Jeffrey P. Snider

August 25, 2018

SNB & CHF

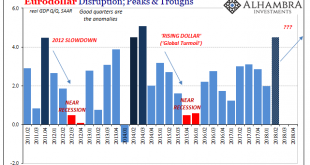

At this particular juncture eight months into 2018, the only thing that will help is abrupt and serious acceleration. On this side of May 29, it is way past time for it to get real. The global economy either synchronizes in a major, unambiguous breakout or markets retrench even more.

That’s been the basis of this thing from Day 1; or, more accurately, Day 3.01. Reflation #3 wasn’t really any different in type from...

Read More »

Jeffrey P. Snider

July 26, 2018

SNB & CHF

In 1999, real GDP growth in the United States was 4.69% (Q4 over Q4). In 1998, it was 4.9989%. These were annual not quarterly rates, meaning that for two years straight GDP expanded by better than 4.5%. Individual quarters within those years obviously varied, but at the end of the day the economy was clearly booming.

It also helped that these particular two years followed two good ones before them. GDP growth in 1997...

Read More »

Jeffrey P. Snider

May 27, 2018

SNB & CHF

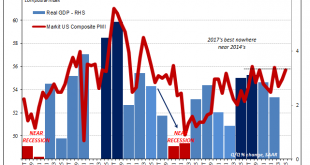

Markit Economics released the flash results from several of its key surveys. Included is manufacturing in Japan (lower), as well as composites (manufacturing plus services) for the United States and Europe. Within the EU, Markit offers details for France and Germany.

Given the nature of sentiment surveys, we tend to ignore these most months unless they suggest either pending changes or extremes.

Beginning with the US,...

Read More »

Jeffrey P. Snider

March 4, 2018

SNB & CHF

Back in October, we noted the likely coming of two important distortions in global economic data. The first was here at home in the form of Mother Nature. The other was over in China where Communist officials were gathering as they always do in their five-year intervals. That meant, potentially:

In the US our economic data for a few months at least will be on shaky ground due to the lingering economic impacts of severe...

Read More »

Jeffrey P. Snider

February 4, 2018

SNB & CHF

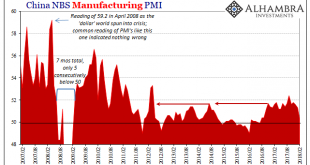

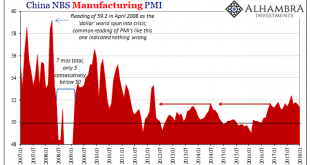

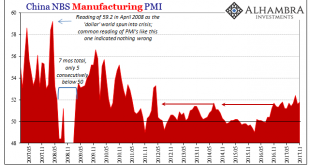

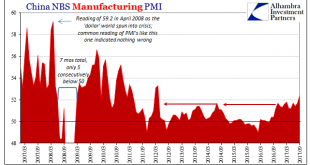

According to China’s official PMI’s, those looking for a boom to begin worldwide in 2018 after it failed to materialize in 2017 are still to be disappointed. If there is going to be globally synchronized growth, it will have to happen without China’s participation in it. Of course, things could change next month or the month after, but this idea has been around for a year and a half already.

Without China, growth won’t...

Read More »

Jeffrey P. Snider

January 25, 2018

SNB & CHF

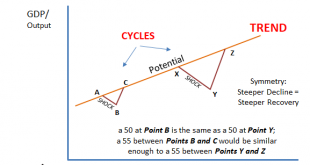

There is a fundamental assumption behind any purchasing manager index, or PMI. These are often but not always normalized to the number 50. That’s done simply for comparison purposes and the ease of understanding in the general public. That level at least in the literature and in theory is supposed to easily and clearly define the difference between growth and contraction.

But is every 50 the same? That’s ultimately at...

Read More »

Jeffrey P. Snider

January 4, 2018

SNB & CHF

While the Western world was off for Christmas and New Year’s, the Chinese appeared to have taken advantage of what was a pretty clear buildup of “dollars” in Hong Kong. Going back to early November, HKD had resumed its downward trend indicative of (strained) funding moving again in that direction (if it was more normal funding, HKD wouldn’t move let alone as much as it has). China’s currency, however, was curiously...

Read More »

Jeffrey P. Snider

December 13, 2017

SNB & CHF

China’s National Bureau of Statistics reported last week that the official manufacturing PMI for that country rose from 51.6 in October to 51.8 in November. Since “analysts” were expecting 51.4 (Reuters poll of Economists) it was taken as a positive sign. The same was largely true for the official non-manufacturing PMI, rising like its counterpart here from 54.3 the month prior to 54.8 last month.

China Manufacturing...

Read More »

Jeffrey P. Snider

November 4, 2017

SNB & CHF

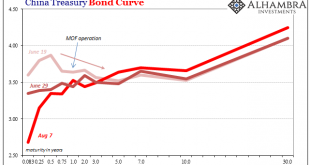

Back in June, China’s federal bond yield curve inverted. Ahead of mid-year bank checks, short-term govvies sold off as longer bonds continued to be bought. It was for some a rotation, for others a reflection of money rates threatening to spiral out of control. On June 19, for example, the 6-month federal security yielded 3.87% compared to a yield of 3.525% for the 10-year.

China Treasury Bonds(see more posts on china...

Read More »

Jeffrey P. Snider

October 14, 2017

SNB & CHF

In the US our economic data for a few months at least will be on shaky ground due to the lingering economic impacts of severe hurricanes. In China, the potential for irregularity is perhaps as great, though it has nothing to do with the weather. In a little over a week, Communist Party officials will gather for their 19th Party Congress.

The temptation may exist to deliver a somewhat better economic picture than has...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org