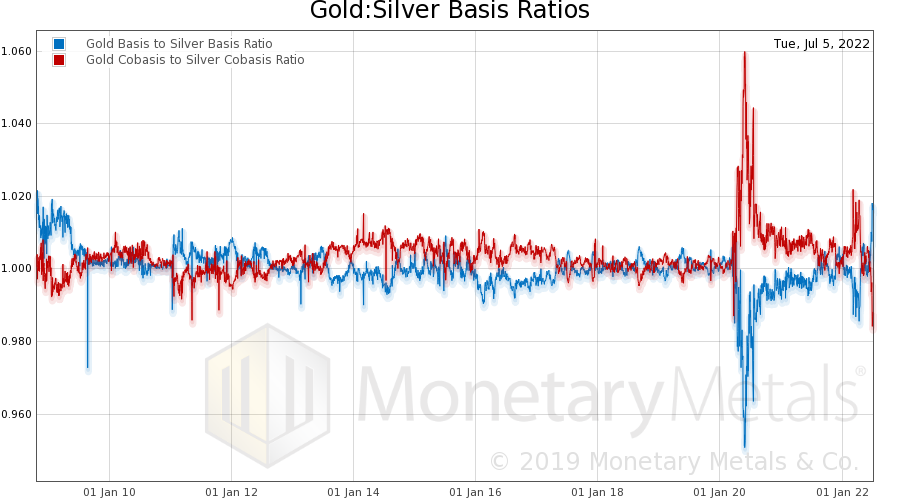

Something has happened which has not occurred since 2009. The silver basis—our measure of abundance of the metal to the market—has gone way under the gold basis. This means silver is less abundant to the market than gold. Here is the picture. The blue line is the ratio of the gold basis to the silver basis (and red is the ratio of the gold cobasis—scarcity—to the silver cobasis). This condition has not occurred in recent years, because the trend has been a rising gold-silver ratio. That is, silver has been generally falling as measured in gold terms. The reason is that there has been no lack of sellers coming to market). Selling physical metal pushes down the bid on the spot price. Cobasis = spot(bid) – future(ask) In other words, selling physical metal tends to

Topics:

Keith Weiner considers the following as important: 6a.) Monetary Metals, 6a) Gold & Monetary Metals, Basic Reports, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Something has happened which has not occurred since 2009. The silver basis—our measure of abundance of the metal to the market—has gone way under the gold basis. This means silver is less abundant to the market than gold. Here is the picture.

The blue line is the ratio of the gold basis to the silver basis (and red is the ratio of the gold cobasis—scarcity—to the silver cobasis). This condition has not occurred in recent years, because the trend has been a rising gold-silver ratio. That is, silver has been generally falling as measured in gold terms. The reason is that there has been no lack of sellers coming to market). Selling physical metal pushes down the bid on the spot price. Cobasis = spot(bid) – future(ask) In other words, selling physical metal tends to push down the cobasis (and push up the basis). Which means that silver, relative to gold, has generally had a higher basis (and when it was lower, it did not go much below gold’s and did not stay there for very long). |

