Joseph Y. Calhoun

August 30, 2019

SNB & CHF

This is a companion piece to last week’s Monthly Macro report found here.

The Treasury market continues to price in lower nominal and real growth. The stress, the urgency, I see in some of these markets is certainly concerning and consistent with what we have seen in the past at the onset of recession. The move in Treasuries is by some measures, as extreme as the fall of 2008 when we were in a full blown panic. That to me, is evidence that this move is overly...

Read More »

Jeffrey P. Snider

August 28, 2019

SNB & CHF

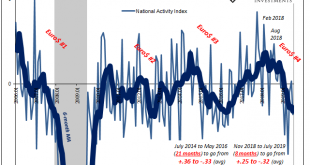

The Chicago Fed’s National Activity Index (NAI) fell to -0.36 in July. That’s down from a +0.10 in June. By itself, the change from positive to negative tells us very little, as does the absolute level below zero. What’s interesting to note about this one measure is the average but more so its rate of change.

The index itself is a product of econometric research. Economists had been searching for an alternative to the unemployment rate in order to increase the...

Read More »

Joseph Y. Calhoun III

August 26, 2019

SNB & CHF

The yield curve’s inverted! The yield curve’s inverted! That was the news I awoke to last Wednesday on CNBC as the 10 year Treasury note yield dipped below the 2 year yield for the first time since 2007. That’s the sign everyone has been waiting for, the definitive recession signal that says get out while the getting is good. And that’s exactly what investors did all day long, the Dow ultimately surrendering 800 points on the day. I don’t remember anyone on CNBC...

Read More »

Jeffrey P. Snider

August 24, 2019

SNB & CHF

The Economics textbook says that when faced with a downturn, the central bank turns to easing and the central government starts borrowing and spending. This combined “stimulus” approach will fill in the troughs without shaving off the peaks; at least according to neo-Keynesian doctrine. The point is to raise what these Economists call aggregate demand.

If everyday folks don’t want to spend – because a lot of them can’t – then the government will spend on their...

Read More »

Jeffrey P. Snider

August 20, 2019

SNB & CHF

The Chinese have been reforming their monetary and credit system for decades. Liberalization has been an overriding goal, seen as necessary to accompany the processes which would keep the country’s economic “miracle” on track. Or get it back on track, as the case may be.

Authorities had traditionally controlled interest rates through various limits and levers. It wasn’t until October 2004, for example, that the upper limit on lending rates was rescinded. In August...

Read More »

Jeffrey P. Snider

August 18, 2019

SNB & CHF

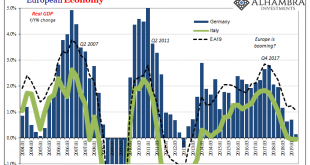

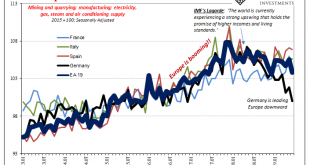

Some further odds and ends of European data. Beginning with Continent-wide Industrial Production. Germany is leading the system lower, but it’s not all just Germany.

And though manufacturing and trade are thought of as secondary issues in today’s services economies, the GDP estimates appear to confirm trade in goods as still an important condition and setting for all the rest.

The weakness is persisting and intensifying – particularly after May 2019.

Europe...

Read More »

Jeffrey P. Snider

August 17, 2019

SNB & CHF

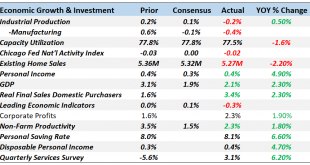

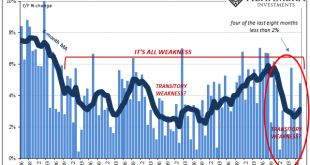

The rules of interpretation that apply to the payroll reports also apply to other data series like retail sales. The monthly changes tend to be noisy. Even during the best of times there might be a month way off trend. On the other end, during the worst of times there will be the stray good month. What matters is the balance continuing in each direction – more of the good vs. more of the bad.

Or when what seems to be a good month is less good than it used to be....

Read More »

Jeffrey P. Snider

August 15, 2019

SNB & CHF

Revised estimates from the Federal Reserve are beginning to suggest another area for concern in the US economy. There hadn’t really been all that much supply side capex activity taking place to begin with. Despite the idea of an economic boom in 2017, businesses across the whole economy just hadn’t been building like there was one nor in anticipation of one.

The only place where there was a truly robust trend was the oil patch. Since the last crash a few years ago,...

Read More »

Jeffrey P. Snider

August 15, 2019

SNB & CHF

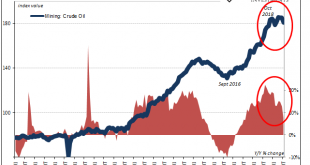

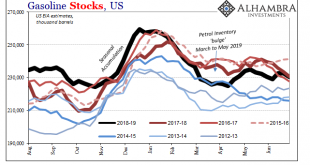

If you like rate cuts and think they are powerful tools to help manage a soft patch, then there was good news in two international oil reports over the last week. The US Energy Information Administration (EIA) cut its forecast for global demand growth for the seventh straight month. On Friday, the International Energy Agency (IEA) downgraded its estimates for the third time in four months.

That wasn’t all, as the EIA’s report focused in on some more sobering aspects...

Read More »

Jeffrey P. Snider

August 14, 2019

SNB & CHF

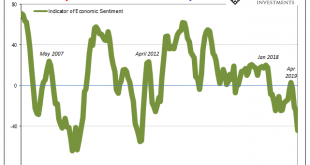

What if Germany’s economy falls into recession? Unlike, say, Argentina, you can’t so easily dismiss German struggles as an exclusive product of German factors. One of the most orderly and efficient systems in Europe and all the world, when Germany begins to struggle it raises immediate questions about everywhere else.

This was the scenario increasingly considered over the second half of 2018 and the first few months of 2019; whether or not recession. Over the past...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org