The US-China trade conflict and then US-Iran confrontation distracted investors from the macroeconomic drivers of the capital markets. It is not that there is really much closure with the exogenous issues, but they are in a less challenging place, at least on the surface. A Chinese delegation, led by the Vice-Premier Liu He, who spearheaded the negotiations, will participate in the signing ceremony on January 15.. While China has agreed to buy 0 bln more of US goods over the next two years, they were prepared to do this or something similar more than a year ago with the trade deal that Treasury Secretary Mnuchin had struck but that President Trump rejected. And don’t forget that in 2017, China-US business deals secured on Trump’s trip to Beijing heralded as

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of England, Economics, Featured, Federal Reserve, Geopolitics, newsletter, South Korea

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

The US-China trade conflict and then US-Iran confrontation distracted investors from the macroeconomic drivers of the capital markets. It is not that there is really much closure with the exogenous issues, but they are in a less challenging place, at least on the surface.

A Chinese delegation, led by the Vice-Premier Liu He, who spearheaded the negotiations, will participate in the signing ceremony on January 15.. While China has agreed to buy $200 bln more of US goods over the next two years, they were prepared to do this or something similar more than a year ago with the trade deal that Treasury Secretary Mnuchin had struck but that President Trump rejected. And don’t forget that in 2017, China-US business deals secured on Trump’s trip to Beijing heralded as much as $250 bln seems illusory.

Moreover, the new agreement violates the spirit if not the letter of the WTO, which seeks to avoid narrow preferential treaties. In some ways, the US secured a sphere of influence: Based on a political decision, the US share of China’s import market will increase and increase substantially at the expense of the market share of other countries. And for the record, during most of 2019, China’s imports were falling.

There is little reason to believe that the Iranian missile strike on Iraqi-bases that housed US forces brings meaningful closure. However, as with the US-China Phase 1 the trade agreement, the cessation of hostilities should not be confused with peace. There was little chance of a Phase 2 agreement with China. Chinese officials have said as much. President Trump recognized the same and suggested that such a deal may come in “his second term.”

Iran’s national self-interest, as determined by its political and religious elite, brings it in opposition to the US. The recent events will likely reinforce the idea that it needs nuclear weapons to protect its sovereignty. The market may price a greater risk premium for oil, and the first test of its assessment may come as the Feb WTI contract approaches the 100 and 200-day moving averages (~$57-$58 a barrel). The March Brent contract has tested its 200-day moving average (~$64.30), while the 100-day moving average near $62.50.

The US-China rivalry can be understood as classic great power politics, which is often compared to a chess game. The US-Iran confrontation seems often expressed through proxies and subterfuge and is more comparable to something like the dance of seven veils.

Investors tend to ignore the low but constant geopolitical jockeying for position, like the background echo of the Big Bang that scientists can detect. However, when it geopolitical tensions escalate, the market spasms. With the tensions subsiding, investors’ attention will likely return to macroeconomic news in a chock-full week of high-frequency reports.

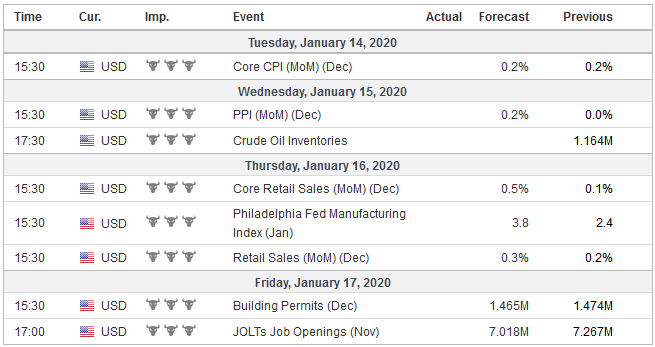

United StatesThe US reports the December readings on inflation, consumption, and production. The Empire State and Philadelphia Fed manufacturing surveys will provide the first inklings into Q1 20, as will the more anecdotal Beige Book, compiled for the upcoming FOMC meeting. The US data may take on greater significance in light of the weak December jobs report and the slower earnings growth. There are conflicting signals about the growth of the US economy in Q4, as illustrated by the divergence between the Atlanta and NY Fed GDP trackers. The former is 2.3% while the latter stands at 11%. |

Economic Events: United States, Week January 13 - Click to enlarge |

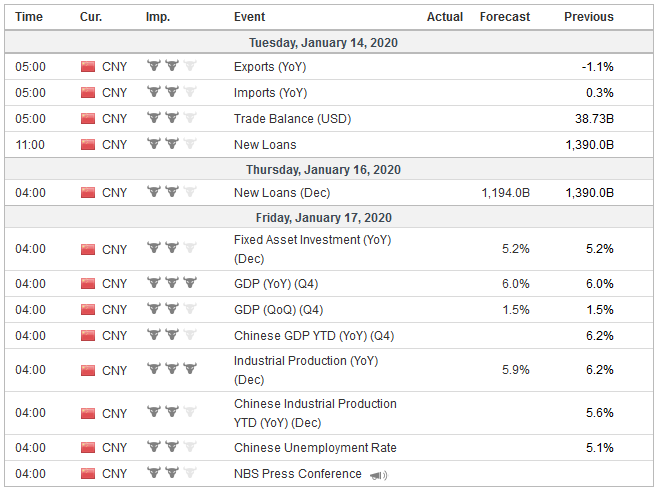

ChinaChina reports December data—lending, trade, retail sales, industrial production—culminating with an estimate of Q4 GDP. Many observers write and talk as if Chinese officials make up the data to whatever they want. If true, why would there ever be disappointment and weakness? Other attempts to estimate the growth seem to suggest that the official estimates are a reasonable approximation. Consider what the US does. It reports an initial estimate and then revises it for years. The PBOC has eased policy through a reduction of reserve requirements and is providing liquidity to the banking system ahead of the Lunar New Year. The one-year Loan Prime Rate, the increasingly important benchmark, is likely to fall 5-10 bp when it is set on January 20. |

