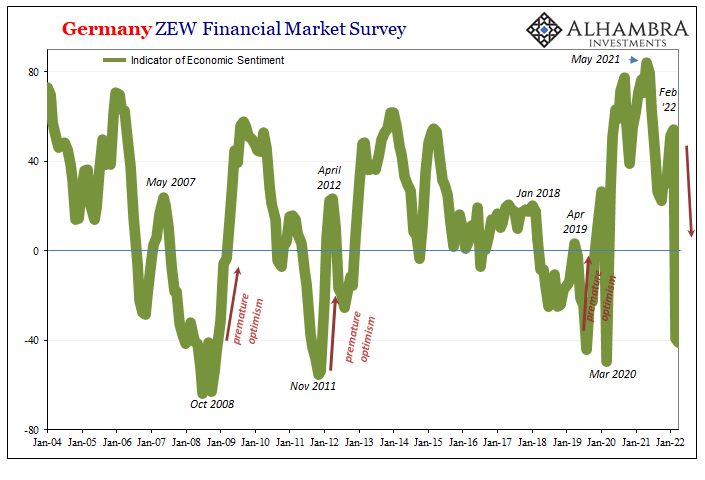

German optimism was predictably, inevitably sent crashing in March and April 2022. According to that country’s ZEW survey, an uptick in general optimism from November 2021 to February 2022 collided with the reality of Russian armored vehicles trying to snake their way down to Kiev. Whereas sentiment had rebounded from an October low of 22.3, blamed on whichever of the coronas, by February the index had moved upward to 54.3. It currently stands at -41.0, collapsing by nearly a hundred in just the two months of Putin’s forced misadventure. . While such reasoning makes sense for sentiment, that the narrative is and will be applied for every ill, now and in the future, for everything wrong in Germany and Europe as a whole requires more consideration. The same

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, currencies, demand destruction, economy, Featured, Federal Reserve/Monetary Policy, Germany, growth scare, inflation, Markets, newsletter, producer prices, sentiment, ZEW

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| German optimism was predictably, inevitably sent crashing in March and April 2022. According to that country’s ZEW survey, an uptick in general optimism from November 2021 to February 2022 collided with the reality of Russian armored vehicles trying to snake their way down to Kiev. Whereas sentiment had rebounded from an October low of 22.3, blamed on whichever of the coronas, by February the index had moved upward to 54.3.

It currently stands at -41.0, collapsing by nearly a hundred in just the two months of Putin’s forced misadventure. |

. |

| While such reasoning makes sense for sentiment, that the narrative is and will be applied for every ill, now and in the future, for everything wrong in Germany and Europe as a whole requires more consideration.

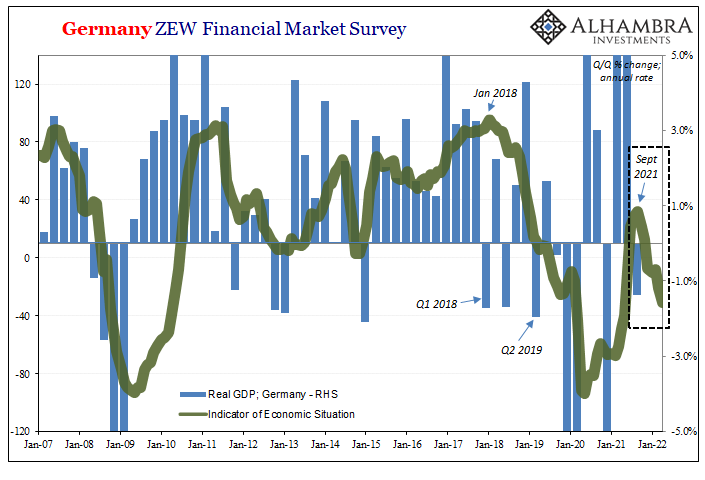

The same survey, ZEW, also tells us something very different when it comes to the German financial and commercial sectors’ assessments of their own current condition. This other index had been going the other way while sentiment had rebounded to finish 2021. In short, though COVID optimism pervaded to end last year and to begin this year before the invasion, it wasn’t being matched by the actual situation. More were telling the group that conditions were declining despite being somewhat happier about the future’s prospects (which, as you can see above, happens quite often). |

. |

| The drop in the situation index long predated the current geopolitical fixation. |

. |

| On the contrary, there is instead a more visible therefore likelier correlation (above).

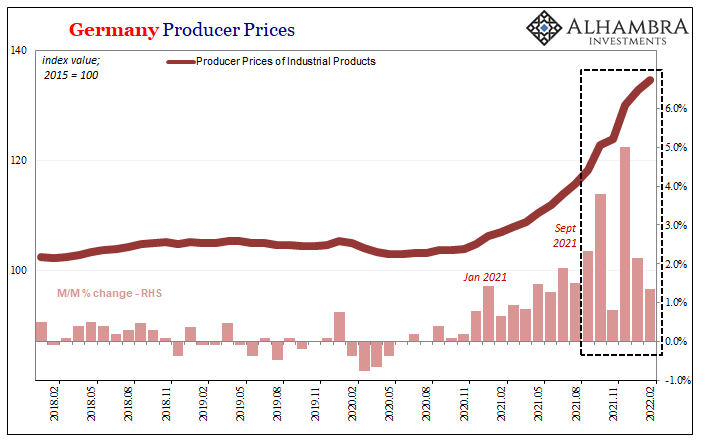

Like practically everywhere else around the world, producer prices in Germany (or Europe) were rising quickly from the beginning of the supply shock. But then around September and October, the pace suddenly and greatly accelerated further. Consumer prices in Europe like America did, too, but not nearly at these ridiculous rates. According to Germany’s deStatis, where the index of industrial prices (PPI) had been increasing at better than 1% monthly rates May through August (inclusive), in September it suddenly skyrocketed to 2.3% m/m and then right after a profoundly harmful 3.8% for October. |

. |

| There would be a small reprieve in November before a truly massive 5.0% m/m increase to close out the year in December. Following this, Germany’s PPI was 25% higher than it had been in December 2020.

