I will begin my remarks with a review of developments on the financial markets over the past half-year. I would then like to discuss the lowering of the threshold factor mentioned by Thomas Jordan. Situation on the financial markets Volatility on the financial markets has increased again significantly since the beginning of the year (cf. chart 1). This was driven by the sharp rise in inflation abroad and by attendant expectations regarding a speedier tightening of monetary policy – especially in the US. Indeed, the Fed has already raised the target range for its federal funds rate in several increments and signalled its intention to increase rates further. In addition, the war in Ukraine and the associated sanctions have exacerbated existing supply bottlenecks

Topics:

Andréa Maechler considers the following as important: 1.) SNB Press Releases, 1) SNB and CHF, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

I will begin my remarks with a review of developments on the financial markets over the past half-year. I would then like to discuss the lowering of the threshold factor mentioned by Thomas Jordan.

Situation on the financial markets

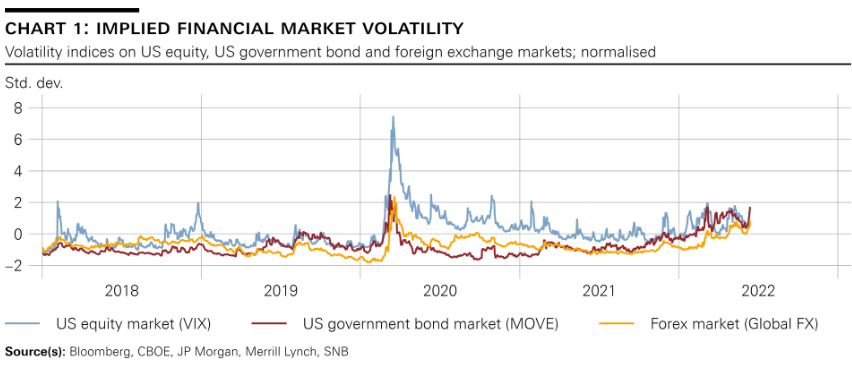

Volatility on the financial markets has increased again significantly since the beginning of the year (cf. chart 1). This was driven by the sharp rise in inflation abroad and by attendant expectations regarding a speedier tightening of monetary policy – especially in the US. Indeed, the Fed has already raised the target range for its federal funds rate in several increments and signalled its intention to increase rates further. In addition, the war in Ukraine and the associated sanctions have exacerbated existing supply bottlenecks and led to surges in energy and commodity prices. These developments have dampened growth expectations and increased uncertainty on the financial markets. |

Global Equity Markets Source: www.snb.ch - Click to enlarge |

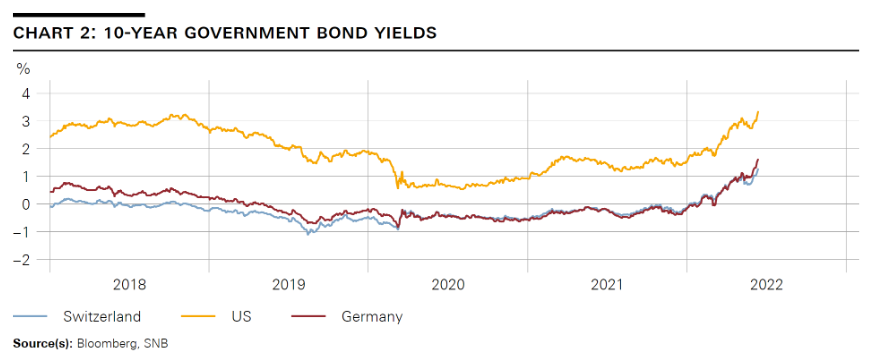

| On the government bond markets, the change in monetary policy direction has had a pronounced impact. In the US, nominal ten-year Treasury yields have risen almost 2 percentage points since the beginning of the year and most recently were standing at well above 3%. Shorter maturities were particularly affected by this revaluation, with a narrowing of yield differentials between long and short maturities. Such a flattening of yield curves is typical in a period of rising inflation and interest rate expectations. In the euro area, the corresponding yields on German government bonds also rose by almost 2 percentage points to about 1.7%. The rise in yields was similar in Switzerland, with ten-year Confederation bonds yielding around 1.3%, their highest level in more than ten years (cf. chart 2). |

10-Year Government Bond Yields Source: www.snb.ch - Click to enlarge |

| In the US, the monetary policy realignment led to a considerable increase in inflation-adjusted bond yields, or real yields. For instance, real yields on ten-year Treasuries have risen by more than 1.5 percentage points since the beginning of the year and are now back at just above 0% for the first time in more than two years. In historical terms, however, this is still very low.

