Sixty percent equities, 40 percent bonds. What has been considered the golden rule of portfolio theory for decades is of less and less value to investors today. Because central banks have backstopped almost every market, essentially mimicking the market maker of last and first resort, returns have been low, correlations have increased, and valuations are deprived of their meaning. To act as the ultimate market maker as such, central banks have been leveraging up their balance sheets. They have been creating liquidity—mainly in the form of electronic bank reserves—only to mainly swap them for pristine collateral in the form of government bonds. This has several consequences. Good collateral is siphoned off from the markets onto the Federal Reserve’s balance sheet,

Topics:

Pascal Hügli considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Sixty percent equities, 40 percent bonds. What has been considered the golden rule of portfolio theory for decades is of less and less value to investors today. Because central banks have backstopped almost every market, essentially mimicking the market maker of last and first resort, returns have been low, correlations have increased, and valuations are deprived of their meaning.

Sixty percent equities, 40 percent bonds. What has been considered the golden rule of portfolio theory for decades is of less and less value to investors today. Because central banks have backstopped almost every market, essentially mimicking the market maker of last and first resort, returns have been low, correlations have increased, and valuations are deprived of their meaning.

To act as the ultimate market maker as such, central banks have been leveraging up their balance sheets. They have been creating liquidity—mainly in the form of electronic bank reserves—only to mainly swap them for pristine collateral in the form of government bonds. This has several consequences. Good collateral is siphoned off from the markets onto the Federal Reserve’s balance sheet, thereby putting pressure on market actors to find eligible collateral to keep the system’s needed credit creation going. As supply shrinks, demand is relentless.

More Debt, Lower Yield

Furthermore, government debt is effectively being monetized by central banks. In 2020, the Federal Reserve bought 55 percent of all US government securities. Impressive to cringeworthy are the forecasts showing that the European Central Bank is likely to monetize a whopping 98 percent of the entire bond issuance by European sovereigns.

So unprecedented demand from private as well as public actors is pushing down the yields of governments bonds. While the yields of US government bonds are still positive, they are historically low nonetheless. The yield of Germany’s thirty-year bond has traded negatively several times this year. And in Switzerland, all its bonds—including the fifty-year bond—effectively have a negative yield. With yields so low, though, governments are happy to provide the much-needed collateral in exchange for the ability to further go into debt. Consequently, global debt levels have grown to a new all-time high of $296 trillion, driven by record increases in government, household, and corporate debt.

Because of their historically low yield, the bonds of major Western countries increasingly turn into hot potatoes no one is willing to hold for long. Although these “saving instruments” can be used to speculate on short-term price gains resulting from interest rate fluctuations, investors do not want to hold the bond to maturity, as bonds then automatically turn into a losing trade.

When Positive Correlations Are Negative

Falling yields also have a continuous impact on stocks, as they affect discount rates. Lower yields mean lower discount rates, which again means that cash flows are discounted at a lower rate, pushing a stock’s value up. So, if bond prices are driven up because of endless money printing, the latter reverberates through equity markets as well.

With stock as well as bond prices rising more and more in lockstep because of central bank intervention, the correlation between the two has increased over the last few years. To the displeasure of investment managers, in recent periods when markets corrected, the correlation was positive—just when a negative correlation between stocks and bonds would have been most important. As a matter of fact, the rolling correlation over the past three years in the US is close to 0.20 and over one year—the pandemic year, notably—even close to 0.40. In markets such as Switzerland or Japan, equities and bonds have only been slightly negatively correlated.

Back in summer (end of July 2021), the stock-bond correlation rose to a level higher than before the financial crisis of 2008. While historically correlations have been higher, today’s situation is especially precarious because of other strains investors are faced with, like negative interest rates, unprecedented debt levels as well as pressing structural issues like demographics.

A Look beyond Fiat-Denominated Assets

In these times of volatile markets, where everything and everyone is hanging on the lips of the central banks, the question arises: If the traditional portfolio with 60 percent equities and 40 percent bonds has had its day—especially due to increased correlation between equities and bonds—what is the alternative? More than ever, the key seems to be agility and a perspective beyond fiat-denominated assets.

