A new era of reference interest rates began at the start of this year. Libor, which had been the key reference rate for several decades and several currencies, including the Swiss franc, ceased to exist in many currencies at the end of 2021. SARON has now fully replaced Swiss franc Libor. This speech explains why reference rates play a central role in financial markets and discusses the circumstances under which some interest rates either achieve or lose reference rate status. Following the Global Financial Crisis of 2007 to 2009, Libor increasingly failed to satisfy two important criteria for reference rates – reliability and robustness – and had to be replaced by alternative reference rates. Given the huge importance of reference rates, intensive work was

Topics:

Andréa Maechler considers the following as important: 1.) SNB Press Releases, 1) SNB and CHF, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

A new era of reference interest rates began at the start of this year. Libor, which had been the key reference rate for several decades and several currencies, including the Swiss franc, ceased to exist in many currencies at the end of 2021. SARON has now fully replaced Swiss franc Libor.

This speech explains why reference rates play a central role in financial markets and discusses the circumstances under which some interest rates either achieve or lose reference rate status. Following the Global Financial Crisis of 2007 to 2009, Libor increasingly failed to satisfy two important criteria for reference rates – reliability and robustness – and had to be replaced by alternative reference rates. Given the huge importance of reference rates, intensive work was required to replace Libor.

The switch from Libor to new reference rates entailed far more than just swapping out one rate for another. Market practices had to adjust because the new reference rates differ in important respects from Libor. The speech examines the most important properties of the new reference rates and how they differ from Libor.

Reference rates are also critically important for the transmission of monetary policy. The speech therefore also discusses the adjustment the SNB made to its monetary policy strategy in response to the transition to SARON and the implications for monetary policy implementation.

You Might Also Like

Fritz Zurbrügg: Macroprudential policy beyond the pandemic: Taking stock and looking ahead

Fritz Zurbrügg: Macroprudential policy beyond the pandemic: Taking stock and looking ahead

2022-03-31

In the aftermath of the Global Financial Crisis (GFC), national regulators and international institutions joined forces to build the foundations of our current macroprudential frameworks. These comprise policies aimed at containing the build-up of vulnerabilities to which the banking sector is exposed, and at strengthening banking sector resilience.

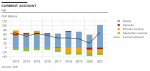

Swiss balance of payments and international investment position: 2021 and Q4 2021

Swiss balance of payments and international investment position: 2021 and Q4 2021

2022-03-22

The current account surplus in 2021 was CHF 69 billion, up CHF 49 billion on the previous year, which was heavily influenced by the coronavirus pandemic. The increase in the current account surplus was almost entirely due to the higher receipts surplus in goods trade (up CHF 45 billion). Here a significantly higher receipts surplus was recorded in both traditional goods trade (foreign trade total 1) and merchanting than in the previous year. Furthermore, there was a reduction in the expenses surplus in non-monetary gold trading.

„Jetzt hilft uns, dass Thomas Jordan ein Falke ist“

„Jetzt hilft uns, dass Thomas Jordan ein Falke ist“

2022-03-20

Der SNB-Chef wurde wegen seiner harten Anti-Inflations-Haltung gescholten, sagt Fabio Canetg, Journalist mit “Geldcast”-Sendung. Nun profitiere die Schweiz davon, weil hier die Preise mit plus 2 Prozent im Vergleich zum Euro-Raum und den USA moderat stiegen. Das wiederum ziehe Vermögen aus dem Ausland an, was den Franken stärke und die Inflation zusätzlich dämpfe.

Swiss National Bank renews its commitment to adhere to the FX Global Code

Swiss National Bank renews its commitment to adhere to the FX Global Code

2022-03-08

The Swiss National Bank (SNB) has renewed the Statement of Commitment to the FX Global Code based on the revised version of the Code dated July 2021. By signing this Statement, the SNB attests that its internal processes are consistent with the principles of the FX Global Code. The SNB also expects its regular counterparties to comply with the agreed rules of conduct.

Swiss National Bank proposes reactivation of sectoral countercyclical capital buffer at 2.5%

2022-01-28

After consultation with the Swiss Financial Market Supervisory Authority (FINMA), the Swiss National Bank has submitted a proposal to the Federal Council requesting that the sectoral countercyclical capital buffer (CCyB) be reactivated. The buffer is to be set at 2.5% of risk-weighted exposures secured by residential property in Switzerland (cf. appendix).

BIS, SNB and SIX successfully test integration of wholesale CBDC settlement with commercial banks

BIS, SNB and SIX successfully test integration of wholesale CBDC settlement with commercial banks

2022-01-13

Project Helvetia looks toward a future with more tokenised financial assets based on distributed ledger technology coexisting with today’s systems.

Swiss National Bank expects annual profit of around CHF 26 billion for 2021

Swiss National Bank expects annual profit of around CHF 26 billion for 2021

2022-01-07

According to provisional calculations, the Swiss National Bank will report a profit in the order of around CHF 26 billion for the 2021 financial year. The profit on foreign currency positions amounted to just under CHF 26 billion. A valuation loss of CHF 0.1 billion was recorded on gold holdings. The net result on Swiss franc positions amounted to over CHF 1 billion.

Swiss balance of payments and international investment position: Q3 2021

Swiss balance of payments and international investment position: Q3 2021

2021-12-22

In the third quarter of 2021, the current account surplus amounted to CHF 24 billion, CHF 10 billion more than in the same quarter of 2020. The increase was mainly attributable to the significantly higher receipts surplus in goods trade. This surplus was due to traditional goods trade (foreign trade total 1), non-monetary gold trading, as well as to merchanting.

Tags: Featured,newsletter