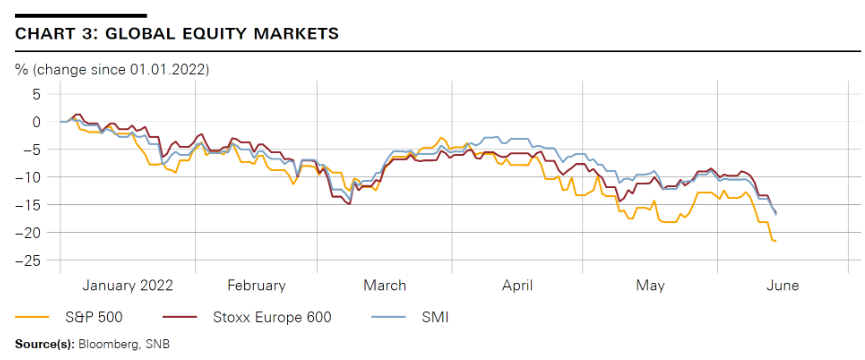

On the stock markets, too, the expectations of a tightening of monetary policy and the heightened uncertainty resulted in price corrections. The leading share indices have recently been trading at well below their levels at the beginning of the year, and the SMI, Switzerland’s leading index, has lost more than 15% over the same period (cf. chart 3). |

Implied Financial Market Volatility Source: www.snb.ch - Click to enlarge |

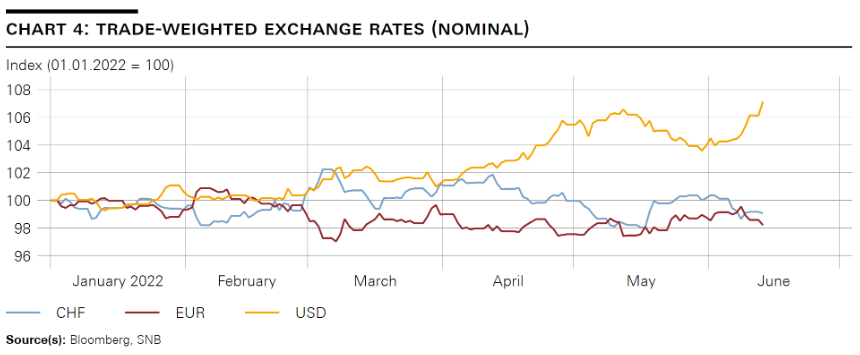

| Foreign exchange markets were likewise heavily shaped by the shift in monetary policy: The US dollar, for instance, has appreciated more than 7% on a trade-weighted basis since the beginning of the year. The trade-weighted euro, on the other hand, has lost around 1.5% and the Japanese yen has actually depreciated by more than 10% on a trade-weighted basis over the same period. The Swiss franc temporarily appreciated immediately following the outbreak of the war in Ukraine. The trade-weighted Swiss franc exchange rate, however, was recently below its level at the beginning of the year (cf. chart 4). |

Trade-weighted Exchange Rates . |

Adjustment of the threshold factor

I would now like to discuss the lowering of the threshold factor from 30 to 28 as mentioned earlier by Thomas Jordan. With this technical adjustment, which will take effect from 1 July 2022, we will ensure that sufficient amounts of sight deposits are subject to negative interest, and that the latter is being passed on to the money market as intended.

From March 2022, upward pressure built up on the short-term rates on the secured money market. This stemmed from the fact that the exemption thresholds had risen over time due to the dynamic calculation model, which meant that there were no longer sufficient amounts of sight deposits subject to negative interest. To keep the secured short-term money market rates close to the SNB policy rate, the SNB provided additional liquidity to the money market via repo transactions as a temporary measure.

However, given that the increase in exemption thresholds is structural in nature, it is appropriate that we lower the threshold factor. This will result in the secured short-term money market rates being close to the SNB policy rate again without the SNB having to regularly provide larger amounts of liquidity.

The SNB will continue to regularly review the basis for calculating the exemption threshold and adjust it as necessary.

You Might Also Like

Тhomas Jordan: Introductory remarks, news conference

Тhomas Jordan: Introductory remarks, news conference

2022-06-16

It is my pleasure to welcome you to the Swiss National Bank’s news conference. In my remarks, I will begin by explaining our monetary policy decision and our assessment of the

economic situation. After that, Fritz Zurbrügg will present the key messages from this year’s Financial Stability Report. Andréa Maechler will then comment on the situation on the

financial markets and the implementation of monetary policy. We will – as ever – be pleased to take your questions afterwards.

