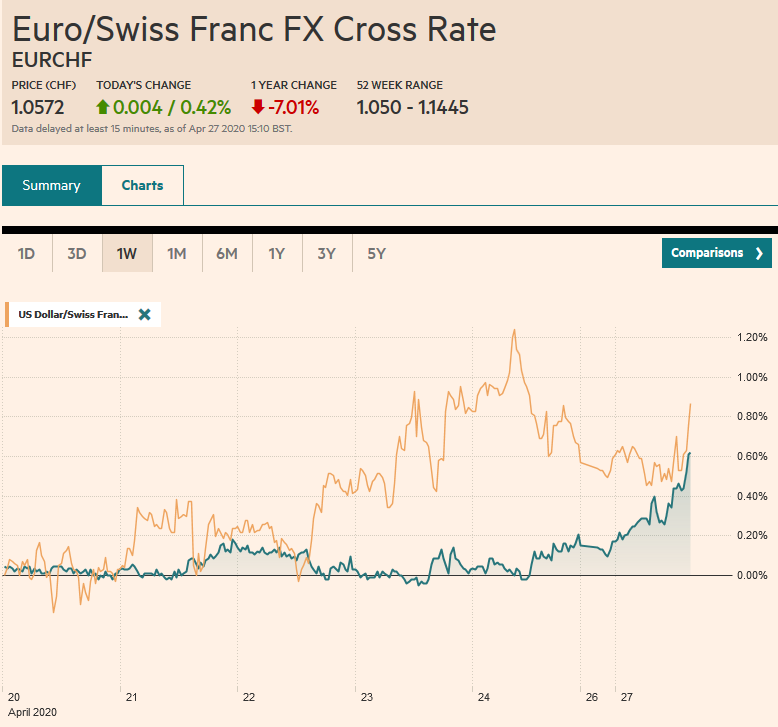

Swiss Franc The Euro has risen by 0.42% to 1.0572 EUR/CHF and USD/CHF, April 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Global equities are beginning the new week on an upbeat note. All the markets in the Asia Pacific region rallied, led by more than 2% gains in the Nikkei and Taiwan. European bourses are higher. All the industry groups are participating and financials and consumer discretionary leading the way. The Dow Jones Stoxx 600 has been in a 320-340 range for the better part of three weeks and is approaching the upper end. The S&P 500 looks poised to gap higher at the opening. The April high just below 2880 is coming into view. Core benchmark yields are a little higher, but the peripheral

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Brazil, Currency Movement, EUR/CHF, Featured, India, newsletter, Oil, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.42% to 1.0572 |

EUR/CHF and USD/CHF, April 27(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equities are beginning the new week on an upbeat note. All the markets in the Asia Pacific region rallied, led by more than 2% gains in the Nikkei and Taiwan. European bourses are higher. All the industry groups are participating and financials and consumer discretionary leading the way. The Dow Jones Stoxx 600 has been in a 320-340 range for the better part of three weeks and is approaching the upper end. The S&P 500 looks poised to gap higher at the opening. The April high just below 2880 is coming into view. Core benchmark yields are a little higher, but the peripheral European bonds are rallying with risk assets. Yields in Italy, Spain, and Portugal are 5-10 bp lower, while Greece’s benchmark yield is off 12 bp. The dollar is softer against all the major and most emerging market currencies. The dollar bloc is the strongest, while the euro and Swiss franc are laggards. JP Morgan’s Emerging Market Currency Index is snapping a five-day slide. Gold is off almost 0.5% as it consolidates above $1700. Crude oil is snapping a three-day advance, and the June WTI contract is near $14 a barrel. |

