Last week, German chancellor Merkel delivered a surprise about-face when she and French president Macron announced a proposal for a EUR 500bn recovery fund in the wake of the coronavirus crisis. The unprecedented plan involves the distribution of grants, rather than loans, to member states in economic need. The deal is far from done, however, as it is currently opposed by the EU ‘frugal four’, who insist on loans rather than grants, which would over-indebt countries like Spain and Italy. The European Commission will propose its own plan this week, with a final agreement during the EU Council in mid-June. Meanwhile, as lockdown restrictions eased across the euro area, purchasing manager indices for May recovered from April’s record lows, despite remaining in

Topics:

Cesar Perez Ruiz considers the following as important: 2.) Pictet Macro Analysis, 2) Swiss and European Macro, Featured, Macroview, newsletter, Pictet

This could be interesting, too:

investrends.ch writes Pictet als Bester Schweizer Asset Manager im Bereich Nachhaltigkeit und Markenführung ausgezeichnet

investrends.ch writes Vom Ölschock zum Stromsuperzyklus

investrends.ch writes Pictet steigt in den Schweizer Treuhandmarkt ein – Partnerschaft mit Tretor

investrends.ch writes Die Schweiz an der Schwelle zur digitalen Transformation der Fondsindustrie

Last week, German chancellor Merkel delivered a surprise about-face when she and French president Macron announced a proposal for a EUR 500bn recovery fund in the wake of the coronavirus crisis. The unprecedented plan involves the distribution of grants, rather than loans, to member states in economic need. The deal is far from done, however, as it is currently opposed by the EU ‘frugal four’, who insist on loans rather than grants, which would over-indebt countries like Spain and Italy. The European Commission will propose its own plan this week, with a final agreement during the EU Council in mid-June. Meanwhile, as lockdown restrictions eased across the euro area, purchasing manager indices for May recovered from April’s record lows, despite remaining in contraction territory. This indicates that we may be past the bottom, the European economy having turned a corner. More encouraging news came from the race to find a coronavirus vaccine last week, which could add further support to market sentiment.

Last week, German chancellor Merkel delivered a surprise about-face when she and French president Macron announced a proposal for a EUR 500bn recovery fund in the wake of the coronavirus crisis. The unprecedented plan involves the distribution of grants, rather than loans, to member states in economic need. The deal is far from done, however, as it is currently opposed by the EU ‘frugal four’, who insist on loans rather than grants, which would over-indebt countries like Spain and Italy. The European Commission will propose its own plan this week, with a final agreement during the EU Council in mid-June. Meanwhile, as lockdown restrictions eased across the euro area, purchasing manager indices for May recovered from April’s record lows, despite remaining in contraction territory. This indicates that we may be past the bottom, the European economy having turned a corner. More encouraging news came from the race to find a coronavirus vaccine last week, which could add further support to market sentiment.

In markets, a ban on short-selling in Europe in place since mid-March to stem coronavirus panic was lifted last week, putting further pressure on financial stocks. At the same time, demand for safety in bonds remained insatiable. The UK issued a negative yielding bond for the first time ever in an over-subscribed sale, suggesting investors expect the Bank of England to deliver further easing in support of the economy. Last week too, the US issued a 20-year bond for the first time in over three decades in an oversubscribed sale of its own. We continue to prefer US Treasuries over other government bonds.

With US presidential elections looming, relations between the world’s two largest economies deteriorated further last week. Chinese authorities moved to impose national security legislation on Hong Kong, reigniting the latter’s pro-democracy demonstrations over the weekend and drawing criticism from US officials. Meanwhile, the US Senate passed a bill that would require US-listed foreign companies to submit to an audit by a US oversight board to determine that they are not under foreign control, or face delisting. Chinese companies with ADR (American depository receipt) US listings are the apparent target, with many assumed to not be able to comply, given Chinese laws around the protection of state secrets. If implemented, the bill will be tougher for the 200+ small Chinese ADR issuers, while the large ones are more likely to complain and move their listings to the UK or Hong Kong.

You Might Also Like

Modern Monetary Theory makes inroads following coronavirus crisis

Modern Monetary Theory makes inroads following coronavirus crisis

US policymakers’ bold actions in response to the coronavirus bear some traces of the free-wheeling deficits, repressed interest rates and central bank activism (money creation) that form the cornerstones of the Modern Monetary Theory (MMT) playbook.

Core sovereign bonds 2020 Outlook

Core sovereign bonds 2020 Outlook

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.

Upward pressure on equity volatility mitigated by fund flows

Upward pressure on equity volatility mitigated by fund flows

Whereas inflation is expected to be dormant next year, our expectation of real GDP growth of just 1.3% in the US in 2020 could put upward pressure on equity volatility. Since monetary policy tends to lead volatility by two and a half years, the Fed’s turn toward quantitative tightening in 2017 is also continuing to exert upward pressure on volatility levels for now.

ECB: Preview of the review

ECB: Preview of the review

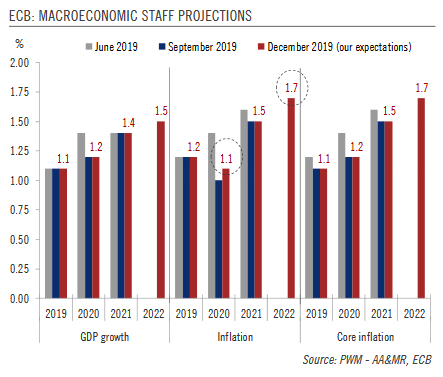

We see the ECB remaining on hold throughout next year although we believe it could tweak some of the technical parameters of its toolkit. The first press conference of any new ECB President is an event in itself, and this time will be no different. Christine Lagarde’s debut this week will understandably attract a lot of attention as the media and market participants scrutinise both form and substance.

Weekly View – Merkel under pressure

Weekly View – Merkel under pressure

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.

Central banks to the rescue

Central banks to the rescue

While expecting long-term yields to be capped, we remain neutral on US Treasuries. We think peripheral euro area bonds to avoid the levels of stress seen during the sovereign debt crisis.

A reality check on China’s return to work

A reality check on China’s return to work

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.

House View, May 2020

House View, May 2020

With leading economies likely facing double-digit declines in GDP in Q1 and Q2, we expect Brent oil in the USD10–20 range in Q2 before reaching a long-term equilibrium of USD18 at year’s end. With consumers tempted to remain cautious, the oil sector in deep difficulty and a big rise in unemployment, we expect dire Q2 GDP figures for the US. We have reduced our GDP forecast for 2020 as a whole to -7.7%.

Tags: Featured,Macroview,newsletter,Pictet