Jeffrey P. Snider

March 5, 2020

SNB & CHF

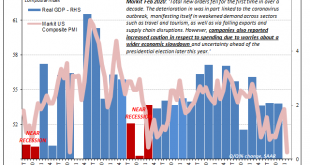

Take your pick, apparently. On the one hand, IHS Markit confirmed its flash estimate for the US economy during February. Late last month the group had reported a sobering guess for current conditions. According to its surveys of both manufacturers and service sector companies, the system stumbled badly last month, the composite PMI tumbling to 49.6 from 53.3 in January.

Today’s update to that flash estimate with more survey responses in hand validated the 49.6....

Read More »

Jeffrey P. Snider

November 9, 2019

SNB & CHF

Note: originally published Friday, Nov 1

There wasn’t much by way of the ISM’s Manufacturing PMI to allay fears of recession. Much like the payroll numbers, an uncolored analysis of them, anyway, there was far more bad than good. For the month of October 2019, the index rose slightly from September’s decade low. At 48.3, it was up just half a point last month from the month prior.

Most of that was related to a curious surge in New Export Orders. Having dropped to...

Read More »

Jeffrey P. Snider

November 7, 2019

SNB & CHF

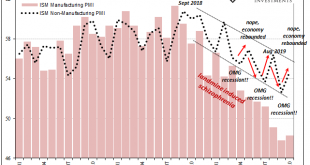

In early September, the Institute for Supply Management (ISM) released figures for its non-manufacturing PMI that calmed nervous markets. A few weeks before anyone would start talking about repo, repo operations, and not-QE asset purchases, recession and slowdown fears were already prevalent. It hadn’t been a very good summer to that end, the promised second half rebound failing to materialize being more and more replaced by central banker backpedaling here as well...

Read More »

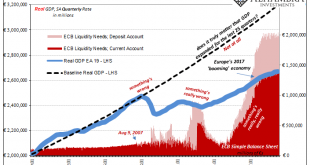

Jeffrey P. Snider

November 3, 2019

SNB & CHF

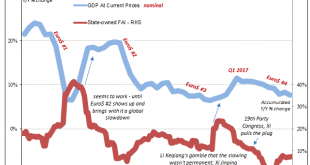

China was the world economy’s best hope in 2017. Like it was the only realistic chance to push out of the post-2008 doldrums, a malaise that has grown increasingly spasmatic and dangerous the longer it goes on. Communist authorities, some of them, anyway, reacted to Euro$ #3’s fallout early on in 2016 by dusting off their Keynes. A stimulus panic that turned out to be more panic than stimulus.

China GDP, 2007-2019(see more posts on China Gross Domestic Product, )...

Read More »

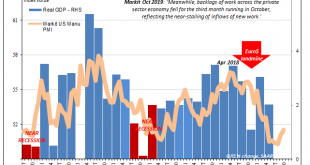

Jeffrey P. Snider

October 25, 2019

SNB & CHF

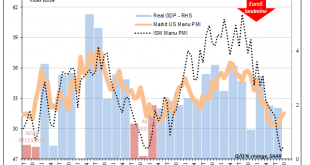

Flash PMI’s from IHS Markit for the US economy were split in October. According to the various sentiment indicators, there’s a little bit of a rebound on the manufacturing side as contrary to the ISM’s estimates for the same sector. Markit reports a sharp uptick in current manufacturing business volumes during this month.

The manufacturing index came in at 51.5, up from a revised reading of 51.1 in September based almost entirely on the production subset. But at the...

Read More »

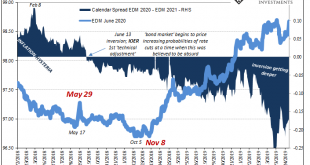

Jeffrey P. Snider

October 5, 2019

SNB & CHF

For the second time this week, the ISM managed to burst the bond bear bubble about there being a bond bubble. Who in their right mind would buy especially UST’s at such low yields when the fiscal situation is already a nightmare and becoming more so? Some will even reference falling bid-to-cover ratios which supposedly suggests an increasing dearth of buyers.

Bid-to-cover, however, is irrelevant. That only tells you about one part of the buying equation, the number...

Read More »

Jeffrey P. Snider

September 24, 2019

SNB & CHF

Mario Draghi can thank Jay Powell at his retirement party. The latter being so inept as to allow federal funds, of all things, to take hold of global financial attention, everyone quickly shifted and forgot what a mess the ECB’s QE restart had been. But it’s not really one or the other, is it? Once it actually finishes, the takeaway from all of September should be the world’s two most important central banks each botching their “accommodations.”

It’s only a little...

Read More »

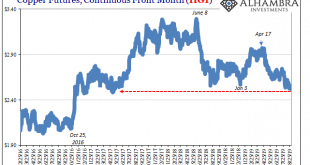

Jeffrey P. Snider

September 4, 2019

SNB & CHF

Copper prices behave more deliberately than perhaps prices in other commodity markets. Like gold, it is still set by a mix of economic (meaning physical) and financial (meaning collateral and financing). Unlike gold, there doesn’t seem to be any rush to get to wherever the commodity market is going. Over the last several years, it has been more long periods of sideways.

That’s what makes any potential breakout noteworthy. Dr. Copper’s place in the hierarchy is...

Read More »

Jeffrey P. Snider

July 27, 2019

SNB & CHF

In the official narrative, the economy is robust and resilient. The fundamentals, particularly the labor market, are solid. It’s just that there has arisen an undercurrent or crosscurrent of some other stuff. Central bankers initially pointed the finger at trade wars and the negative “sentiment” it creates across the world but they’ve changed their view somewhat.

A few billion in tariffs, even if we include what is to...

Read More »

Jeffrey P. Snider

July 25, 2019

SNB & CHF

The popular image of the German industrial machine politics is one which has Germany’s massive factories efficiently churning out goods for trade with the South of Europe (Club Med). Because of the common currency, numerous disparities starting with productivity differences had left the South highly indebted to the North just as the Global Financial Crisis would strike.

The aftermath of that crisis, particularly the...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org