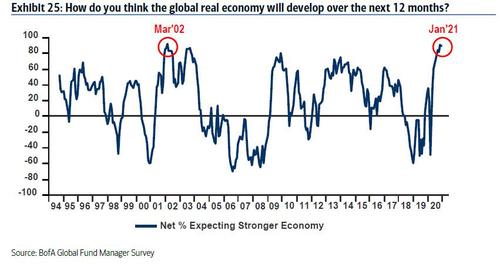

On Saturday, we showed why according to observations from Credit Suisse and BofA, the “US Economy Is Set To Overheat As Households Are Flooded With Trillion In Excess Savings.” Then, in a note this morning from Morgan Stanley asking “What To Do About All This Optimism” the bank said that “in November, December and now January, no question or concern has come up more often than ‘everyone is optimistic’.” Finally, the latest Fund Managers Survey showed that investors’ global growth expectations rose by 1% to a net 90%, the 3rd highest growth expectations ever (#1 in March 2002, #2 in November 2020). Global Real Economy, 1994-2020 - Click to enlarge This unbridled optimism prompted Goldman to boost its full year US GDP forecast to 6.6%, nearly 50% higher than

Topics:

Tyler Durden considers the following as important: 3.) Swiss Banks, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| On Saturday, we showed why according to observations from Credit Suisse and BofA, the “US Economy Is Set To Overheat As Households Are Flooded With $2 Trillion In Excess Savings.” Then, in a note this morning from Morgan Stanley asking “What To Do About All This Optimism” the bank said that “in November, December and now January, no question or concern has come up more often than ‘everyone is optimistic’.” Finally, the latest Fund Managers Survey showed that investors’ global growth expectations rose by 1% to a net 90%, the 3rd highest growth expectations ever (#1 in March 2002, #2 in November 2020). |

Global Real Economy, 1994-2020 - Click to enlarge |

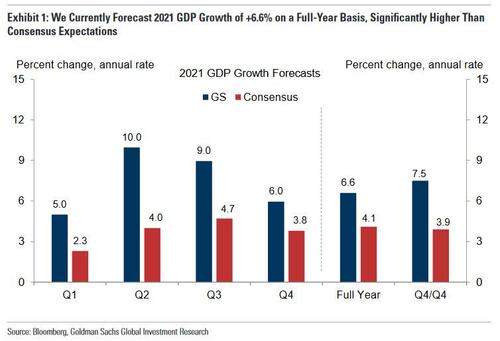

| This unbridled optimism prompted Goldman to boost its full year US GDP forecast to 6.6%, nearly 50% higher than the 4.1% consensus.

The common theme: record euphoria has gripped not just markets – Wall Street is just as euphoric about the broader economy where “everyone is optimistic” and for a very simple reason: with the Biden admin set to (realistically) unleash at least $1 trillion in new stimulus (down from Biden’s $1.9 trillion target), and also planning to unveil a new multi-trillion infrastructure program later in the year, negative numbers and bearish narratives simply do not matter ahead of this stimulus tsunami. Whether or not such euphoria is justified – after all, thanks to the Blue Wave, risks from insufficient fiscal aid or substantial scarring effects now look much less likely than a few months ago – but as Goldman’s chief economist Jan Hatzius wrote today in a lengthy note titled “What Could Go Wrong” with the 2021 rebound, other downside risks remain “including uncertainty about how consumers will respond to lingering risks and how new virus mutations will affect virus spread and vaccine efficacy.” Some more details on these three risks: |

2021 GDP Growth Forecasts - Click to enlarge |

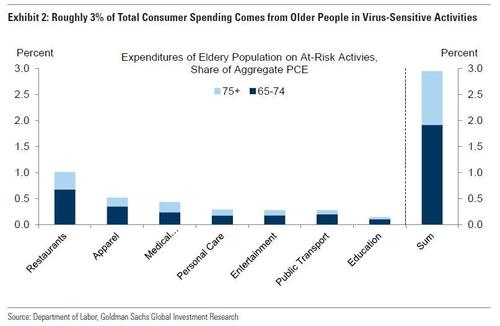

Some more details on each of these points as excerpted from the Goldman report: Downside Risk #1: Greater Consumer Caution

