Swiss Economicblogs.org

Swiss Economicblogs.org

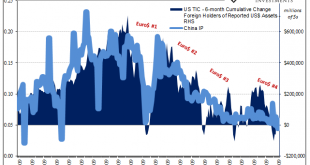

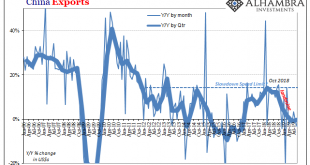

China’s growing troubles go way back long before trade wars ever showed up. It was Euro$ #2 that set this course in motion, and then Euro$ #3 which proved the country’s helplessness. It proved it not just to anyone willing to honestly evaluate the situation, it also established the danger to one key faction of Chinese officials. The entire world slowed in 2012 following #2, but until the bottom of #3 it wasn’t really clear what that might mean. For a very long time,...

Read More »The Dollar-driven Cage Match: Xi vs Li in China With Nowhere Else To Go