Swiss Economicblogs.org

Swiss Economicblogs.org

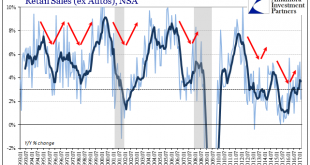

Retail sales comparisons were for February 2017 skewed by the extra day in February 2016. With the leap year February 29th a part of the base effect, the estimated growth rates (NSA) for this February are to some degree better than they appear. Seasonally-adjusted retail sales were in the latest estimates essentially flat when compared to the prior month (January). That leaves too much guesswork to draw any hard...

Read More »Retail Sales: Extra Day Likely, no Meaningful Difference