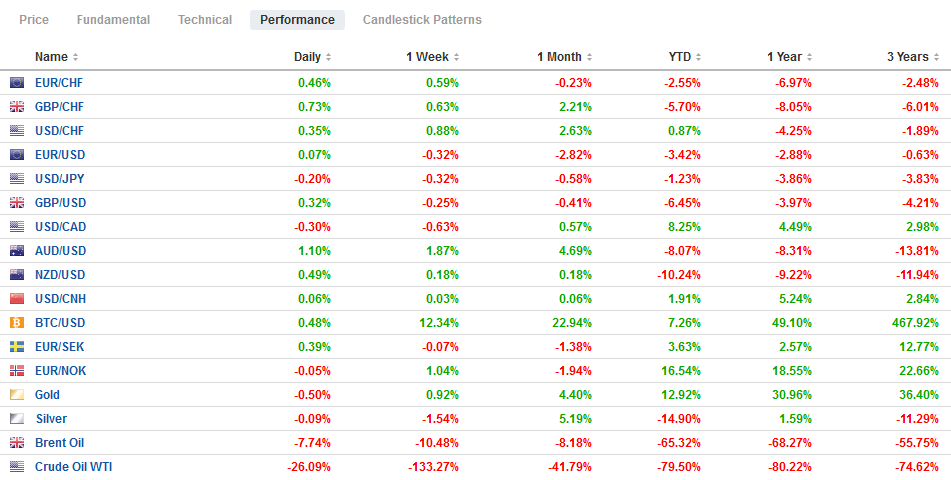

FX Performance, April 27 - Click to enlarge |

Asia Pacific

The Bank of Japan made modest adjustments to its policy earlier today. Three steps were taken. First, it removed the JPY80 trillion cap on government bond purchases. This is largely symbolic as the yield curve control policy has seen its bond purchases fall well shy of the cap (~JPY14 trillion over the past 12 months). It did make a minor tweak to the different buckets (maturities) that it will buy. Second, it doubled the amount of corporate bonds, and commercial paper it will purchase (to JPY20 trillion). This was as expected. Third, it expanded access to its emergency loan facility to a wider range of banks. Its forecasts were sobering. Growth, it suggested, could contract by up to 5% (IMF -5.2%), and inflation could be -0.7% this fiscal year.

India’s central bank opened a new credit facility for mutual funds after Franklin Templeton shut six funds last week, citing a lack of liquidity. The new facility is for INR500 bln (~$6.6 bln) as of today that can be lent to the mutual fund industry or buy investment-grade debt held by the funds. Corporate borrowing costs soared after the funds were closed.

The dollar slipped toward the lower end of its two-week trading range against the yen (~JPY106.90-JPY108.10). There is an option for $1.2 bln struck at JPY107.00 that expires today. There are also options for $1.1 bln placed in the JPY107.55-JPY107.60 range that also expire today. The options may mark the range in the North American morning. The Australian dollar was bid to new highs for the month today near $0.6470. Note that $0.6450 corresponded to the (61.8%) retracement of this year’s decline. The next immediate target is near $0.6500, though a close below $0.6445 would be seen as a failure. The Chinese yuan was sidelined and little changed with the dollar near CNY7.08030.

Europe

S&P maintained its BBB rating of Italy and its negative outlook. It noted the ECB’s backstop, and that in nominal terms, assuming no further deterioration in borrowing costs, Italy may pay less to service its sovereign debt the next few years than it did in 2019. It seemed to suggest that it needed so see improvement in the debt trajectory over the medium-term (three years). It suggested the same thing about the UK’s debt trajectory as the rating agency maintained its AA rating. S&P cut the outlook of Greece’s BB- rating to negative.

The Swiss National Bank appears to have stepped up its intervention. Sight deposits jumped by CHF13.4 bln (~$14 bln) in the week ending April 24. They can be influenced by other activities but are believed to reflect ongoing attempts to limit additional strength against the euro. The euro had been hovering just above CHF1.05 over the last couple of weeks, which is its lowest level in about five years. Today, the euro traded near CHF1.0560, its highest in a couple of weeks. A move above CHF1.06 is needed to signal anything important from a technical perspective.

