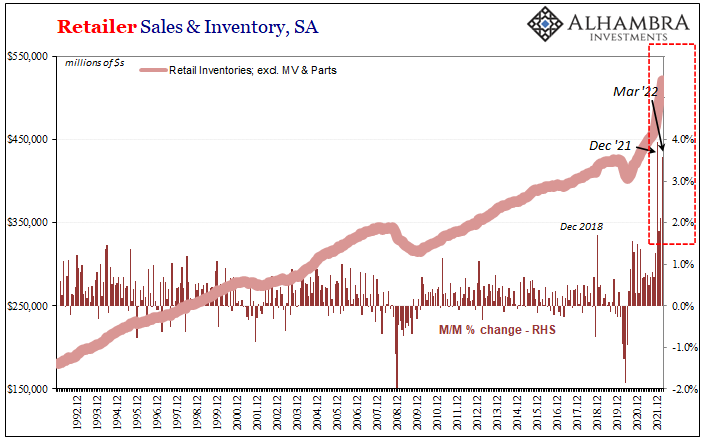

If it continues to play out the same way, it would be all the worst scenarios lumped together all at the same time. A real unfortunate convergence, yet one that has been entirely predictable. Consumers reaching their absolute spending limits. Warehouse and storage capacity nationwide dwindling to long-time lows, leaving firms no options to store inbound goods. And, of course, the stream of goods into inventory that shows no signs (yet) of letting up. Taking the last one first, today the Census Bureau reported its advanced estimates for wholesale and retail inventories. . To start with, the figures for March were already excessive; in retail, the month-over-month change (seasonally-adjusted) had been the second highest on record, behind only December. The

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, economy, Featured, Federal Reserve/Monetary Policy, inflation, Inventory, Markets, newsletter, personal savings rate, real personal income excluding transfer receipts, wholesale inventory

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| If it continues to play out the same way, it would be all the worst scenarios lumped together all at the same time. A real unfortunate convergence, yet one that has been entirely predictable.

Consumers reaching their absolute spending limits. Warehouse and storage capacity nationwide dwindling to long-time lows, leaving firms no options to store inbound goods. And, of course, the stream of goods into inventory that shows no signs (yet) of letting up. Taking the last one first, today the Census Bureau reported its advanced estimates for wholesale and retail inventories. |

. |

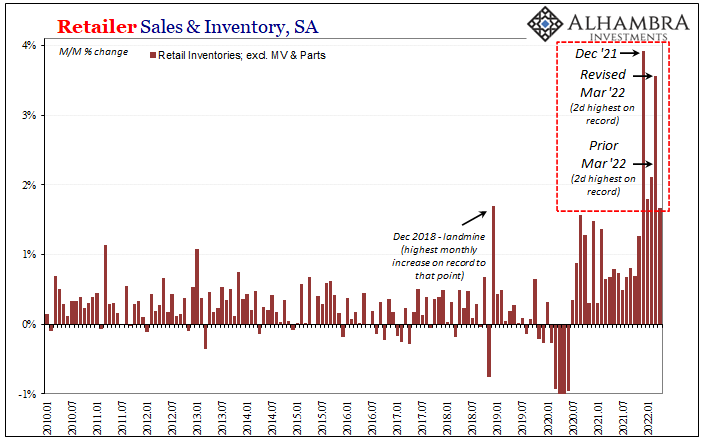

| To start with, the figures for March were already excessive; in retail, the month-over-month change (seasonally-adjusted) had been the second highest on record, behind only December.

