– Four key themes to drive gold prices in 2018 – World Gold Council annual review– Monetary policies, frothy asset prices, global growth and demand and increasing market access important in 2018 – Weak US dollar in 2017 saw gold price up 13.5%, largest gain since 2010– “Strong gold price performance was a positive for investors and producers, and was symptomatic of a more profound shift in sentiment: a growing recognition of gold’s role as a wealth preservation and risk mitigation tool” – China’s gold coins and bars market recorded its second-best year ever– German, central bank and technological demand supporting gold prices– Latest Goldnomics podcast explores these and other themes Editor: Mark O’Byrne Annual

Topics:

Mark O'Byrne considers the following as important: Daily Market Update, Featured, GoldCore, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

– Four key themes to drive gold prices in 2018 – World Gold Council annual review

– Monetary policies, frothy asset prices, global growth and demand and increasing market access important in 2018

– Weak US dollar in 2017 saw gold price up 13.5%, largest gain since 2010

– “Strong gold price performance was a positive for investors and producers, and was symptomatic of a more profound shift in sentiment: a growing recognition of gold’s

role as a wealth preservation and risk mitigation tool”

– China’s gold coins and bars market recorded its second-best year ever

– German, central bank and technological demand supporting gold prices

– Latest Goldnomics podcast explores these and other themes

Editor: Mark O’Byrne

| Annual Review 2017 has just been released by the World Gold Council (WGC) and it’s annual report on the gold market and the outlook for gold prices is fact based, comprehensive and well worth a read – especially the section ‘Market Outlook for 2018’.

2017 was a relatively quiet one for gold prices, which was surprising given the increasing tensions and turbulence going on in the rest of the financial and particularly political spheres. The World Gold Council’s comprehensive analysis strongly suggests that the set up for gold is very positive and we are on the verge of further gains in the coming years. This is also our own view which we expanded upon in the just released latest Goldnomics podcast (Episode 3). |