Gold: Silver Basis Ratios |

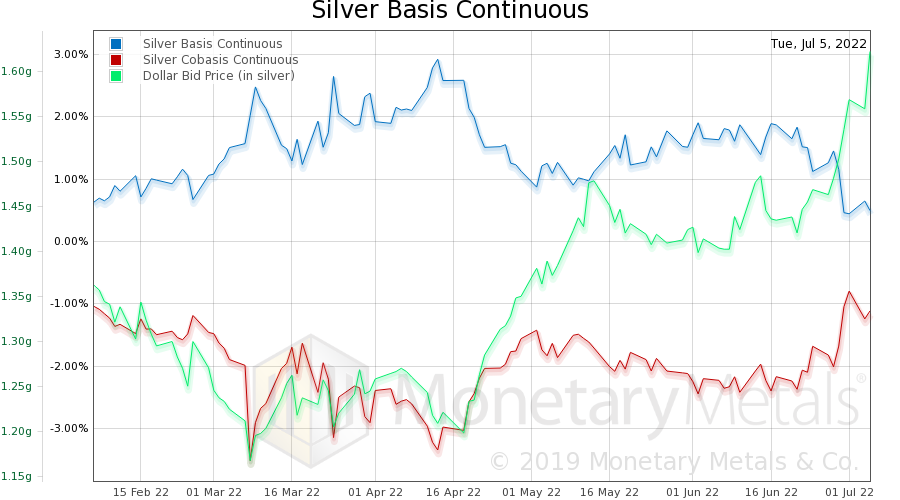

Is This the Moment We’ve Been Waiting For?It is premature to say how durable this is, if silver metal will come to market from private hoards when the price blips up. Or if this is the Moment Everyone Has Been Waiting For™, the final capitulation in the silver price and the start of a multi-year run up in its price. We emphasize that it’s premature to make this call. We want to see how the basis reacts to the next price blip (which seems likely to come here). Does the basis shoot back up to normal? Or does the cobasis stubbornly remain low, and the metal continue to be scarcer than gold, even as its price moves higher relative to gold? Let’s look at a picture of the silver basis by itself. This is the continuous basis, but the September contract is in backwardation (which we strictly define as cobasis > 0, when it’s profitable to de-carry metal, i.e. sell metal and simultaneously buy a futures contract). Backwardation should never occur in a monetary metal. |

Silver Basis Continuous |

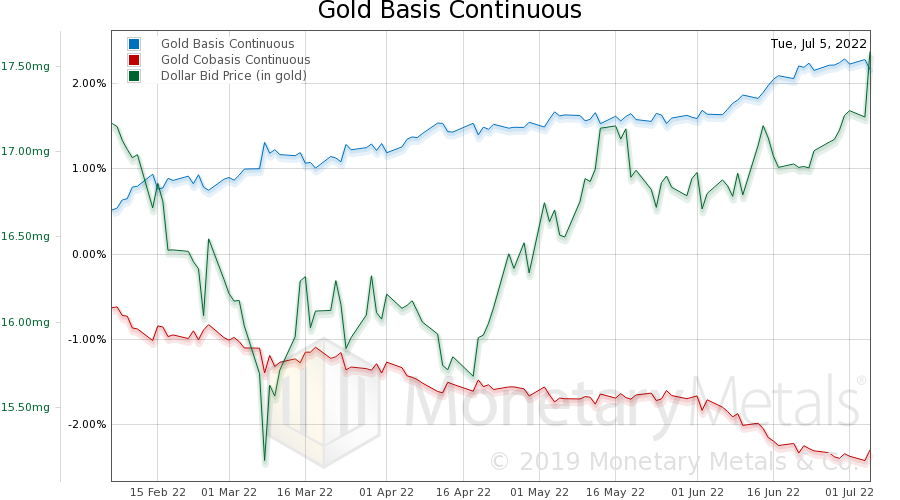

| For comparison, here’s the gold chart.

Note the rising basis, even while the dollar is rising. The basis goes from 1.5% on April 18, to 2.2% on July 5. This occurred when the price of the dollar rose from 15.68 milligrams gold to 17.59mg (that is, the price of gold fell from $1,983 to $1,768, or 10.8%). Gold became more abundant to the market, as its price fell. This is not what most people want to see! During the same period, the price of the dollar in silver terms rose from 1.2 grams to 1.6g (i.e. the price of silver fell from $25.92 to $19.16, or 26.1%). However, the silver basis fell from 2.58% to 0.49%. |

Gold Basis Continuous |

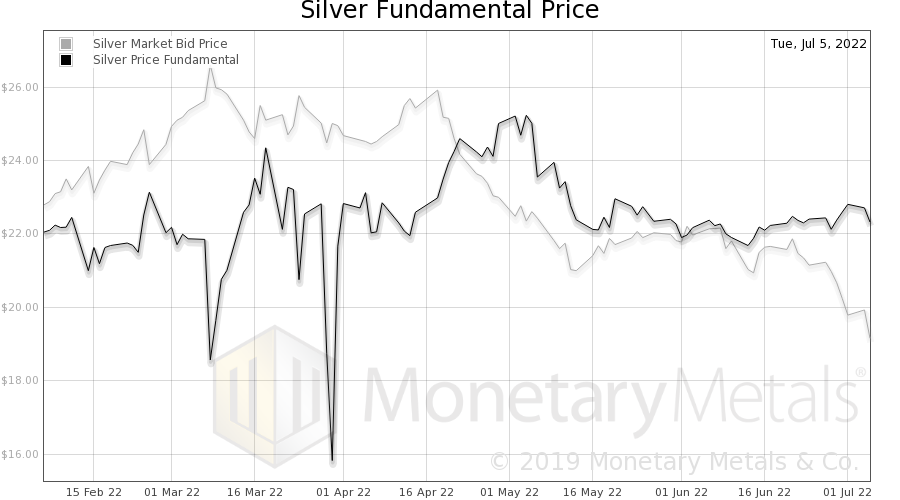

| Next, let’s look at the calculated Monetary Metals silver fundamental price.