The revision for March nearly doubled the monthly rate. |

. |

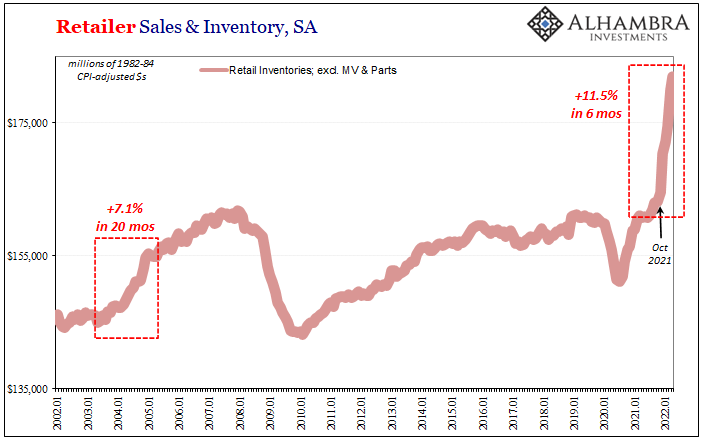

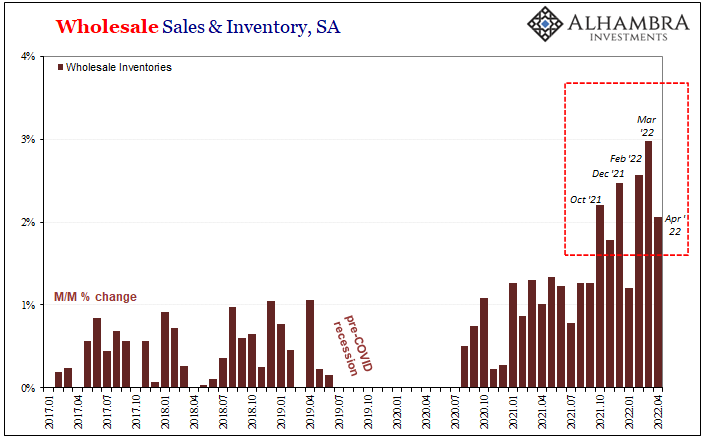

| April’s updated 1.7% would’ve been the second highest on record if it had been April 2021, but now seems small compared these gains since October.And, as noted before, it’s not all due to price effects. Using one form of deflating factor or another, whichever way you account for price changes the result is the same. There is an historic influx of actual goods on top of shipping bills, and it has been nonstop for retailers since October. |

. |

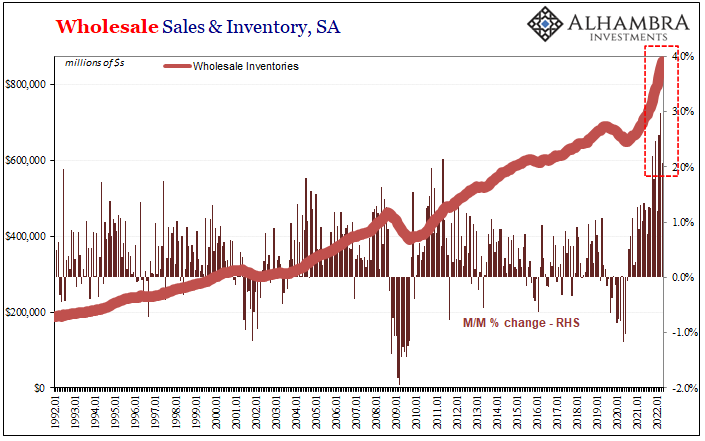

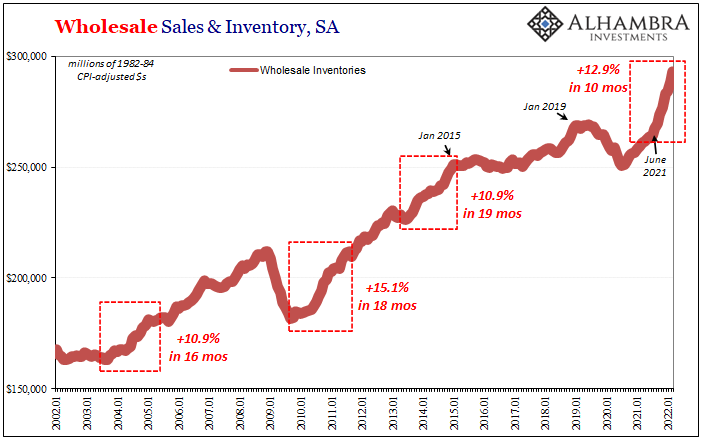

| For wholesalers, the inventory flood goes back a few more months to last July. Like the retail level, wholesale is both real (price adjusted) as well as disproportionate. To put April’s advance estimate into perspective, while it gained 2.1% m/m that’s merely the sixth highest.It also would’ve been second if not for those other recent four months (with March’s figure also revised significantly higher). |

. |

. |

|

. |

|

| So, while goods continue to surge into the US supply chain, more and more it looks like consumers just may have exhausted themselves. Nominal spending is rising, but that’s just the price illusion harmfully redistributing what’s left of the economy after 2020.