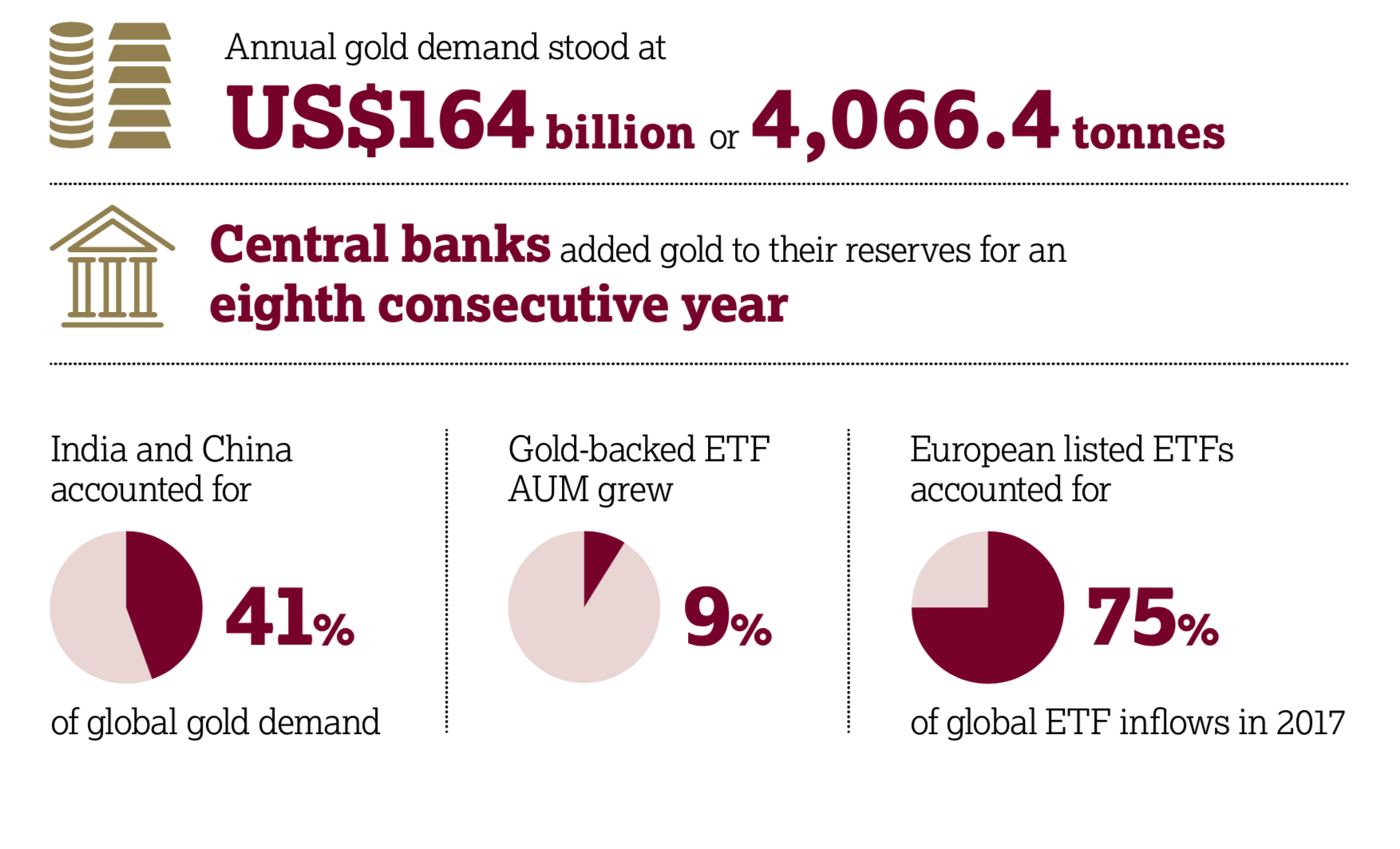

Annual Gold Demand, 2017 - Click to enlarge |

Gold demand fell slightly but supply was also down

2017 was a challenging year for gold demand: it fell to its lowest level since 2009. Investment and central bank demand accounted for most of the decline.

There were two interesting positive increases in gold demand in 2017; central banks and the technology industry. Whilst central bank demand did decline from the previous year, it was still notable.

According to the World Gold Council we are set to see both of these factors rise in 2018 which bodes well for gold prices.

Central banks continue buying as tensions rise between West and East

Last year made for the eighth consecutive year that central banks added to their gold reserves. As mentioned in our latest podcast this demand is high, but it could increase even more given the level of foreign exchange reserves.

Just this last week the news broke that the Russian central bank added a further 18 tonnes to their gold reserves. By way of reminder this is the bank that last year said it was stocking up on gold in order to “beef up national security.”

2017’s most notable central banks buying gold were Russia, Turkey and Kazakhstan. The former two having made some bold statements in recent times about protecting themselves from US dollar hegemony.

| China, Russia, Iran and more recently Turkey have made no secret of their desire to operate outside of the financial and monetary control mechanisms the U.S. has managed to control for so long. China (another major central bank buyer) is the most important in this regard but each of these countries have actively encouraged private gold ownership as well as national, in order to reduce their reliance on and exposure to the US dollar.

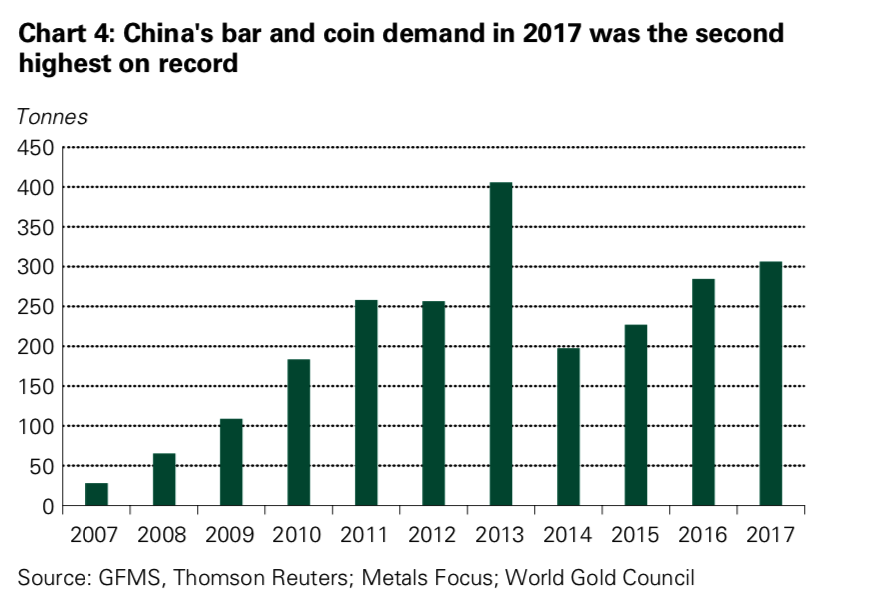

Interestingly, the WGC highlight China’s phenomenal gold buying record which rose again once again in 2017 to the second highest level on record. Geopolitical changes are seen as driving factors for the 2018 gold price by both the WGC and ourselves. The WGC draw particular attention to the sabre-rattling between North Korea and the United States. Whilst in our latest podcast we do touch on North Korea we also consider a number of factors including the ‘massive’ destabilisation of the Middle East. We discuss rising political tensions as well as what uncertainty and war mean for the gold price. Hint … increased safe haven demand. |