Obviously, investors—especially professional asset managers—won’t be able to avoid the fiat world completely. To some extent, they will need to keep playing the fiat game, which has turned into a constant fight against devaluation. By means of sophisticated and clever algorithms, an investor’s time in the markets should be optimized. By staying invested in risk-on assets, an investor stands the chance of properly outperforming today’s ongoing fiat devaluation.

At the same time, investors should stand ready to temporarily flee the equity and broader risk-on markets when short-term hiccups disrupt them. This can be done by attempting to anticipate recurring interest rate shocks (focusing on central banks’ “open mouth operations”) as well as volatility disruptions. But merely staying within the world of fiat-denominated assets won’t be enough. Gold as well as bitcoin offer ways to get hold of assets that can potentially function beyond the pale of traditional finance. While gold is the ultimate risk-off asset as of now, bitcoin is currently the world’s most desired risk-on asset that is rapidly developing into another risk-off vehicle outside the fiat system.

Flexibility Is Needed

Algorithms that help an investor optimize his time in the broader market as well as in concrete assets must be endowed with the greatest possible flexibility in terms of asset selections—interest rate products, volatility products, precious metal products, and digital assets allow for a nuanced strategy and can potentially outperform in different scenarios. This added flexibility gives the algorithm a huge advantage over the rigid stock and bond selection of a classic 60:40 portfolio.

After all, the rigidity of a classic 60:40 portfolio is currently more of a disadvantage than an advantage. If inflation continues to rise, as it has in recent months, central banks could be forced to momentarily deviate from their ultraexpansionary monetary policy. This would certainly bring an investor’s traditional 60:40 portfolio under even more pressure, as both equities and bonds would have to price in the new interest rate levels.

You Might Also Like

Joe Salerno on Rothbard’s History of Economic Thought

Joe Salerno on Rothbard’s History of Economic Thought

2021-10-20

We wrap up our look at Murray Rothbard’s sprawling two volume An Austrian Perspective on the History of Economic Thought with Dr. Joe Salerno, Rothbard’s friend and colleague.

“They Said What?!” John Lennon edition

“They Said What?!” John Lennon edition

2021-08-06

Bob unveils a new recurring series, in which he gives the context of infamous quotations. In this episode, he covers two allegedly shocking quotes from John Lennon, John Maynard Keynes’ "in the long run we’re all dead," Trump on Nazis being very fine people, Dan Quayle misspelling potato, Obama’s "you didn’t build that," and Bohm-Bawerk on Karl Marx.

Secession and the Production of Defense

Secession and the Production of Defense

2021-07-27

[unable to retrieve full-text content][Chapter 11 of The Myth of National Defense: Essays on the Theory and History of Security Production, edited by Hans-Hermann Hoppe (Auburn, Ala.: Mises Institute, 2003), pp. 369–413.]

Few people object to the private production of shoes or rock concerts.

Forced Vaccinations in France Bring Both Repression and Protest

Forced Vaccinations in France Bring Both Repression and Protest

2021-07-23

In a speech to the nation just ahead of Bastille Day on July 14 celebrating the French Revolution, President Emmanuel Macron delivered a paradoxical blow to the Republic’s famous slogan: Liberté, égalité, fraternité. He announced a series of measures to speed up the pace of covid-19 vaccinations which undermine individual liberties and threaten a strong political and economic backlash.

Fiat Money Economies Are Built on Lies

Fiat Money Economies Are Built on Lies

2021-07-21

Now and then, it pays to take a step back to get a broader perspective on things, to look beyond the daily financial news, to see through the short-term ups and downs in the market to find out what is really at the heart of the matter. If we do that, we will not miss the fact that we are living in the age of fiat currencies, a world in which basically everything bears their fingerprints: the economic and financial system, politics—even people’s cultural norms, values, and morals will not escape the broader consequences of fiat currencies.

Paying People Not to Work Won’t Make Us Richer

Paying People Not to Work Won’t Make Us Richer

2021-07-20

One of the most important principles of economics is that people respond to incentives. You get more of whatever you incentivize. You get less of whatever you disincentivize. This is irrefutable. The supplemental unemployment payment does both—it incentivizes people not to work, and simultaneously disincentivizes them from working.