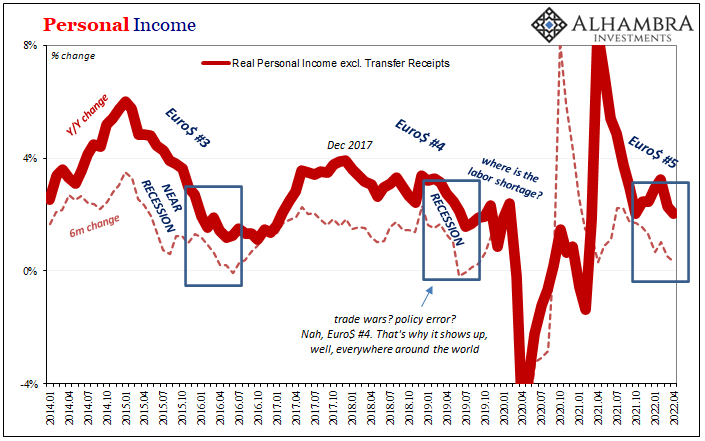

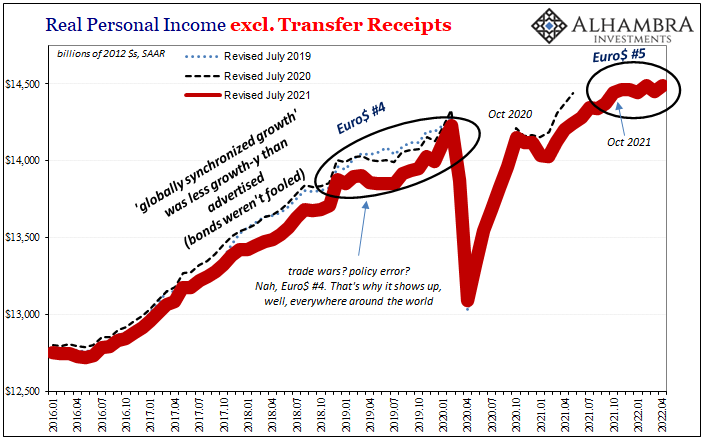

Target and Walmart warnings in mind, now comes the Bureau of Economic Analysis with its personal income and spending data. The key on the income side, Real Personal Income excluding Transfer Receipts, was revised somewhat higher for recent months but still going nowhere. Americans are earning more in their paychecks, collectively among the fewer who are working (compared to 2019), but it’s not keeping up with prices. |

. |

| Earning somewhat more, paying a lot more, all to get slightly less for the round trip. |

. |

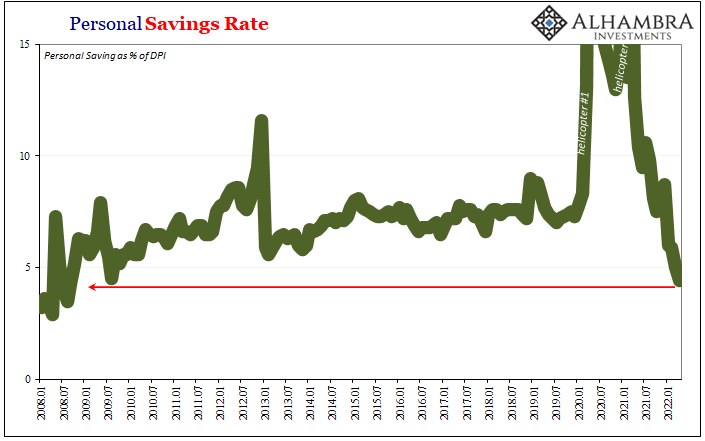

| The most concerning part of today’s BEA release has to be savings; there is not much left to them. The Personal Savings Rate fell to just 4.4%, the lowest since the first part of the Great “Recession.”It’s typical to find a low savings rate associated with the start of any macro contraction phase. The simple reason is there’s nothing left for consumers to support continued spending at the same rates, no margin for any perceived or real error.

