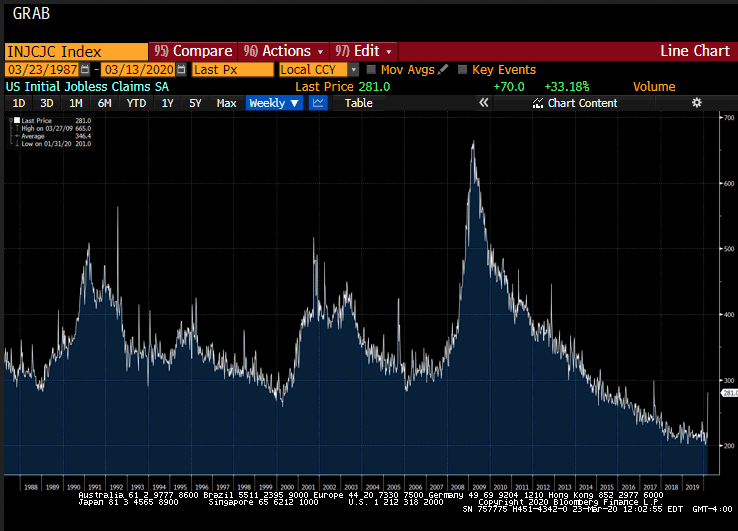

Here is the link for the replay of the conference call I hosted earlier today. I shared two ways in which this crisis is different from what we have seen in the last generation. Unlike the Great Financial Crisis, the tech bubble, and the S&L Crisis, the current crisis did not begin in the financial sector, but the real economy. Also, what follows from that is that this crisis is about liquidity, while the GFC was about counter-party risk. In the call, I covered five main topics: The economic hit like we have never experienced as significant parts of the economy are shutdown. Flash March PMIs tomorrow will give an inkling and the weekly jobless claims, which surged by a third in last week’s, are forecast to jump five-fold (~1.45 mln) in this Thursday’s report and

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, economy, Featured, Federal Reserve, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Here is the link for the replay of the conference call I hosted earlier today. I shared two ways in which this crisis is different from what we have seen in the last generation. Unlike the Great Financial Crisis, the tech bubble, and the S&L Crisis, the current crisis did not begin in the financial sector, but the real economy. Also, what follows from that is that this crisis is about liquidity, while the GFC was about counter-party risk.

In the call, I covered five main topics:

|

US Initial Jobless Claims SA, 1988-2019 - Click to enlarge |

You Might Also Like

FX Daily, March 16: Monday Blues: Fed Moves Bigly and Stocks Slump

FX Daily, March 16: Monday Blues: Fed Moves Bigly and Stocks Slump

Overview: The Federal Reserve and central banks in the Asia Pacific region acted forcefully, but were unable to ease the consternation of investors. The Reserve Bank of New Zealand cut key rates by 75 bp. The Bank of Japan appears to have doubled its ETF purchase target to JPY12 trillion, and the Reserve Bank of Australia is preparing for new measures that will be announced Thursday.

FX Daily, March 18: Bonds Join Equities in the Carnage

FX Daily, March 18: Bonds Join Equities in the Carnage

Overview: A new phase of the market turmoil is at hand. Bonds are no longer proving to be the safe haven for investors fleeing stocks. The tremendous fiscal and monetary efforts, with more likely to come, have sparked a dramatic rise in yields. Meanwhile, equities are getting crushed again.

FX Daily, March 19: ECB’s Bazooka Support Bonds but not the Euro

FX Daily, March 19: ECB’s Bazooka Support Bonds but not the Euro

Overview: It is not just that the dollar soared while stocks and bonds continued to plunge. The dollar’s strength is, in effect, a powerful short-covering rally. It was used to fund a great part of the global circuit of capital. The circuit of capital is in reverse now, and the funding currency is being bought back. The dollar’s strength is a function of the sell-off of other assets.

FX Daily, March 23: Greenback Demand Not Satisfied by Swap Lines

FX Daily, March 23: Greenback Demand Not Satisfied by Swap Lines

Overview: In HG Wells’ "War of the Worlds," the common cold repelled a Martian invasion. Now, a novel coronavirus is disrupting everything and everywhere. Global equities continue to get hammered, though the apparent relative resilience of Japan may have spurred some buying of Japanese equities.

FX Daily, October 2: Greenback Shows Resiliency, Stocks Don’t

FX Daily, October 2: Greenback Shows Resiliency, Stocks Don’t

Shockingly poor ISM data sent shivers through the market on Tuesday and hand the S&P 500 its biggest loss in five weeks and took the shine off the greenback. The S&P 500 reached a five-day high before reversing course and cast a pall over today’s activity. All the markets were lower in Asia Pacific, with China and India closed for holidays.

FX Daily, October 9: Hope is Trying to Supplant Pessimism Today

FX Daily, October 9: Hope is Trying to Supplant Pessimism Today

Overview: The 1.5% drop in the S&P 500 and the deterioration of US-China relations and the prospects of a no-deal Brexit failed did not carry over much into today’s activity. Asia Pacific equities were mostly a little lower, though China and India bucked the regional trend, while Korea was closed for a national holiday. Taiwan led the losses amid a sell-off in semiconductor stocks.

FX Daily, January 29: Escaped from a Crocodile’s Mouth, Entered a Tiger’s Mouth

FX Daily, January 29: Escaped from a Crocodile’s Mouth, Entered a Tiger’s Mouth

Overview: This colorful Malay saying captures the spirit of the animal spirits. Narrowly escaping an escalation of a trade war between the world’s two largest economies, the outbreak of a deadly virus has spurred moves, especially the sell-off in stocks and rally in bonds, for which many investors seemed ill-prepared. Even though the virus contagion has not peaked, the recovery in US equities yesterday points to a break the fear and anxiety.

FX Daily, March 17: Even Turn Around Tuesday is Flat

FX Daily, March 17: Even Turn Around Tuesday is Flat

Overview: While the markets are not as disorderly as they have been, the tone is fragile, and the animal spirits have been crushed. Australian stocks fell more than 10% last week and dropped another 9.7% yesterday before rebounding by almost 6% today to be one of the few Asia Pacific equity markets to rise. The Nikkei eked out a small gain, but the broader Topix rose 2.6%.

Tags: #USD,economy,Featured,federal-reserve,newsletter