The fundamental price is well over $22. Also, notice that it’s not a falling trend. It’s been sideways since well back into 2021. |

Silver Fundamental Price |

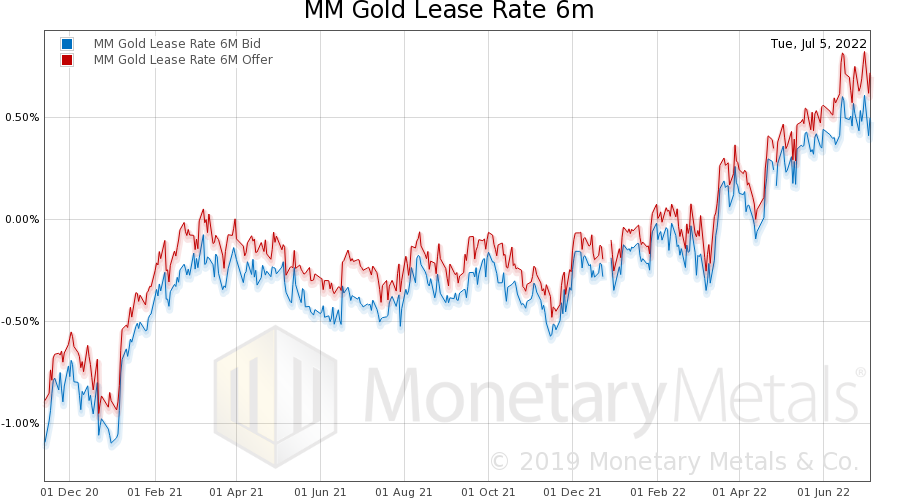

The Silver Squeeze on BusinessesFinally, let’s look at the gold and silver lease rates. The London Bullion Market Association used to provide these, until it ceased publishing due to regulatory compliance costs in 2015. Monetary Metals calculates them from public market data. Our lease rate shows the zero-arbitrage point. In the real world, a bank would charge this rate plus its internal cost of funding, plus its administrative costs, plus its desired profit margin, plus a credit spread. In other words, do not take our rate as an indication of what a real business pays. However, pay attention to the trend. First, here is gold. |

MM Gold Lease Rate 6m |

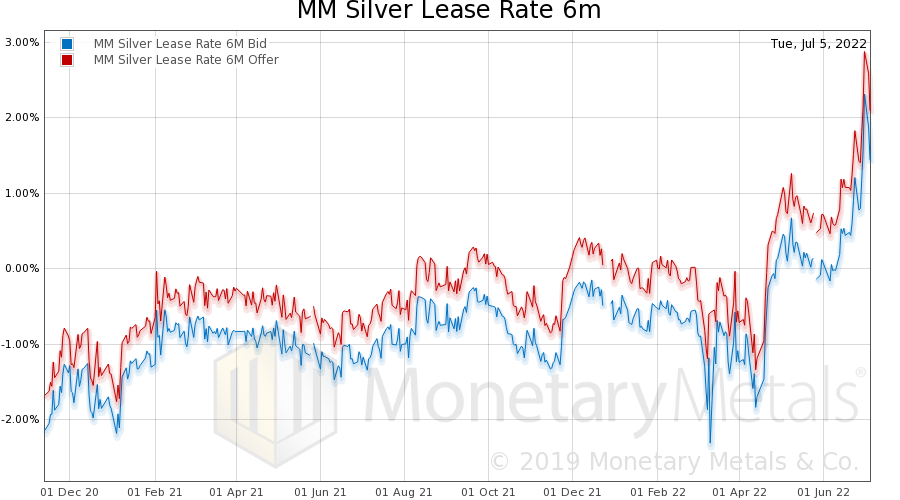

| It’s a rising trend. But this is nothing compared to silver!

Silver is getting downright expensive to lease. |

MM Silver Lease Rate 6m |

Dollar Gyrations vs Metal Leasing

One final word about lease rates. These are based on arbitrage in the dollar markets, and therefore the lease rate moves around based on all sorts of factors in the dollar markets.

