Searching for clues or even small collateral indications, you can’t leave out the gold market. We’ve been on the lookout for scarcity primarily via the T-bill market, and that’s a good place to start, yet looking back to last March the relationship between bills and bullion was uniquely strong. It’s therefore a persuasive pattern if or when it turns up again. To recap the main push of last year’s acute dollar shortage: Over the past several dreadful weeks of liquidations the pattern has largely repeated. During the early morning hours, before regular trading opens, yesterday’s repo transactions are unwound. Under normal and even less-than-ideal conditions these are just rolled over. Not any more. Collateral calls mean in some cases using gold as a last resort

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, Collateral, currencies, economy, Featured, Federal Reserve/Monetary Policy, Gold, Markets, newsletter, nominal yields, real yields, Repo, reverse repo, rrp, T-Bills, TIPS, U.S. Treasuries

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Searching for clues or even small collateral indications, you can’t leave out the gold market. We’ve been on the lookout for scarcity primarily via the T-bill market, and that’s a good place to start, yet looking back to last March the relationship between bills and bullion was uniquely strong. It’s therefore a persuasive pattern if or when it turns up again.

To recap the main push of last year’s acute dollar shortage:

During the early morning hours, before regular trading opens, yesterday’s repo transactions are unwound. Under normal and even less-than-ideal conditions these are just rolled over. Not any more. Collateral calls mean in some cases using gold as a last resort (which gets dumped immediately) and in others the buying of pristine collateral at any price. Gold is slammed while T-bill prices skyrocket, their yields plummet. For those unlucky enough to have neither option in front of them, fire sales of assets including stocks and other risk credits. |

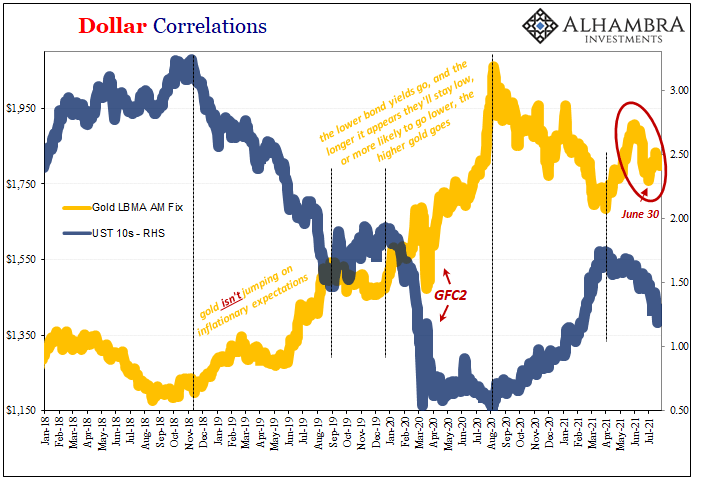

Dollar Correlations, 2018-2021 - Click to enlarge |

| No gold “slams” in 2021, though; not even last Tuesday morning during what had been otherwise a near perfect example of this scramble for collateral (scarcity).

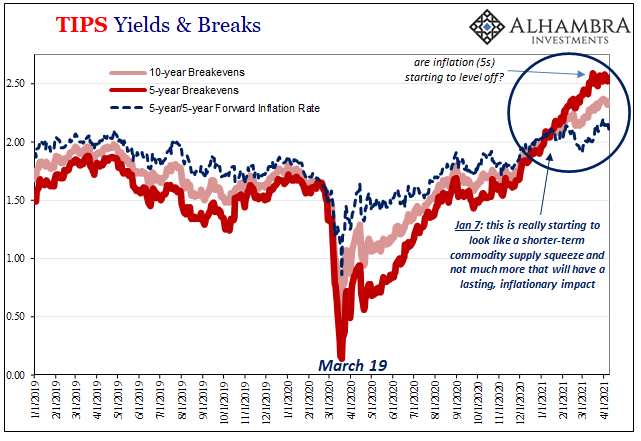

This doesn’t necessarily mean the price behavior in gold has been inconsistent or refuting the notion. On the contrary, there’s been an ongoing modest/mild contraction in it thus possible corroboration worth serious and ongoing attention and analysis. For what I do, I tend to look at gold via its relationship to nominal LT UST yields (since I’m more interested in other factors related to what’s going on in collateral). Many others, especially my colleague Joe Calhoun for more investment-focused considerations (and I encourage you to ask him all about the how’s and why’s), map gold against real yields. They both come up with mostly the same thing, despite some trivial quirks along the way. |