|

Consumer Spending - Click to enlarge |

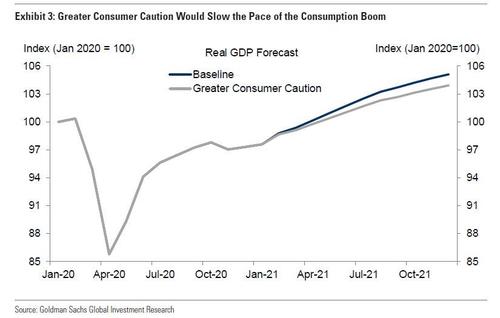

| To assess a downside case with increased consumer caution, we first use surveys of social distancing by age group to project our baseline services spending forecast across age groups, and then assume that services spending recovers 50% more slowly than in our baseline forecast for the older population and 10% more slowly for everyone else. As shown in Exhibit 3, more caution would slow the pace of the consumption boom, but would still likely imply fairly robust growth throughout 2021 of +5.9% on a full year basis (vs. +6.6% in our baseline forecast) and +6.3% on a Q4/Q4 basis (vs. +7.5%). |

Greater Consumer Caution Would Slow the Pace of the Consumption Boom - Click to enlarge |

Downside Risk #2: A Highly Infectious Strain

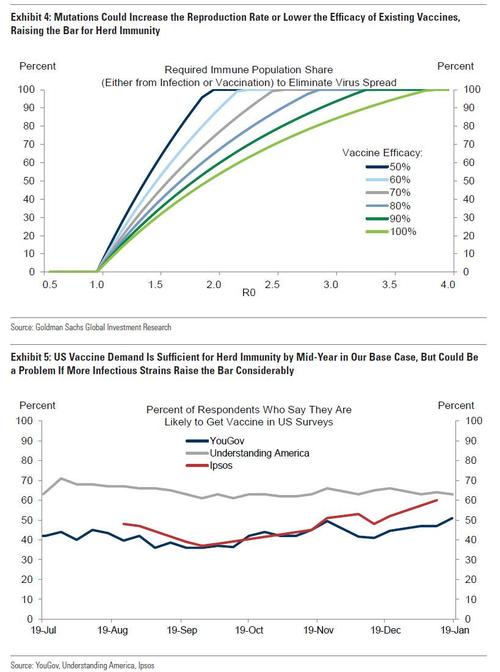

If R0 were 2.5, for example, and infections and vaccines provided an average protection of 80%, reaching herd immunity would require immunity of 86% of the population, acquired either through infection or through vaccination. While vaccine demand appears to have edged up over time (Exhibit 5) and is likely to rise as awareness of efficacy grows, achieving very elevated vaccine coverage might be challenging. This is especially true if lower efficacy or uncertainty about efficacy against new strains further discourages vaccination. |

. |

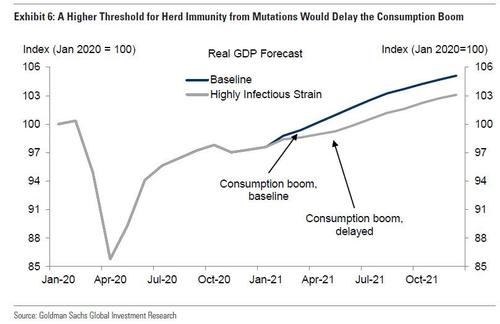

| Under the scenario where virus mutations significantly increase the bar for herd immunity, virus spread would remain considerably higher for longer and the consumption boom would likely be both delayed and softer. Exhibit 6 shows a stylized scenario where we assume that the boost from the recovery in services spending is pushed back by two months due to the delay in reaching herd immunity, and subsequent growth in services spending is 30% slower than in our baseline forecast. In this scenario we would expect moderately lower growth in 2021 of +5.1% on a full year basis (vs. +6.6% in our baseline forecast) and +5.4% on a Q4/Q4 basis (vs. +7.5%). |

. |

Downside Risk #3: Vaccine-Resistant Variant

|

Sign of Relief, 2020-2021 - Click to enlarge |

Richard Lessels (lead author of one study) characterized the results as showing that it was “possible” that that vaccine efficacy may be “slightly diminished.” At this point, it seems unlikely that vaccines will need to be adjusted to remain effective against either new strain, although the South African virus strain has more downside potential.

In addition to the risks from current strains, nearly all experts anticipate that vaccine-resistant strains could evolve, although generally do not believe such an evolution is imminent (Table 1). Instead, a vaccine-resistant virus would likely reflect the accumulation of mutations that lower the efficacy of vaccines over time. The risk that a vaccine-resistant virus strain emerges have risen recently, since higher case counts and more infectious strains increase opportunities for efficacy-lowering mutations to occur. Nevertheless, most viruses (with the seasonal flu as a notable exception) do not mutate in a manner that regularly renders vaccines ineffective, and so we do not incorporate such a mutation in our baseline forecast.