The savings rate has tumbled because on the whole consumers/workers are paying more, getting less and not earning enough to make up the difference. Savings at these low levels, it tracks with what Walmart and Target had said last week about consumers trading down to lower cost items as well as scaling back on overall purchases. There was always a limit to last year’s supply shock/helicopter trend, and savings like retailer warnings are a particularly worrisome sign the limit is near. |

. |

All that just in time for the historic flood of inventory, and no room at the warehouse for the weary goods traveled.

While certainly a big problem for the domestic situation, the US consumer has been maybe the lone outlier everywhere in terms of activity over the past year, fourteen months (of data). |

. |

| Shopping online from overseas suppliers, the downside of the inventory cycle just might hit the rest of the global economy that much harder for lack of any momentum or alternative to American (over)buying.

There’s a reason why financial markets have gone curve crazy, several, actually, and this toxic stew of extremes sits (along with collateral scarcity) near the top of every list. And, as I started, it has played out entirely predictably. Rate hikes? Even if they were anything more than symbolic, they’re just not needed. |

. |

. |

You Might Also Like

Some ‘Core’ ‘Inflation’ Difference(s)

Some ‘Core’ ‘Inflation’ Difference(s)

2022-05-06

The FOMC meets next week, with everyone everywhere expecting a 50 bps rate hike to be announced on Wednesday. Yesterday’s “unexpected” and “shocking” negative GDP is unlikely to deter anyone on the committee.

Is It Recession?

Is It Recession?

2022-04-30

According to today’s advance estimate for first quarter 2022 US real GDP, the third highest (inflation-adjusted) inventory build on record subtracted nearly a point off the quarter-over-quarter annual rate. Yes, you read that right; deducted from growth, as in lowered it. This might seem counterintuitive since by GDP accounting inventory adds to output.

Historic Inventory Continued In March, But Is It All Price Illusion, Too?

Historic Inventory Continued In March, But Is It All Price Illusion, Too?

2022-04-28

The Census Bureau today released its advanced estimates for March trade. These include, among other accounts like imports and exports, preliminary results reported by retailers and wholesalers. That means, for our purposes, inventories. Oh my, was there ever more inventory. It was, apparently, widely expected that following an avalanche of goods building up over the previous five months the situation might calm down a touch.

Concocting Inventory

Concocting Inventory

2022-04-11

The Census Bureau provided some updated inventory estimates about wholesalers, including its annual benchmark revisions. As to the latter, not a whole lot was changed, a small downward revision right around the peak (early 2021) of the supply shock which is consistent with the GDP estimates for when inventory levels were shrinking fast.

The Short, Sweet Income Case For Ugly Inversion(s), Too

The Short, Sweet Income Case For Ugly Inversion(s), Too

2022-04-04

A nod to just how backward and upside down the world is now. The economic data everyone is made to pay attention to, payrolls, that one is, in my view, irrelevant. As is the consumer price estimates from earlier this week, the PCE Deflator. That’s another one which receives vast amounts of interest even though it is already old news.

We Can Only Hope For Another (bond) Massacre

We Can Only Hope For Another (bond) Massacre

2022-03-30

To begin with, the economy today is absolutely nothing like it had been almost thirty years ago. That fact in and of itself should end the discussion right here. However, comparisons will be made and it does no harm to review them.I’m talking about 1994, or, more specifically, the eleven months between late February 1994 and early February 1995.

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

FOMC Goes With Unemployment Rate While This Huge Number Happens To Far More Relevant Economic Data

2022-01-29

The first time I can consciously remember using the term landmine was probably here in February 2019. I had described the same process play out several times before, I had just never applied that term. There was all sorts of market chaos in the final two months of 2018, including a full-on stock market correction, believe it or not, leaving the inflation and recovery narrative in near complete tatters.

White-Hot Cycles of Silence

White-Hot Cycles of Silence

2021-12-28

We’re only ever given the two options: the economy is either in recession, or it isn’t. And if “not”, then we’re led to believe it must be in recovery if not outright booming already. These are what Economics says is the business cycle. A full absence of unit roots. No gray areas to explore the sudden arrival of only deeply unsatisfactory “booms.”

Tags: currencies,economy,Featured,Federal Reserve/Monetary Policy,inflation,Inventory,Markets,newsletter,personal savings rate,real personal income excluding transfer receipts,wholesale inventory