Dollar Correlations, 2018-2021 - Click to enlarge |

| For our purposes here, evaluating the potential for collateral scarcity, as well as attempting to get a sense of its intensity, from late May until June 30 gold moved contrary to LT nominal yields (as well as, to a smaller degree, contrary to real yields).

While there hadn’t been any obvious daily or morning “slams” that matched the price behavior of T-bills, already the five-week downturn in gold was contrary to falling nominals (and real yields sideways to lower in late June). Since gold’s opportunity cost is defined by interest rates, the drop in them and the possibility this signals lower rates farther out into the future, plus the dour outlook in real yields, it really should’ve been a good month of June for the metal. But it wasn’t. Even more compelling still, the recent bottom in gold came in on exactly June 30; the same date I’ve already noted in T-bills (and RRP, of course). From the pricing action in the secondary market, it sure seemed like there was an easing off of collateral pressure (scarcity) beginning right on July 1 (likewise confirmed by less usage of RRP) and lasting through maybe the first half of the month. |

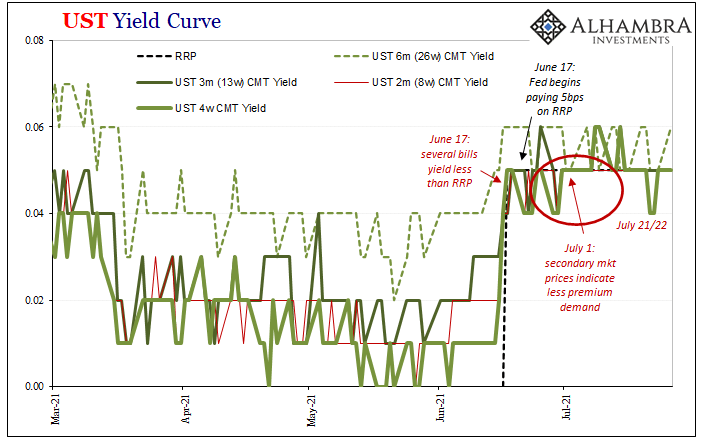

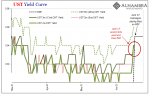

UST Yield Curve, 2021 - Click to enlarge |

| Was the subsequent rebound in gold, beginning on the same day, July 1, another point of collateral corroboration going in the other direction? It just may have been.As might this latest decline in gold; topping out on July 15, we’ve noticed and noted a downward tendency (especially in relation to the RRP “floor”) in bill yields recently, too (obviously including the early AM fireworks last Tuesday) as well as now a rising RRP toward the second half of July.

Nothing conclusive, but a lot that’s compelling because it’s consistent. Therefore, worth keeping an eye on gold for all the usual reasons, relating to real yields and whatnot, but also this keen tendency to second collateral at important times. |

