Swiss Economicblogs.org

Swiss Economicblogs.org

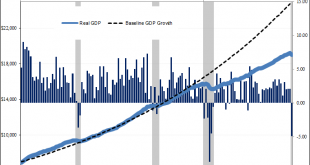

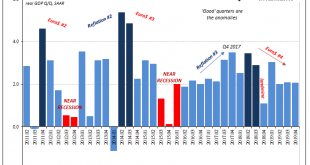

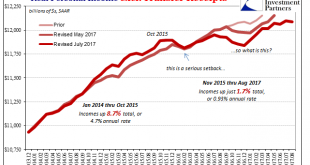

According to today’s advance estimate for first quarter 2022 US real GDP, the third highest (inflation-adjusted) inventory build on record subtracted nearly a point off the quarter-over-quarter annual rate. Yes, you read that right; deducted from growth, as in lowered it. This might seem counterintuitive since by GDP accounting inventory adds to output. It only does so, however, via its own rate of change; the second derivative for specifically the difference....

Read More »Is It Recession?