They don’t… but they just might and soon, considering the highly “political” nature of the covid pandemic, which in addition to directly toppling the Trump presidency, has emerged as the most palatable way of mainstreaming MMT and helicopter money, and overhauling the entire fiscal and monetary structure virtually overnight. It’s why one doesn’t have to be a deranged conspiracy theorist to conclude that despite the sudden improvement in the US covid picture since Biden’s inauguration, which as we reported on Friday resulted in a record one-day drop in covid hospitalizations…

… if it means that trillions more will be pumped into the economy – again, for political purposes, that the third risk, one of a “vaccine resistant virus strain”, is quite likely to emerge some time around the summer, not only to extend the lockdowns into 2022 but to give Congress and the Fed political cover for more trillions in Universal Basic Income-funding stimmy checks (while politicians quietly embezzle trillions more).

You Might Also Like

Art Basel and UBS art market survey shows online sales and millennial collectors increasingly important to an art market hit hard by COVID-19

Art Basel and UBS art market survey shows online sales and millennial collectors increasingly important to an art market hit hard by COVID-19

2020-09-09

Art Basel and UBS today published a 2020 mid-year survey ‘The Impact of COVID-19 on the Gallery Sector’ written by renowned cultural economist Dr. Clare McAndrew, Founder of Arts Economics. The survey findings present an analysis of how the COVID-19 pandemic has impacted 795 galleries operating in the Modern and contemporary gallery sector, representing 60 different markets across all levels of turnover, throughout the first six months of 2020.

UBS Global Real Estate Bubble Index 2020: Munich and Frankfurt are the most overvalued housing markets globally

UBS Global Real Estate Bubble Index 2020: Munich and Frankfurt are the most overvalued housing markets globally

2020-10-01

The UBS Global Real Estate Bubble Index, a yearly study by UBS Global Wealth Management’s Chief Investment Office, indicates bubble risk or a significant overvaluation of housing markets in half of all evaluated cities.

Change to the UBS Board of Directors

2021-01-18

The UBS Board of Directors announced today that Beatrice Weder di Mauro is not standing for re-election to the Board of Directors of UBS Group AG and UBS AG. She has informed the Board of her decision to step down after serving since 2012.

Weekly View – Election nerves increase

Weekly View – Election nerves increase

2020-09-10

The sell-off in stocks last week showed a certain nervousness about the sharp run-up in tech stocks and the role of big option bets. Indeed, prices in some instances had risen too fast. But this was a technical correction. With the US tech titans generating free cash flow, we do not believe we are facing a repeat of the bursting of the dot-com bubble in 2000.

Weekly View – No breakfast at Tiffany’s

Weekly View – No breakfast at Tiffany’s

2020-09-18

The impact of political tensions on business is ever more apparent: LVMH of France will not, after all, proceed with the purchase of Tiffany of the US. If, as seems likely, the hand of the French government was involved, this is solid evidence that political sensitivities are increasingly influencing cross-border deals – something that is likely to remain the case just as M&A in general has been declining.

“Monetäre Staatsfinanzierung mit Folgen (Monetary Financing of Government),” Die Volkswirtschaft, 2020

“Monetäre Staatsfinanzierung mit Folgen (Monetary Financing of Government),” Die Volkswirtschaft, 2020

2020-07-27

Die Volkswirtschaft, 24 July 2020. PDF. Clarifying the connections between outright monetary financing, QE, the distribution of seignorage profits, the relationship between fiscal and monetary policy, and central bank independence.

Temporary employee sector hit hard by Covid-19 crisis

Temporary employee sector hit hard by Covid-19 crisis

2020-07-30

The number of hours worked by temporary employees in Switzerland has dropped by about 23% due to the impact of restrictions imposed in the wake of the Covid-19 pandemic.

FX Daily, July 30: Greenback’s Bounce is Likely Short-Lived

FX Daily, July 30: Greenback’s Bounce is Likely Short-Lived

2020-07-30

A wave of profit-taking is seen through most of the capital markets today, with the exception of the bond market, where yields continue to trend lower. The US 10-year is now yielding 55 bp, a new low since early March, and the five-year yield set a new record low near 23 bp. European yields are 2-4 bp lower.

Tags: Featured,newsletter