Economic Events: China, Week January 13 - Click to enlarge |

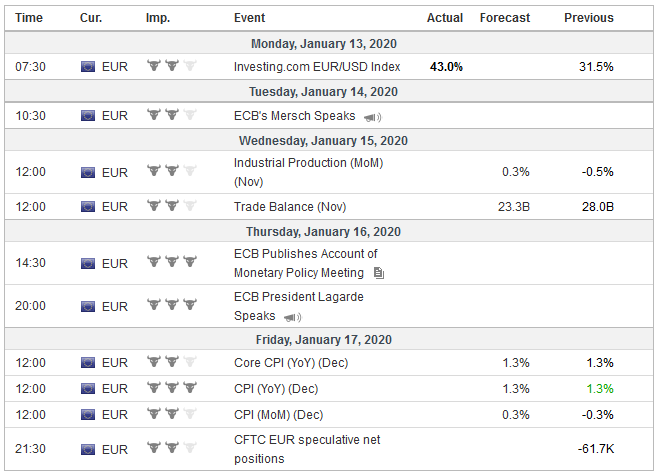

EurozoneThe four largest eurozone countries reported December industrial production figures that surprised to the upside, including Germany and Italy, which have been struggling. This suggests an upside risk on the aggregate report. Similarly, the continued weakness of German exports hints of smaller surplus for the eurozone as a whole. German will report 2019 GDP, and within it will contain the first read of Q4 GDP. The Bundesbank has warned that the economy may have stagnated. The UK will exit the EU on January 31 into a standstill agreement for the rest of the year. Nothing changes while a new trade agreement is negotiated. There is much posturing by the UK and the EC in this pre-negotiating dance. With the election uncertainty lifted, investors can turn their attention back to the economy. The consensus narrative has been that the lifting of this uncertainty will remove a headwind on the UK economy. There are some cracks in the story, but the data next week may not be decisive. The data-dump includes inflation, trade, industrial output, and the service index (similar to Japan’s tertiary index). BOE Governor Mark Carney’s term that was supposed to end this month has been extended again, but he sounds like a man with a mission. He recently talked about a digital alternative to the role of the dollar as a reserve asset (I wish I had a penny for every time someone claimed to identify a rival to the dollar), why central banks need to take into account climate change, and that it may have to act quickly and decisively if it concludes the economy is weakening. |

Economic Events: Eurozone, Week January 13 - Click to enlarge |

Japan reports November trade figures, core machinery orders, and the tertiary index. There is little doubt that the world’s third-largest the economy contracted in Q4. The one-two punch of the October sales tax increase and tsunami hit an economy with a shrinking working-age population and weak real income. This month’s Bloomberg survey showed net-net median forecast now anticipates a 3.7% annualized decline in Q4 19 GDP from last’s month’s projection of a 2.6% fall.

Carney, too sounded dovish. “The economy has been sluggish, slack has been growing, and inflation is below target,” he explained last week. Two members of the Monetary Policy Committee have voted at the past two meetings to cut rates immediately. Before the weekend, MPC member Tenreyro suggested that she, too, could support a rate cut if the economic data does not improve.

The market appears ill-prepared for a UK rate cut, and the risk seems greater than generally appreciated. Sterling’s recovery on a broad-trade weighted basis (~10% in the last four months) moves financial conditions in the opposite direction and may also help provide more room to maneuver for the Bank of England. Interpolating from the derivatives market, investors appear to be discounting about a 1-in-4 chance fo a cut at this month’s meeting (Jan 30) and about a 1-in-3 chance of a reduction at the following meeting (March 26).

Three emerging market central banks meet next week that typically draw attention. The central banks of Turkey and South Africa meet on January 16, and the Bank of Korea meets the following day. A more compelling case of the need for South Africa to cut rates that Turkey can be made. But next week, South Africa’s Reserve Bank is expected to standpat while the central bank of Turkey cuts. South Africa’s economy contracted (-0.6%) in Q3 and was nearly flat year-over-year (0.1%). The economic data for Q4 is worrisome. Headline CPI is a little north of 3%, while the key repo rate is at 6.50%. A proxy then for the real rate is about 3.5%.

Turkey’s CPI rose to 11.8% in December from 10.6% in November. It bottomed in October, near 8.5%. The key policy rate, the one-week repo, is at 12%. The proxy real rate is less than 50 bp. That does not mean that the central bank won’t cut rates, but that easy monetary policy at this juncture may weaken the currency further. The lira fell about 10% against the euro and about 12.5% against the dollar in 2019. A weaker lira will likely boost inflation, while the further erosion of confidence in the central bank may exacerbate Turkey’s economic challenges.

South Korea’s one-week repo rate (1.25%) will most likely be left alone when the central bank meets on January 17. The most recent data lends credence to views of a preliminary economic recovery. The drag from exports is easing. News from the important semiconductor industry and guidance by Samsung has also been positive, and the December manufacturing PMI rose back above the 50 boom/bust level. The dollar encounters key support near KRW1150, and a break could set the tone for the weeks.

China faces another challenge and it is primarily of its own making. Taiwan holds national elections and by the time Asian markets open on Monday, the results will be known. Most like the Tsai Ing-Wen will be re-elected. There may not be any strong market reaction but it may embolden her to seek greater distance from China, and given the China hawks that seem to dominate the US administration, she will likely find support from the US.

Tags: Bank of England,Economics,Featured,federal-reserve,Geopolitics,newsletter,South Korea