Policy errors have consequences, and we’re only in the first inning of those consequences. Please note: Of Two Minds subscription rates are going up this Friday 3/1/24 from /month or /year to /month or /year, so subscribe by Thursday if you want to lock in current rates. Thank you for understanding the necessity of adjusting rates that have been unchanged since 2011. If we ask, “what’s changed?,” two under-appreciated dynamics pop out: risk and consequences: risks are rising globally in a multi-dimensional self-reinforcing way, and the consequences of the Federal Reserve’s 14-year policy error known as ZIRP–zero interest rate policy–are finally manifesting in unwelcome ways. The Great Moderation is a term often invoked to describe the multi-decade

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Policy errors have consequences, and we’re only in the first inning of those consequences.

Please note: Of Two Minds subscription rates are going up this Friday 3/1/24 from $5/month or $50/year to $7/month or $70/year, so subscribe by Thursday if you want to lock in current rates. Thank you for understanding the necessity of adjusting rates that have been unchanged since 2011.

If we ask, “what’s changed?,” two under-appreciated dynamics pop out: risk and consequences: risks are rising globally in a multi-dimensional self-reinforcing way, and the consequences of the Federal Reserve’s 14-year policy error known as ZIRP–zero interest rate policy–are finally manifesting in unwelcome ways.

The Great Moderation is a term often invoked to describe the multi-decade reduction in global risks from 1990 to 2020. Geopolitical tensions diminished, the entry of China’s vast workforce and productive capacity lowered the costs of labor and production, effectively suppressing inflationary forces, and the financial markets responded by demanding less of a risk premium on the price of bonds and credit: a reduction in inflationary pressure and risk led to a gradual reduction in yields and interest rates.

Global risks are now rising, as are inflationary pressures. China’s inflationary monetary and fiscal policies have raised wages and costs, ending the era of China exporting deflation. The Federal Reserve’s 14-year suppression of interest rates to near-zero as it opened the floodgates of credit has finally generated consequences: inflationary pressures can no longer be put back in the bottle, for a variety of reasons, including unfavorable demographics, global changes in supply chains, resource depletion, and so on.

The Fed’s ZIRP policy error also inflated a series of asset bubbles, as those with access to the Fed’s nearly free money used this money to bid up income-producing assets, a decade-long behavior-modification program that incentivized rampant leverage and speculation which pushed asset prices into a parabolic rise.

This generated a “wealth effect,” long believed to be a core Fed goal: with household wealth soaring, the top 10% who owns the vast majority of the financial assets certainly feel richer. Those living paycheck to paycheck made use of lower interest rates to load up on debt: student loans, auto-truck loans, credit cards, etc.

Federal and local government spending also soared as public-sector borrowing skyrocketed. Super-low borrowing costs invited spending sprees, both public and private.

Now the economy is dependent on historically unprecedented low rates of interest or it collapse in a heap.

But the stagflationary forces unleashed by the Fed’s 14-year policy error cannot be suppressed; even worse, the Fed’s usual “fixes”–flooding the economy with liquidity and lowering rates–actually adds fuel to the stagflationary fires.

What few observers seem to grasp is the Federal Reserve is a closed system, which creates an illusion of godlike control as closed systems have limited inputs and processes, and so the output can be tweaked / controlled.

But the economy is an open, dynamic system, and rock-bottom yields and interest rates generate self-reinforcing feedback loops that generate forces beyond the Fed’s control. The Fed’s apparent control of yields and interest rates generated an illusory belief that the Fed could also control the consequences of their 14-year ZIRP policy error. This illusion is unraveling in real time, and the consequences cannot be controlled by lowering interest rates or flooding the financial sector with liquidity.

If stagflation and global risks continue to rise, the Fed will have to raise rates, not lower them. Or private capital will demand higher risk premiums regardless of what the Fed does, in effect forcing the Fed’s hand.

Note that rates are simply within a long-term range of between 3% and 5%. But even 5% rates are crushing the economy, a reality currently being masked by rapid expansion of public and private debt and the resulting doom spending–spending borrowed money like there’s no tomorrow.

But there is a tomorrow, and so leverage and speculations that only made sense in a ZIRP fantasy land will implode, popping the speculative mania asset bubbles generating the wealth effect. This will generate the dreaded reverse wealth effect in which the wealthy feel poorer and less motivated to borrow and spend freely.

Recall that every dollar that must be devoted to debt service (paying interest and principal) is a dollar that cannot be spent on consuming goods and services. So rising rates eventually crush consumer spending. Ironically, lowering rates will boost inflation, which has the same effect: the purchasing power of consumers’ wages plummets, reducing the quantity of goods and services they can afford to buy.

I’ve been writing about debt saturation for 15 years, and perhaps we’re finally seeing debt saturation take hold: debt saturation means borrowers have maxed out their capacity to borrow more: they lack the income and/or collateral to borrow more, and as rates rise, their spending declines accordingly. This is stagflation: no real growth yet prices continue to edge higher as risks and inflationary feedbacks continue apace.