China Bar and Coin Demand, 2007 - 2017 - Click to enlarge |

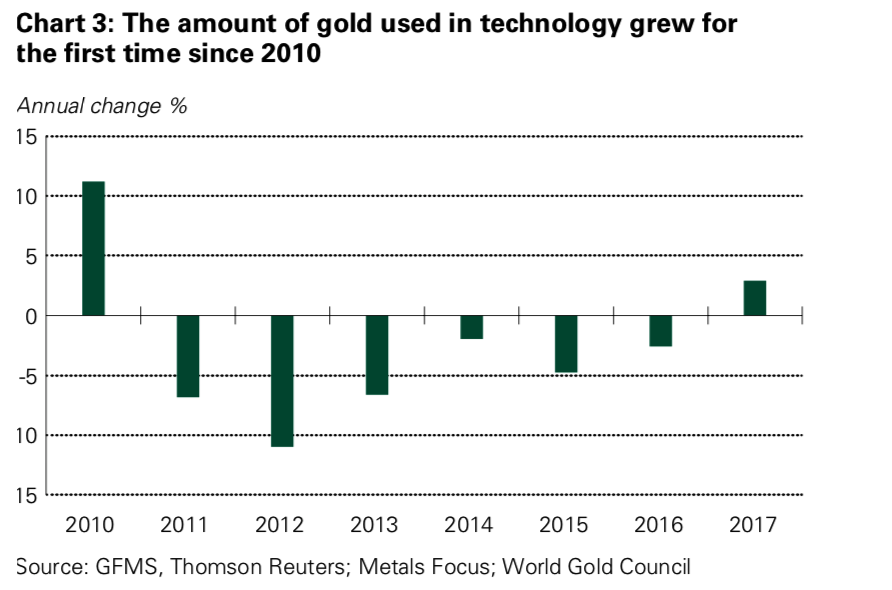

Tech demand for goldIn 2017 demand for gold in technology increased for the first time since 2010. The WGC expects this to be an ongoing trend as both the semi-conductor sector and gold nanoparticle-based technologies grow in popularity.

Back to Basics: Supply and DemandThe WGC look to synchronised global economic growth, monetary policy, frothy asset prices and market transparency and access including Sharia gold demand to drive the gold market into 2018. Monetary policy and frothy asset prices are those grabbing the headlines of late. It may be surprising to many investors but higher interest rates are good news for gold (as discussed here) whilst frothy asset prices could lead to yet another stock market crash and indeed another financial crisis. Investors should realise that cash can quickly turn to trash and how bail-ins are a very real threat today. However, it is the basics of supply and demand which are key to the price of gold in the long-term. The underlying fundamentals of gold, particularly on the supply side, and the advent of peak gold, help to underpin gold’s likely rise to $10,000 in the long term. |

Gold used in Technology Grew, 2010 - 2017 - Click to enlarge |

| Most commentators focus on the demand side of the gold market but we consider the supply side to be just as important. As discussed in our podcast we are seeing supply drop. According to this latest report from the WGC ‘Total supply [in 2017] fell 4% compared to 2016. Declines in recycling and hedging activity offset a modest rise in mine production.’

It is increasingly expensive to mine gold and there have been no major gold discoveries in recent years. How will this play out in the long term when gold demand has been increasing on average by 18% per year in recent years? Elon Musk’s grand plans to mine in space gets lots of headlines and uninformed press which misguided gold bears use to bolster their weak central thesis. In truth, mining gold on asteroids or on Mars is fake gold news. There is no real threat here to the gold market. Indeed, the notion of mining on other planets is laughable nonsense. It is not feasible today and if it does become feasible, the cost per ounce of “space gold” or “asteroid gold” will be hundreds of thousands of dollars if not million of dollars per ounce. We discuss many of the 2018 factors raised by the WGC in Goldnomics but expand into other areas, notably the key decisions and lessons investors must take in the current environment when it comes to protecting their assets and the importance of owning gold in the safest way possible. Not all types of gold are made equal. |

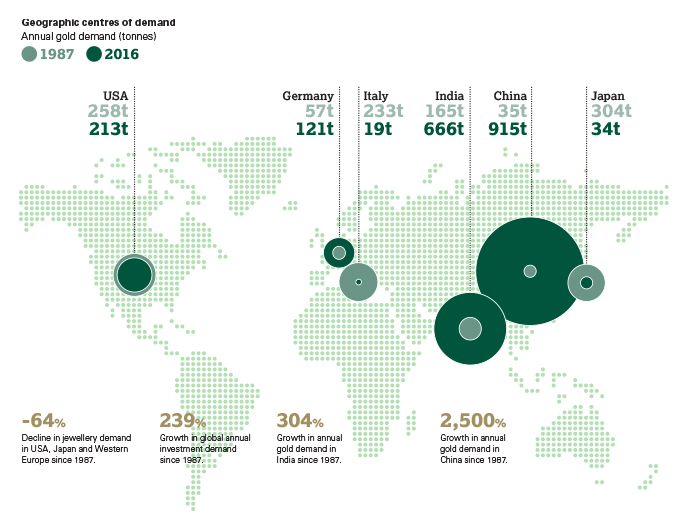

Geographic Centres of Demand, 1987 - 2016 - Click to enlarge |

Tags: Daily Market Update,Featured,newsletter