Interim results of the Swiss National Bank as at 31 March 2022

Interim results of the Swiss National Bank as at 31 March 2022

2022-05-03

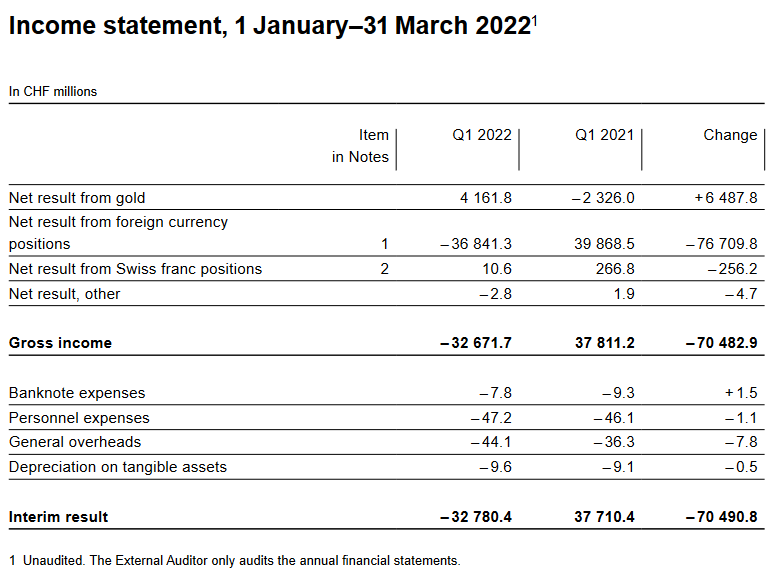

The Swiss National Bank reports a loss of CHF 32.8 billion for the first quarter of 2022. The loss on foreign currency positions amounted to CHF 36.8 billion. A valuation gain of CHF 4.2 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 10.6 million.

Swiss Financial Accounts: Household wealth in 2021

Swiss Financial Accounts: Household wealth in 2021

2022-04-27

The Swiss National Bank is today publishing financial accounts data for Q4 2021. Data on household wealth are thus available for the whole of 2021; a commentary is provided below. This is followed by a detailed look at the development of the financial net worth of the Swiss economy’s institutional sectors since the onset of the coronavirus pandemic.

Macro Week 2022: Thomas Jordan

Macro Week 2022: Thomas Jordan

2022-04-08

At this critical juncture for the global economy and monetary policy, the Peterson Institute for International Economics is convening central bankers and finance officials from around the world for our annual Macro Week—a series of speeches and onstage discussions moderated by PIIE President Adam S. Posen.

Fritz Zurbrügg: Macroprudential policy beyond the pandemic: Taking stock and looking ahead

Fritz Zurbrügg: Macroprudential policy beyond the pandemic: Taking stock and looking ahead

2022-03-31

In the aftermath of the Global Financial Crisis (GFC), national regulators and international institutions joined forces to build the foundations of our current macroprudential frameworks. These comprise policies aimed at containing the build-up of vulnerabilities to which the banking sector is exposed, and at strengthening banking sector resilience.

Swiss balance of payments and international investment position: 2021 and Q4 2021

Swiss balance of payments and international investment position: 2021 and Q4 2021

2022-03-22

The current account surplus in 2021 was CHF 69 billion, up CHF 49 billion on the previous year, which was heavily influenced by the coronavirus pandemic. The increase in the current account surplus was almost entirely due to the higher receipts surplus in goods trade (up CHF 45 billion). Here a significantly higher receipts surplus was recorded in both traditional goods trade (foreign trade total 1) and merchanting than in the previous year. Furthermore, there was a reduction in the expenses surplus in non-monetary gold trading.

Swiss National Bank proposes reactivation of sectoral countercyclical capital buffer at 2.5%

2022-01-28

After consultation with the Swiss Financial Market Supervisory Authority (FINMA), the Swiss National Bank has submitted a proposal to the Federal Council requesting that the sectoral countercyclical capital buffer (CCyB) be reactivated. The buffer is to be set at 2.5% of risk-weighted exposures secured by residential property in Switzerland (cf. appendix).

BIS, SNB and SIX successfully test integration of wholesale CBDC settlement with commercial banks

BIS, SNB and SIX successfully test integration of wholesale CBDC settlement with commercial banks

2022-01-13

Project Helvetia looks toward a future with more tokenised financial assets based on distributed ledger technology coexisting with today’s systems.

Tags: Featured,newsletter