The euro had fallen to its lowest level in a month (~$1.0725) at the end of last week before recovering to settle on the session highs, almost a cent higher. Follow-through buying today lifted it to about $1.0860 in late Asian turnover. It has consolidated in the European morning. The $1.0800-$1.0820 area holds expiring options worth about 1.7 bln euros. Last week’s high was near $1.09, and this needs to be convincingly taken out to lift the tone. Sterling reached a five-day high today near $1.2455. Last week’s top was just above $1.2500. A gain above there is needed to undermine a potential head and shoulders topping pattern some see. Initial support is seen near $1.2420.

America

The busy week in North America begins slowly. The US and Canada have a light schedule today, with Mexico reporting March unemployment statistics. The first look at US Q1 GDP and the FOMC meeting are the highlights. Canada reports February monthly GDP later this week. Mexico also reports Q1 GDP, which is expected to have fallen for the fifth consecutive quarter. US oil inventory data will draw attention. Despite cuts in output, and the shuttering of more oil rigs (-60 last week, leaving 378, a four-year low), US storage space is quickly becoming exhausted, and there is concern that the problem will persist through the expiration of the June WTI contract.

Over the weekend, Treasury Secretary Mnuuchin reiterated that the US was looking at how to help the oil sector. It is not clear if it would be another facility that Fed supported or whether it would be the Treasury or Energy Department taking a leading role. Last week, President Trump again threatened tariffs on oil imports. Trump has also spoken about boosting the Strategic Petroleum Reserves and giving some private producers access to some of its storage capacity. Several of the largest oil companies, including Exxon, Mobil, British Petroleum, and Royal Dutch report earnings this week. Many still insist the lower oil prices are a function of a dispute between Saudi Arabia and Russia. Yet, since 2008, the US has doubled its output, which reached 13 mln barrels per day by the end of last year.

The US is not the low-cost producer, though access to cheap capital helped. The industry was set for consolidation even before the latest drop. Failures and acquisitions are rationalizing the fragmented shale industry and the larger players finding opportunities. Diamond Offshore Drilling became the latest casualty over, filing bankruptcy after missing a debt servicing payment a week and a half ago. Last year, its losses doubled to almost $360 mln as revenues fell by about $100 mln to $980 mln. We suspect that most of the US assistance would not go to the small fledgling producers, many of whom are not investment grade. If this is true, it may accelerate the re-shaping of the industry, while at the same time, putting down a marker that claims the US will not bear the burden of the global adjustment: Saudi Arabia and Russia need to accommodate it.

The Brazilian real slumped to record lows before the weekend following the resignation of the Justice Minister Moro, who was held in high regard as the driving force behind the anti-corruption Car Wash investigation that ultimately jailed former President Lula. It followed the dismissal of the head of the Federal Police. President Bolsonaro has been widely criticized for the handling of the health crisis and last week dismissed the Health Minister that favored social isolation. The Bovespa lost roughly 5.5% at the end of last week.

The US dollar traded between CAD1.40 and CAD1.42 last Thursday. This range is still key for the near-term outlook. After finishing last week near CAD1.4100, the US dollar slipped to about CAD1.4040 before finding support. We continue to see the Canadian dollar more sensitive to the risk appetite (S&P 500 proxy) than oil prices per se. A convincing break of the CAD1.40 area would target the month’s low near CAD1.3860. The greenback closed firmly against the Mexican peso at the end of last week after poking above MXN25.00 for the first time since April 6, when the record high was set (~MXN25.7850). It is trading within the pre-weekend range and found support near MXN24.75, just above the five-day moving average.

You Might Also Like

FX Daily, December 12: Enguard Lagarde

FX Daily, December 12: Enguard Lagarde

With the FOMC meeting delivered no surprises, attention turns to the ECB meeting as the UK go to the polls. Lagarde will hold her first press conference as ECB president today, and it will naturally command attention. Equities are advancing today, and tech appears to be leading the way. In Asia Pacific, Taiwan and South Korea rallied more than 1%, while the Hang Seng gapped higher to almost its best level in three weeks.

