Jeffrey P. Snider

September 17, 2019

SNB & CHF

Before the Great “Recession” ended the business cycle as we once knew it, there was a widely accepted concept known as stall speed. In the US, if GDP growth decelerated down to around 2% it suggested the system had reached a danger zone of sorts. In a such a weakened state, one good push, or shock, could send the economy plunging into recession.

Any economy which might slow down into a weakened state for whatever reasons becomes susceptible. What might be a minor,...

Read More »

Jeffrey P. Snider

September 17, 2019

SNB & CHF

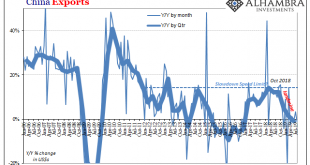

Trade between Asia and Europe has dimmed considerably. We know that from the fact Germany and China are the two countries out of the majors struggling the most right now. As a consequence of the slowing, shipping companies have had to make adjustments to their fleet schedules over and above normal seasonal variances.

It was reported last week that Maersk and MPC would “temporarily suspend” their sailings on one of the biggest routes between Europe and Asia.

Weakening...

Read More »

Jeffrey P. Snider

September 16, 2019

SNB & CHF

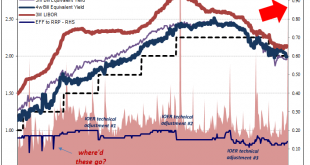

Finally, finally the global bond market stopped going in a straight line. I write often how nothing ever does, but for almost three-quarters of a year the guts of the financial system seemed highly motivated to prove me wrong. Yields plummeted and eurodollar futures prices soared. It is only over the past few weeks that rates have backed up in what has been the first real selloff since last year.

Is this a meaningful change?

It may seem that way in certain places....

Read More »

Jeffrey P. Snider

September 14, 2019

SNB & CHF

The thing about R* is mostly that it doesn’t really make much sense when you stop and think about it; which you aren’t meant to do. It is a reaction to unanticipated reality, a world that has turned out very differently than it “should” have. Central bankers are our best and brightest, allegedly, they certainly feel that way about themselves, yet the evidence is clearly lacking.

When Ben Bernanke wrote for the Washington Post in November 2010 announcing somehow the...

Read More »

Jeffrey P. Snider

September 12, 2019

SNB & CHF

If Mario Draghi wanted to wow them, this wasn’t it. Maybe he couldn’t, handcuffed already by what seems to have been significant dissent in the ranks. And not just the Germans this time. Widespread dissatisfaction with what is now an idea whose time may have finally arrived.

There really isn’t anything to this QE business.

But we already knew that. American officials knew it in June 2003 when the FOMC got together to savage the Bank of Japan for their lack of...

Read More »

Jeffrey P. Snider

September 12, 2019

SNB & CHF

The last time was bad, no getting around it. From the end of 2014 until the first months of 2016, the Chinese economy was in a perilous state. Dramatic weakness had emerged which had seemed impossible to reconcile with conventions about the country. Committed to growth over everything, and I mean everything, China was the one country the world thought it could count on for being immune to the widespread economic sickness.

That’s why in early 2016 authorities...

Read More »

Jeffrey P. Snider

September 11, 2019

SNB & CHF

For every action there is a reaction. Not only is that Sir Isaac Newton’s third law, it’s also a statement about human nature. Unlike physics where causes and effects are near simultaneous, there is a time component to how we interact. In official capacities, even more so.

Bureaucratic inertia means a lot more than just resistance to change, it also means, at times and in certain capacities, all sorts of biases. When the bureaucracy predicts one set of circumstance,...

Read More »

Jeffrey P. Snider

September 9, 2019

SNB & CHF

Give stimulus a chance, that’s the theme being set up for this week. After relentless buying across global bond markets distorting curves, upsetting politicians and the public alike, central bankers have responded en masse. There were more rate cuts around the world in August than there had been at any point since 2009.

And there’s more to come. As Bloomberg reported late last week:

Over the next 12 months, interest-rate swap markets have priced in around 58 more...

Read More »

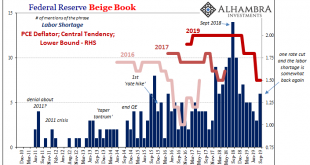

Jeffrey P. Snider

September 7, 2019

SNB & CHF

Federal Reserve policymakers appear to have grown more confident in their more optimistic assessment of the domestic situation. Since cutting the benchmark federal funds range by 25 bps on July 31, in speeches and in other ways Chairman Jay Powell and his group have taken on a more “hawkish” tilt. This isn’t all the way back to last year’s rate hikes, still a pronounced difference from a few months ago.

The common forecast relies entirely on the subjective...

Read More »

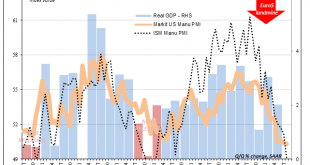

Jeffrey P. Snider

September 5, 2019

SNB & CHF

Bond yields have tumbled this morning, bringing the 10-year US Treasury rate within sight of its record low level. The catalyst appears to have been the ISM’s Manufacturing PMI. Falling below 50, this widely followed economic indicator continues its rapid unwinding.

Back in November 2018, at just about 59 the overall index had still been close to its multi-decade high. Over the next nine months through the latest update for August 2019, it has shed almost 10 points....

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org