Monetary Metals leases metal to businesses who need metal inventory or work-in-progress such as refiners. Since we obtain the metal from investors who own it, these gyrations do not affect us. Our lease rate is stable, which is a win-win for both metal owners and metal-using businesses. In the meantime, we’ll continue to monitor this situation and report on what the data says.

Make sure to Media Appearances, Podcast Episodes and more!

Additional Resources for Earning Interest on Gold

If you’d like to learn more about how to earn interest on gold with Monetary Metals, check out the following resources:

In this paper we look at how conventional gold holdings stack up to Monetary Metals Investments, which offer a Yield on Gold, Paid in Gold®. We compare retail coins, vault storage, the popular ETF – GLD, and mining stocks against Monetary Metals’ True Gold Leases.

The Case for Gold Yield in Investment Portfolios

Adding gold to a diversified portfolio of assets reduces volatility and increases returns. But how much and what about the ongoing costs? What changes when gold pays a yield? This paper answers those questions using data going back to 1972.

You Might Also Like

Will Interest Rate Hikes Fix Inflation?

Will Interest Rate Hikes Fix Inflation?

2022-06-19

Senator Elizabeth Warren and President Joe Biden claim that inflation[i] is caused by greedy corporations. And they propose to solve this problem by making the corporations pay. Whether it’s extracting a “windfall profits” tax, crushing them under even more regulation, or attacking them with antitrust enforcement, the idea is the same.

The Silver Chart THEY Don’t Want You to See!

The Silver Chart THEY Don’t Want You to See!

2022-05-16

On Thursday May 12, the price of silver fell about a buck. As with every one of these big price moves, the question is: what really happened? Below is a chart of the day’s action, with price overlaid with basis. Basis = future – spot. It is a great (i.e. the only) indicator of abundance or scarcity of metal to the market.

Forensic Analysis of Fed Action on Silver Price

Forensic Analysis of Fed Action on Silver Price

2022-05-09

The last few days of trading in silver have been a wild ride.

On Wednesday morning in New York, six hours before the Fed was to announce its interest rate hike, the price of silver began to drop. It went from around $22.65 to a low of $22.25 before recovering about 20 cents.

At 2pm (NY time), the Fed made the announcement. The price had already begun spiking higher for about two minutes.

As an aside, we wonder a bit about how they keep privileged traders from peeking at such announcements before the rest of the world gets to see it. If there was not central planning which ruled our fates with its every edict, this issue would not exist.

Anyways, the price moved up 23 cents by 2:05. It moved sideways waiting for the Fed press conference. Within 11 minutes of the start, the price was

Time for a Silver Trade?

Time for a Silver Trade?

2022-05-04

The price of silver has been going down, and then down some more. From over $28 a year ago, and over $26.50 a month ago, it’s now at a new low under $22.50. Four bucks down in a month.

Oil, the Ruble and Gold Walk into a Bar…Part III

Oil, the Ruble and Gold Walk into a Bar…Part III

2022-04-12

Part III – Gold Standards, the good, the bad, and the ugly. Gresham’s law and gold. Is it even possible to return to a gold standard today? Is Russia leading the push, or do we need something else?

Oil, the Ruble, and Gold Walk into a Bar…

Oil, the Ruble, and Gold Walk into a Bar…

2022-04-05

Part I – Unpacking the narrative of how Russia is going to change the global monetary system. There is a Narrative about Russia and how it will change the monetary system. Many analysts in the gold community are promoting this story. There’s just one problem with this Narrative. It is like how Michael Crighton described the Gell-Mann Amnesia Effect, stating that the newspaper is full of stories explaining how “wet streets cause rain.”

Human Action in the Silver Market

Human Action in the Silver Market

2022-03-29

We have recently seen an increase in social media posts about the big increase in short positions by the bullion banks. What would motivate them to short a commodity during this period of inflation, much less a monetary metal when central banks are printing money with reckless abandon? And doesn’t their shorting of silver push down the price?

This is Not The Silver Breakout You’re Looking For!

This is Not The Silver Breakout You’re Looking For!

2022-03-10

Every once in a while, one regrets not acting sooner, or not acting soon enough. In our case, we did not publish this Tuesday evening. We should have. Today the price is down, and others may also call for lower silver prices.

Tags: Basic Reports,Featured,newsletter