FX Daily, February 6: Stocks Push Higher but more Cautious Tone may be Emerging

FX Daily, February 6: Stocks Push Higher but more Cautious Tone may be Emerging

Overview: The bullish enthusiasm that carried the S&P 500 to new closing highs yesterday is helping Asia Pacific and European shares today. The MSCI Asia Pacific Index rose for the third session with Tokyo, Hong Kong, and Korea jumping two percent. Europe’s Dow Jones Stoxx 600 gapped to new record highs before stabilizing in mid-morning turnover. US shares are mostly firmer.

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims

Overview: Equity losses in the US appeared to drag most Asia Pacific markets lower today, with China and India the notable exceptions. European bourses are higher, and the only energy sector is a drag on the Dow Jones Stoxx 600, which is around 1% higher in late morning turnover, while US shares are also trading firmer. Asia Pacific 10-year benchmark yields eased.

FX Daily, April 21: Oil Drilled Below Zero, Equity Rally Stalls, Greenback Advances

FX Daily, April 21: Oil Drilled Below Zero, Equity Rally Stalls, Greenback Advances

Overview: Oil’s wild ride has been joined by two other developments that are keeping investors off-balance. First, reports suggest that North Korea’s Kim Jong-Un maybe in critical condition after surgery. He apparently was absent from last week’s events celebrating his grandfather. The concern is about a potential power vacuum and the command and control of North Korea’s weapons. Second, in a tweet late yesterday, US President Trump said he would sign an executive order suspending immigration, ostensibly to fight the virus and protect jobs. No details were provided. Trump has also renewed his threat to stop imports of Saudi and Russian oil. These disruptions have seen global equities fall. Following yesterday’s 1.8% decline of the S&P 500, most of Asia Pacific’s major bourses

FX Daily, April 22: Investors Catch Collective Breath, but Sentiment remains Fragile

FX Daily, April 22: Investors Catch Collective Breath, but Sentiment remains Fragile

Overview: Risk-appetites appear to have stabilized for the moment. Most equity markets are higher. Japan and Malaysia were exceptions, but the MSCI Asia Pacific Index rose for the first time this week. In Europe, the Dow Jones Stoxx 600 is recouping about a third of yesterday’s loss.

FX Daily, January 9: Animal Spirits Roar Back

FX Daily, January 9: Animal Spirits Roar Back

Overview: The S&P 500 recovered from a 10-day low to reach a new record high, which set the tone for the Asia Pacific and European markets today. The MSCI Asia Pacific Index jumped by the most in a month with the Nikkei’s 2% advance leading the way. More broadly, the markets in Taiwan, South Korea, Hong Kong, India, and Thailand all rose more than 1%.

FX Daily, March 31: March Ends like a Lion, No Lamb in Sight

FX Daily, March 31: March Ends like a Lion, No Lamb in Sight

Overview: The coronavirus plague upended the world in March. Equities are finishing the month on a firm note. Strong gains in the US yesterday and an unexpectedly strong Chinese PMI (yes, to be taken with the proverbial grain of salt) helped lift most Asia Pacific and European markets today. Japan and Australia are exceptions to the generalization.

FX Daily, April 14: Equities are Firm but New Developments Needed or Risk Appetites may Become Satiated

FX Daily, April 14: Equities are Firm but New Developments Needed or Risk Appetites may Become Satiated

Overview: Risk appetites have returned today after taking yesterday off. The MSCI Asia Pacific Index advanced every day last week, slipped yesterday, and jumped back today. Most of the national benchmark advanced at least 1.5%, and the Nikkei led the way with a 3% rally to reach its best level since mid-March.

Tags: #USD,Brazil,Currency Movement,EUR/CHF,Featured,India,newsletter,OIL,USD/CHF