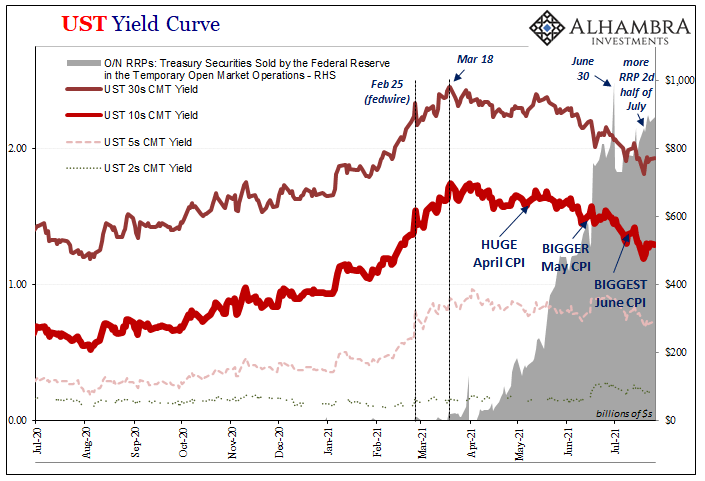

UST Yield Curve, 2020-2021 - Click to enlarge |

You Might Also Like

SNB Sight Deposits: Inflation is there, CHF must Rise

SNB Sight Deposits: Inflation is there, CHF must Rise

2021-07-26

Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

Lower Yields And (fewer) Bills

Lower Yields And (fewer) Bills

2021-07-21

Back on February 23, Federal Reserve Chairman Jay Powell stopped by (in a virtual, Zoom sense) the Senate Banking Committee to testify as required by law. In the Q&A portion, he was asked the following by Montana’s Senator Steve Daines.

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market

And Now Three Huge PPIs Which Still Don’t Matter One Bit In Bond Market

2021-07-15

And just like that, snap of the fingers, it’s gone. Without a “bad” Treasury auction, there was no stopping the bond market today from retracing all of yesterday’s (modest) selloff and then some. This despite the huge CPI estimates released before the prior session’s trading, and now PPI figures that are equally if not more obscene.

RRP No Collateral Coincidences As Bills Quirk, Too

RRP No Collateral Coincidences As Bills Quirk, Too

2021-07-12

So much going on this week in the bond market, it actually overshadowed the ridiculous noise coming from the Fed’s reverse repo. Some maybe too many want to make a huge deal out of this RRP if only because the numbers associated with it have gotten so big.

The FOMC Accidentally Exposes Itself (Reverse Repo-style)

The FOMC Accidentally Exposes Itself (Reverse Repo-style)

2021-06-18

Initially, the dots got all the attention. Though these things are beyond hopeless, the media needs them to write up its account of a more fruitful monetary policy outcome because markets continue to discount that entirely.

Rechecking On Bill And His Newfound Followers

Rechecking On Bill And His Newfound Followers

2021-04-09

The benchmark 10-year US Treasury has obtained some bids. Not long ago the certain harbinger of bond rout doom, the long end maybe has joined the rest of the world in its global pause if somewhat later than it had begun elsewhere (including, importantly, its own TIPS real yield backyard).

Three Things About Today’s UST Sell-off, Beginning With Fedwire

Three Things About Today’s UST Sell-off, Beginning With Fedwire

2021-02-28

Three relatively quick observations surrounding today’s UST selloff.1. The intensity. Reflation is the underlying short run basis, but there is ample reason to suspect quite a bit more than that alone given the unexpected interruption in Fedwire yesterday.

For The Dollar, Not How Much But How Long Therefore How Familiar

For The Dollar, Not How Much But How Long Therefore How Familiar

2021-02-24

Brazil’s stock market was rocked yesterday by politics. The country’s “populist” President, Jair Bolsonaro, said he was going to name an army general who had served with Bolsomito (a nickname given to him by supporters) during that country’s prior military dictatorship as CEO of state-owned oil giant Petróleo Brasileiro SA. Gen. Joaquim Silva e Luna is being installed, allegedly, to facilitate more direct control of the company by the federal government.With the economy still gripped by the latest recession, and oil prices rising worldwide as supplies continue to be squeezed, Brazilians have been caught in the vise between fuel prices and unemployment – pure misery for a nation still reeling from Euro$ #3’s (2014-16) crushing impacts. A depression for years before COVID…and now this.

Tags: Bonds,collateral,currencies,economy,Featured,Federal Reserve/Monetary Policy,Gold,Markets,newsletter,nominal yields,real yields,repo,reverse repo,rrp,T-Bills,TIPS,U.S. Treasuries