Win Thin

May 21, 2018

SNB & CHF

Summary

Bank Indonesia started a tightening cycle with a 25 bp hike to 4.5%.

Jailed Malaysia opposition leader Anwar Ibrahim was released by new Prime Minister Mahathir.

Malaysia scrapped the controversial 6% goods and services tax (GST).

Violent protests shook Israel as the relocated US embassy opened in Jerusalem.

Argentina committed to fiscal tightening as part of a comprehensive IMF program.

Brazil central bank...

Read More »

Jeffrey P. Snider

May 20, 2018

SNB & CHF

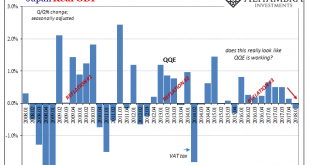

Back in February, Japan’s Cabinet Office reported that Real GDP in Japan had grown in Q4 2017 for the eighth consecutive quarter. It was the longest streak of non-negative GDP since the 1980’s. Predictably, this was hailed as some significant achievement, a true masterstroke of courage and perseverance. It was taken as a sign that Abenomics and QQE was finally working (never mind the four years).

Those making that...

Read More »

Jeffrey P. Snider

May 19, 2018

SNB & CHF

After being rumored and talked about for over a year, at the end of last year the tax cuts were finally delivered. The idea had captured much market attention during that often anxious period of political flirtation. Prices would rise or fall by turn based on whether or not it seemed a realistic possibility.

Public Law #115-97 or An Act to provide for reconciliation pursuant to titles II and V of the concurrent...

Read More »

Charles Hugh Smith

May 18, 2018

SNB & CHF

Healthcare/sickcare will bankrupt the nation by itself.

If you want to understand why the U.S. healthcare system is bankrupt, financially, morally and politically, then start with this representative anecdote from a U.S. physician. I received this report from correspondent J.F. on the topic of direct advertising of pharmaceutical products to the public (patients).

As background information, pharmaceutical companies...

Read More »

Joseph Y. Calhoun

May 17, 2018

SNB & CHF

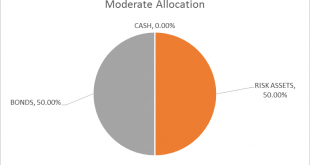

The risk budget changes this month as I add back the 5% cash raised in late October. For the moderate risk investor, the allocation to bonds is still 50% while the risk side now rises to 50% as well. I raised the cash back in late October due to the extreme overbought nature of the stock market and frankly it was a mistake. Stocks went from overbought to more overbought and I missed the rally to all time highs in...

Read More »

Jeffrey P. Snider

May 16, 2018

SNB & CHF

Last year’s infatuation with globally synchronized growth was at least understandable. From a certain, narrow point of view, Europe’s economy had accelerated. So, too, it seemed later in the year for the US economy. The Bank of Japan was actually talking about ending QQE with inflation in sight, and the PBOC was purportedly tightening as China’s economy appeared to many ready for its rebound.

Operating under these...

Read More »

Charles Hugh Smith

May 15, 2018

SNB & CHF

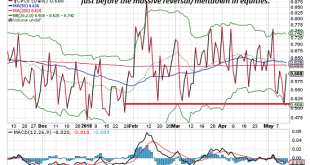

Fortunately for Bulls, none of this matters.

A relatively reliable measure of complacency/euphoria in the stock market just hit levels last seen in late January, just before stocks reversed in a massive meltdown, surprising all the complacent/euphoric Bulls.

The measure is the put-call ratio in equities. Since this time is different, and the market is guaranteed to roar to new all-time highs, we can ignore this (of...

Read More »

Charles Hugh Smith

May 13, 2018

SNB & CHF

How do we explain our obsession with relatively low risk dangers and our collective blindness to manufactured/marketed scourges that kill tens of thousands of people annually?

If you’ve bought a new vehicle recently, you may have noticed some “safety features” that strike many as Nanny State over-reach. You can’t change radio stations, for example, if the vehicle is in reverse. Who knows who or what you’ll run over in...

Read More »

Jeffrey P. Snider

May 12, 2018

SNB & CHF

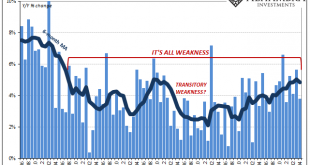

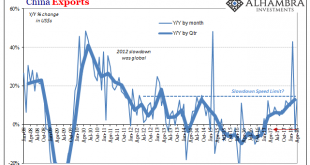

Chinese exports rose 12.9% year-over-year in April 2018.

China Exports, Jan 2008 - Apr 2018(see more posts on China Exports, ) - Click to enlarge

Imports were up 20.9%. As always, both numbers sound impressive but they are far short of rates consistent with a growing global economy. China’s participation in global growth, synchronized or not, is a must.

The lack of acceleration on the export side tells us a lot...

Read More »

Jeffrey P. Snider

May 11, 2018

SNB & CHF

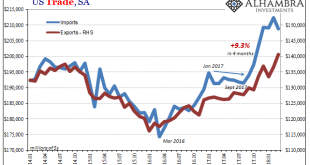

The US trade deficit, a sensitive political topic these days, declined sharply in March. It had expanded significantly (more deficit) in January and February, reaching nearly -$76 billion (seasonally adjusted) in the latter month, before posting -$68 billion in the latest figures. Exports rose while imports fell in March, making for the largest single month change in the trade condition in many years.

That may mean...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org