optimism about this year’s outlook, with business expectations up to an eight-month high.The modest...

Read More »

Frederik Ducrozet and Nadia Gharbi

January 19, 2018

Perspectives Pictet

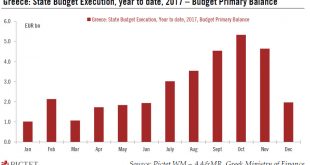

The Eurogroup is set to conclude its third review of Greece’s bailout programme. The country could exit the programme this summer.Eight years after it first requested financial assistance from its European and international partners in April 2010, Greece has never been so close to a ‘clean exit’ from its bailout programme(s). The economy has shown more convincing signs of improvement, with real GDP recovering since mid-2016 and fall in unemployment accelerating in 2017. Macro imbalances have...

Read More »

Frederik Ducrozet

January 19, 2018

Perspectives Pictet

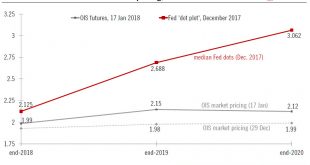

We see little incentive for the ECB to precipitate things at the beginning of the year, especially as core inflation continues to disappoint, but there could be hints at “gradual changes” in forward guidance.We expect no policy decision and no major change in the ECB’s communication at its 25 January meeting. There is no incentive for the ECB to fuel further hawkish market re-pricing at this stage, especially after core inflation disappointed again and the EUR has strengthened once more. The...

Read More »

Perspectives Pictet

January 19, 2018

Perspectives Pictet

[embedded content]

The euro area is benefitting from a very strong momentum at the start of the year, supporting our view that economic growth will remain broadly stable in 2018 at around 2.3%. Risks to this rosy outlook include political events and a more hawkish ECB, although both look very manageable.

Read More »

Perspectives Pictet

January 19, 2018

The euro area is benefitting from a very strong momentum at the start of the year, supporting our view that economic growth will remain broadly stable in 2018 at around 2.3%. Risks to this rosy outlook include political events and a more hawkish ECB, although both look very manageable.

Read More »

Thomas Costerg

January 18, 2018

Perspectives Pictet

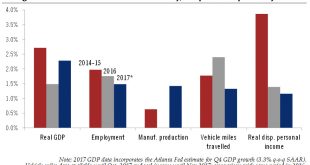

The US economy was not firing on all cylinders in 2017, but this could change with the tax cuts.This is a good time to take stock of how well the US economy did in 2017. Assuming Q4 GDP is in line with the current estimate from the Atlanta Fed (which is close to our own), 2017 growth will be 2.3%. This would mark a step-up from annual growth of 1.5% in 2016 – when the sharp drop in oil prices hit investment and the wider economy hard – but would be close to the growth trajectory seen since...

Read More »

Nadia Gharbi

January 18, 2018

Perspectives Pictet

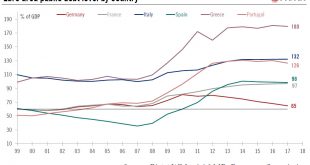

Italian elections are the next big political challenge facing the euro area. While near-term risks seem contained, medium-term ones remain.The Italian government confirmed 4 March as the date for the next parliamentary elections. The lower and upper houses will be elected under a new electoral law, but a hung parliament is the likely initial outcome of the elections given the fragmented political landscape in Italy.However, we do not think that, as things stand, political uncertainty will...

Read More »

Thomas Costerg

January 17, 2018

Perspectives Pictet

With Fed officials becoming more optimistic about the US outlook, there is a risk of additional rate hikes this year. Meanwhile, strategy brainstorming about tweaking inflation targeting continues.A number of Fed officials have given speeches since the beginning of the year, sending mixed messages to markets in the process. Complicating matters, the discussion about the short-term cyclical outlook has become mixed up with an open debate about whether the Fed’s current flexible inflation...

Read More »

Frederik Ducrozet

January 12, 2018

Perspectives Pictet

The outcome of German wage negotiations will have important implications for the broader inflation outlook in the euro area, and thus for ECB policy.German wage negotiations are in full swing amid growing calls for strikes. This comes at a crucial time for the ECB as strong growth and falling unemployment are expected to feed into higher inflation. IG Metall is by far the most important union to watch, representing almost 4 million German workers and being seen as a benchmark, including in...

Read More »

Perspectives Pictet

January 12, 2018

Perspectives Pictet

Pictet Wealth Management's latest positioning across asset classes and invesment themes.Asset AllocationEconomic and earnings growth continue to offer good momentum and the possibility of upside surprises for 2018, so we remain overweight developed market (DM) equities.However, uncertainties over other key aspects of the outlook mean that investors may be unwise to lower their defences. We are keeping tail risk mitigation in portfolios.Emerging market (EM) equities should continue to perform...

Read More »

Perspectives Pictet

Perspectives Pictet