That this matches the direction of at least the ZEW’s current situation index may just be random coincidence. It might also represent a powerfully meaningful relationship on the industrial side where fast-rising commodities and input costs put the brakes on whatever non-COVID recovery might have been possible. Producer-side demand destruction? No Russians nor pandemic variants required. Put that together with slowing goods trade in Germany and elsewhere around the world, especially in “real” terms, and you have last year’s now-forgotten “growth scare” showing up “unexpectedly” as this year’s Global Recession Watch. |

. |

Why should anyone outside of Germany or Europe care? Because like last time, 2018’s Euro$ #4, we saw the global macro consequences develop and then spread from there first (along with China and Japan). And the ZEW data was among the earliest warnings (for the entire mainstream to ignore).

By the time the 2s10s UST yield curve inverted in August 2019, the matter had been long before settled:

What if Germany’s economy falls into recession? Unlike, say, Argentina, you can’t so easily dismiss German struggles as an exclusive product of German factors. One of the most orderly and efficient systems in Europe and all the world, when Germany begins to struggle it raises immediate questions about everywhere else.

This was the scenario increasingly considered over the second half of 2018 and the first few months of 2019; whether or not recession. Over the past few months, however, the question has changed again.

It had definitely changed; prior to the middle of ’19, for the Germans the question went from “if” to “how long” and “how deep” at the same time the uncomfortable probabilities of “if” were being applied to more and more other places around the world.

Including, pre-COVID, the United States. He’d never admit it, but Jay Powell’s rate cuts indicate otherwise.

We look at Germany as a very possible and useful window into our own future. That means we can only hope curves are wrong this time, for the first time, and decoupling can actually become something more than just a toss-away word.

You Might Also Like

Concocting Inventory

Concocting Inventory

2022-04-11

The Census Bureau provided some updated inventory estimates about wholesalers, including its annual benchmark revisions. As to the latter, not a whole lot was changed, a small downward revision right around the peak (early 2021) of the supply shock which is consistent with the GDP estimates for when inventory levels were shrinking fast.

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

2022-01-16

How is that US Treasury rates out in the independent longer end of the yield curve have now “suffered” a seven percent CPI to go along with double taper and triple maybe quadruple (if the whispers are to be believed) rate hikes this year, yet have weathered all of that allegedly bond-busting brutality with barely a market fluctuation?

Testing The Supply Chain Inflation Hypothesis The Real Money Way

Testing The Supply Chain Inflation Hypothesis The Real Money Way

2021-12-18

Basic intuition says this is a no-brainer. Producer prices rise, businesses then pass along these higher input costs to their customers in the form of consumer price “inflation” so as to preserve profits. This is the supply chain hypothesis. Statistically, we’d therefore expect the PPI to lead the CPI.And this was expected for much of Economics’ history, taken for granted as one of those self-evident truths (kind of like the Inflation Fairy). After the dreadful experience of the Great Inflation, and the dreadful performance of Economics during it, a few scholars went back to take a second look.One of the most cited contrary studies was published in 1995 by Todd Clark of the Federal Reserve’s branch in Kansas City (Economic Review; vol. 80, issue Q III, 25-39). Using econometric evidence,

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

2021-11-26

When Japan’s Ministry of Trade, Economy, and Industry (METI) reported earlier in November that Japanese Industrial Production (IP) had plunged again during the month of September 2021, it was so easy to just dismiss the decline as a product of delta COVID.

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

2021-11-03

Bring on the tantrum. Forget this prevaricating, we should want and expect interest rates to get on with normalizing. It’s been a long time, verging to the insanity of a decade and a half already that keeps trending more downward through time. What’s the holdup?

Short Run TIPS, LT Flat, Basically Awful Real(ity)

Short Run TIPS, LT Flat, Basically Awful Real(ity)

2021-10-28

Over the past week and a half, Treasury has rolled out the CMB’s (cash management bills; like Treasury bills, special issues not otherwise part of the regular debt rotation) one after another: $60 billion 40-day on the 19th; $60 billion 27-day on the 20th; and $40 billion 48-day just yesterday.

What *Seems* Inflation Now Is Something Else Entirely

What *Seems* Inflation Now Is Something Else Entirely

2021-10-27

This is yet another one of those crucial recent developments which should contribute much clarity about the economic situation, yet is exploited in other ways (political) adding only more to the general state of economic confusion. The shelves may be empty in a lot of places around the country, leaving anyone with the impression there just aren’t enough goods.

An Anti-Inflation Trio From Three Years Ago

An Anti-Inflation Trio From Three Years Ago

2021-10-26

Do the similarities outweigh the differences? We better hope not. There is a lot about 2021 that is shaping up in the same way as 2018 had (with a splash of 2013 thrown in for disgust). Guaranteed inflation, interest rates have nowhere to go but up, and a certified rocking recovery restoring worldwide potential.

Tags: Bonds,currencies,demand destruction,economy,Featured,Federal Reserve/Monetary Policy,Germany,growth scare,inflation,Markets,newsletter,producer prices,sentiment,ZEW