Keynes Said Inflation Fixed the Problems of Sticky Wages. He Was Wrong.

Keynes Said Inflation Fixed the Problems of Sticky Wages. He Was Wrong.

2021-07-08

Britain’s economy had been suffering chronic unemployment for a decade prior to 1936. Economic theory as it was then understood clearly showed that the cause of a market surplus was sellers asking a price in excess of what buyers are willing to pay.

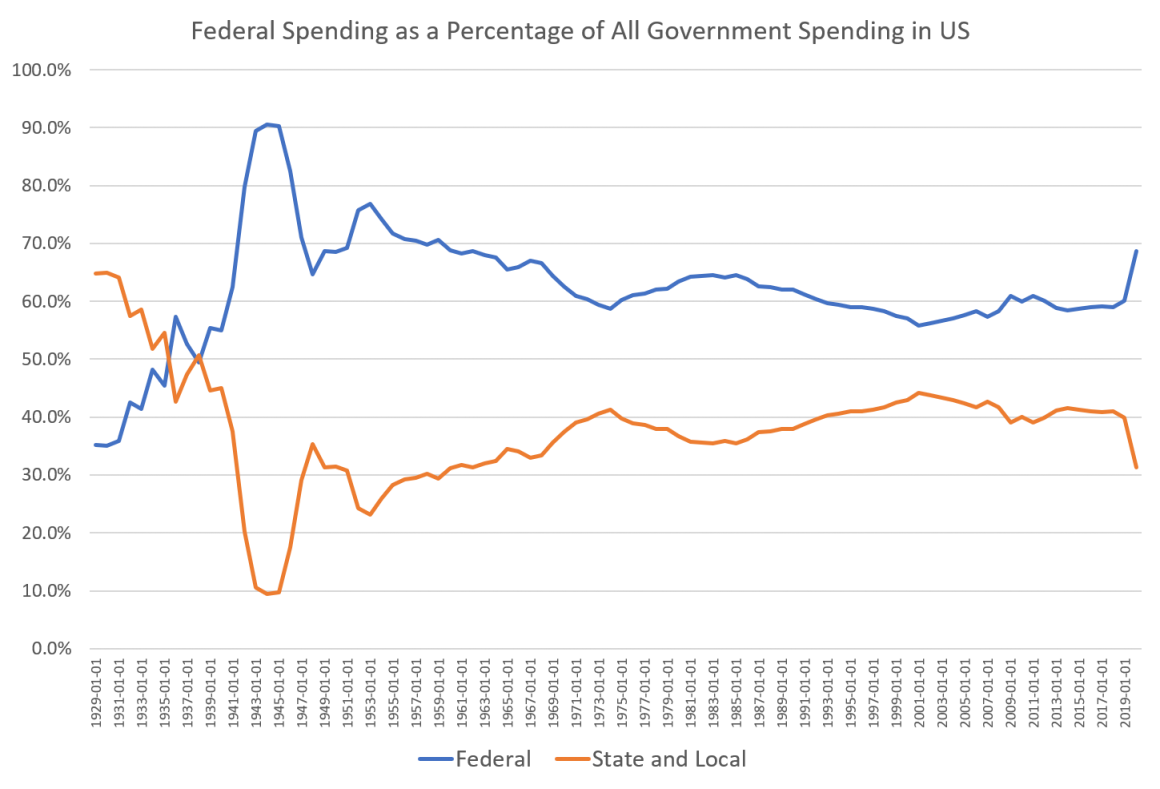

The Fed: Why Federal Spending Soared in 2020 but State and Local Spending Flatlined

The Fed: Why Federal Spending Soared in 2020 but State and Local Spending Flatlined

2021-06-28

In the wake of the Covid Recession and the drive to pour ever larger amounts of “stimulus” into the US economy, the Federal Government in 2020 spent more than double—as a percentage of all government spending—of what all state and local governments spent in 2020, combined.

Tags: Featured,newsletter