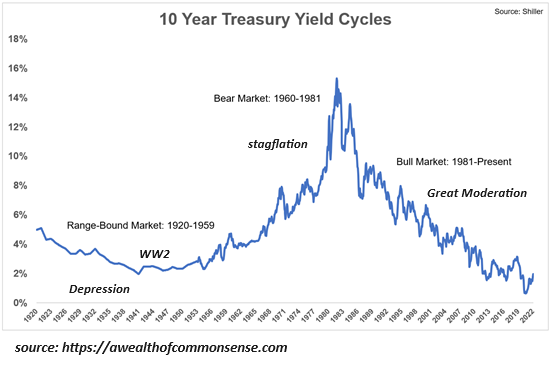

| In summary: policy errors have consequences, and we’re only in the first inning of those consequences. Here is long-term chart of 10-year Treasury bond yields. The Great Depression and World War II were both unique circumstances, and it is folly to use these as analogs supporting the illusion that rates can hover near zero forever. Note what happens when stagflation takes hold: rates rise, or inflation undermines the economy. There are no painless choices left. |

. |

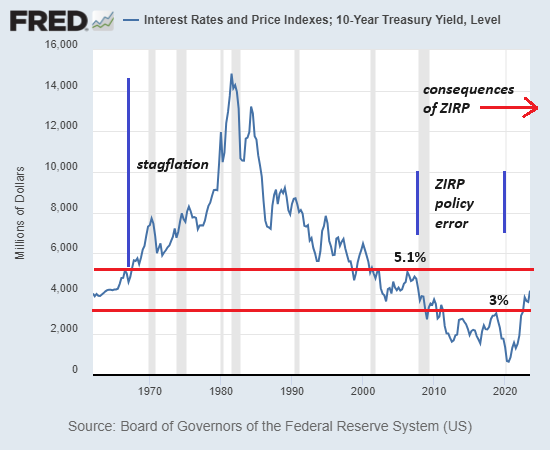

| Here we see the long-term range of 10-year Treasury bond yields, and how the Fed made a soon-to-be horrendously painful policy error in imposing ZIRP for 14 long years. |

. |

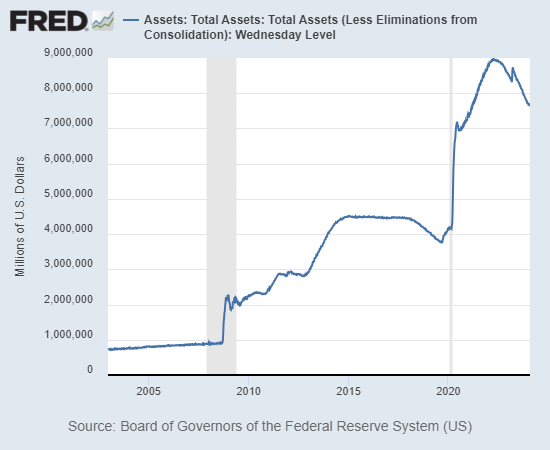

| Nothing to see here, just a 10-fold increase in the Fed’s balance sheet: |

. |

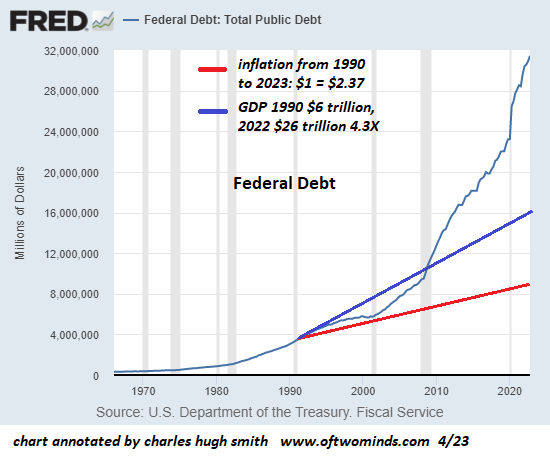

| Notice how federal debt took off in the era of ZIRP: free money, hey, might as well grab some and spend it. |

. |

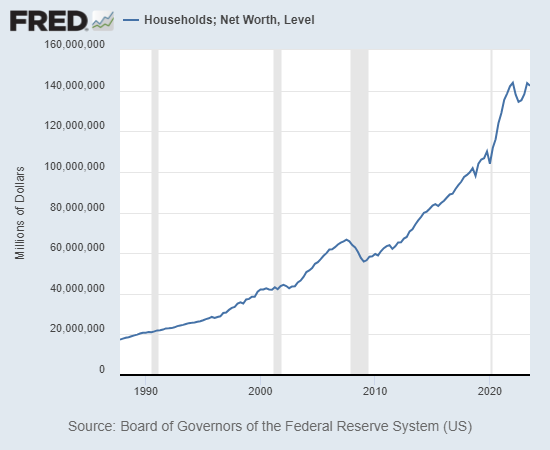

| The resulting speculative mania asset bubbles boosted household net worth: OK, so most of the gains went to the top 0.1%, top 1% and top 5%, but in aggregate it paints a pretty picture: everyone’s richer, thank you, Fed!

Thank you, Fed, for the coming decade of asset deflation, real-world inflation, debt saturation and the upward spiral of stagflation. Too bad the Fed’s levers only control behavior modification, not the real world. |

. |

Tags: Featured,newsletter