Joseph Y. Calhoun

June 21, 2018

SNB & CHF

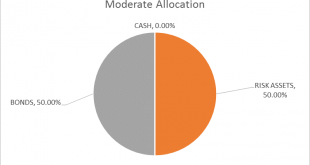

The risk budget is unchanged this month. For the moderate risk investor the allocation to bonds and risk assets is evenly split. There are changes this month within the asset classes.

How far are we from the end of this cycle? When will the next recession arrive and more importantly when will stocks and other markets start to anticipate a slowdown? These are critical questions for investors and ones that can’t be...

Read More »

Jeffrey P. Snider

June 20, 2018

SNB & CHF

US Industrial Production dipped in May 2018. It was the first monthly drop since January. Year-over-year, IP was up just 3.5% from May 2017, down from 3.6% in each of prior three months. The reason for the soft spot was that American industry is being pulled in different directions by the two most important sectors: crude oil and autos.

In the middle is the middling performance of manufacturing especially for consumer...

Read More »

Jeffrey P. Snider

June 16, 2018

SNB & CHF

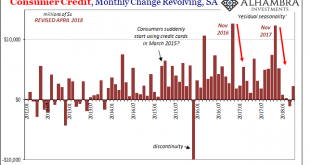

US consumers continue to recover from their debt splurge at the end of last year. Combined with still weaker income growth, the Federal Reserve estimates that aggregate revolving credit balances grew only marginally for the fourth straight month in April 2018. To put it in perspective, the total for revolving credit (seasonally adjusted) is up a mere $2.2 billion for all four months of this year combined, compared to...

Read More »

Jeffrey P. Snider

June 15, 2018

SNB & CHF

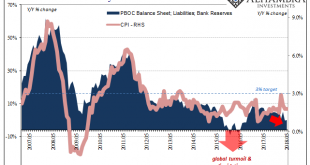

The People’s Bank of China won’t update its balance sheet numbers for May until later this month. Last month, as expected, the Chinese central bank allowed bank reserves to contract for the first time in nearly two years. It is, I believe, all part of the reprioritization of monetary policy goals toward CNY. How well it works in practice remains to be seen.

Authorities are not simply contracting one important form of...

Read More »

Joseph Y. Calhoun

June 14, 2018

SNB & CHF

[embedded content]

Interview with Joe Calhoun about BiWeekly Economic Review 15/06/2018.

Related posts: Bi-Weekly Economic Review: As Good As It Gets?

Bi-Weekly Economic Review – VIDEO

Weekly SNB Intervention Update: SNB Resumes Interventions

Bi-Weekly Economic Review: Oil, Interest Rates & Economic Growth

Bi-Weekly Economic Review

Bi-Weekly...

Read More »

Jeffrey P. Snider

June 13, 2018

SNB & CHF

Whenever a big bank is rumored to be in unexpected merger talks, that’s always a good sign, right? The name Deutsche Bank keeps popping up as it has for several years now, this is merely representative of what’s wrong inside of a global system that can’t ever get fixed. In this one case, we have a couple of perpetuated conventional myths colliding into what is still potentially grave misfortune.

As noted last time, I...

Read More »

Jeffrey P. Snider

June 12, 2018

SNB & CHF

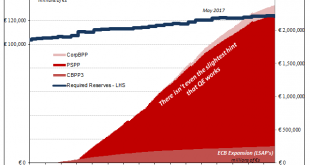

The concept of bank reserves grew from the desire to avoid the periodic bank runs that plagued Western financial systems. As noted in detail starting here, the question had always been how much cash in a vault was enough? Governments around the world decided to impose a minimum requirement, both as a matter of sanctioned safety and also to reassure the public about a particular bank’s status.

Later on, governments...

Read More »

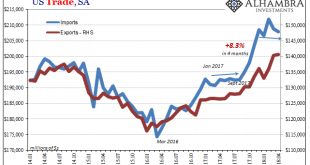

Jeffrey P. Snider

June 8, 2018

SNB & CHF

US trade is further leveling off after several months of artificial intrusions. On the import side, in particular, first was a very large and obvious boost following last year’s big hurricanes along the Gulf Coast. Starting in September 2017, for four months the value of imported goods jumped by an enormous 8.3% (revised, seasonally-adjusted). Most of the bump related to consumer and capital goods.

Since December,...

Read More »

Joseph Y. Calhoun

June 6, 2018

SNB & CHF

In the last update I wondered if growth expectations – and growth – were breaking out to the upside. 10 year Treasury yields were well over the 3% threshold that seemed so ominous and TIPS yields were nearing 1%, a level not seen since early 2011. It looked like we might finally move to a new higher level of growth. Or maybe not.

10 year yields fell nearly 40 basis points in a matter of days as did TIPS yields. The...

Read More »

Marcelo Perez

June 4, 2018

SNB & CHF

[embedded content]

Interview with Joe Calhoun about BiWeekly Economic Review 01/06/2018.

Related posts: The Currency of PMI’s

Why The Last One Still Matters (IP Revisions)

The Dismal Boom

Central Bank Transparency, Or Doing Deliberate Dollar Deals With The Devil

What About 2.62 percent?

More Pieces of Impossible

Not Do We Need One, But Do We Need...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org