After consultation with the Swiss Financial Market Supervisory Authority (FINMA), the Swiss National Bank has submitted a proposal to the Federal Council requesting that the sectoral countercyclical capital buffer (CCyB) be reactivated. The buffer is to be set at 2.5% of risk-weighted exposures secured by residential property in Switzerland (cf. appendix). The SNB’s proposal envisages a deadline for compliance with the increased CCyB requirements of 30 September 2022. The Federal Council approved the SNB’s proposal on 26 January 2022. The SNB is herewith publishing the main reasons behind its proposal. In March 2020, against the backdrop of the coronavirus pandemic, the sectoral CCyB – which then stood at 2% of the relevant risk-weighted exposures – was

Topics:

Swiss National Bank considers the following as important: 1.) SNB Press Releases, 1) SNB and CHF, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

After consultation with the Swiss Financial Market Supervisory Authority (FINMA), the Swiss National Bank has submitted a proposal to the Federal Council requesting that the sectoral countercyclical capital buffer (CCyB) be reactivated. The buffer is to be set at 2.5% of risk-weighted exposures secured by residential property in Switzerland (cf. appendix). The SNB’s proposal envisages a deadline for compliance with the increased CCyB requirements of 30 September 2022. The Federal Council approved the SNB’s proposal on 26 January 2022. The SNB is herewith publishing the main reasons behind its proposal.

After consultation with the Swiss Financial Market Supervisory Authority (FINMA), the Swiss National Bank has submitted a proposal to the Federal Council requesting that the sectoral countercyclical capital buffer (CCyB) be reactivated. The buffer is to be set at 2.5% of risk-weighted exposures secured by residential property in Switzerland (cf. appendix). The SNB’s proposal envisages a deadline for compliance with the increased CCyB requirements of 30 September 2022. The Federal Council approved the SNB’s proposal on 26 January 2022. The SNB is herewith publishing the main reasons behind its proposal.

In March 2020, against the backdrop of the coronavirus pandemic, the sectoral CCyB – which then stood at 2% of the relevant risk-weighted exposures – was deactivated at the proposal of the SNB. The deactivation was made as part of a package of measures by the federal government, the SNB and FINMA and was aimed at giving banks maximum latitude for lending to companies.

The reasons that led to the sectoral CCyB being deactivated now no longer exist. The pandemic-related uncertainty with regard to companies’ access to credit has decreased significantly, thanks also to the measures taken by the authorities. There are no signs of companies experiencing a credit tightening.

However, the vulnerabilities on the mortgage and residential real estate markets have increased since the CCyB was deactivated. Both the volume of mortgage lending and prices for residential property have risen more strongly than can be explained by fundamental factors such as rents and income. Affordability risks have remained persistently high, and in the residential investment property segment they have continued to rise. A strong correction on these markets would have a noticeable impact on the banking sector and the Swiss economy.

The SNB has therefore concluded that a reactivation of the sectoral CCyB is necessary. In light of the now higher risks on the Swiss mortgage and real estate markets, banks’ capital adequacy is of great importance. A sectoral capital buffer of 2.5% – half a percentage point higher than before the deactivation in March 2020 – is thus justified.

The reactivation of the sectoral CCyB will lead to a temporary rise in the capital requirements for mortgage loans on residential property in Switzerland. This will first and foremost maintain the banking sector’s resilience, and strengthen it where necessary. In this way it is possible to limit the negative consequences of a strong correction on the Swiss mortgage and residential real estate markets for the banking sector and the Swiss economy.

The SNB will continue to monitor developments on the mortgage and real estate markets closely, and to assess whether further measures are necessary to mitigate the risks to financial

stability.

Appendix

Formal proposal to reactivate the sectoral countercyclical capital buffer

Under art. 44 of the Ordinance on the Capital Adequacy and Risk Diversification of Banks and Securities Firms (Capital Adequacy Ordinance, CAO), the Swiss National Bank may submit a proposal to the Federal Council to oblige banks to hold a countercyclical capital buffer (CCyB) in the form of Common Equity Tier 1 capital of a maximum of 2.5% of their risk-weighted exposures in Switzerland. The SNB submits such a proposal if this is necessary to strengthen the banking sector’s resilience to the risks of excessive credit growth, or to counteract excessive credit growth. The CCyB may be restricted to certain credit exposures.

On the basis of art. 44 CAO, and following consultation with the Swiss Financial Market Supervisory Authority (FINMA), the SNB proposes to the Federal Council that:

the sectoral countercyclical capital buffer be reactivated and that banks be obliged from 30 September 2022 to hold a countercyclical capital buffer amounting to 2.5% of their risk-weighted, direct or indirect mortgage-backed exposures as defined by art. 72 CAO that are secured by residential property in Switzerland.

You Might Also Like

BIS, SNB and SIX successfully test integration of wholesale CBDC settlement with commercial banks

BIS, SNB and SIX successfully test integration of wholesale CBDC settlement with commercial banks

2022-01-13

Project Helvetia looks toward a future with more tokenised financial assets based on distributed ledger technology coexisting with today’s systems.

Swiss National Bank expects annual profit of around CHF 26 billion for 2021

Swiss National Bank expects annual profit of around CHF 26 billion for 2021

2022-01-07

According to provisional calculations, the Swiss National Bank will report a profit in the order of around CHF 26 billion for the 2021 financial year. The profit on foreign currency positions amounted to just under CHF 26 billion. A valuation loss of CHF 0.1 billion was recorded on gold holdings. The net result on Swiss franc positions amounted to over CHF 1 billion.

Swiss balance of payments and international investment position: Q3 2021

Swiss balance of payments and international investment position: Q3 2021

2021-12-22

In the third quarter of 2021, the current account surplus amounted to CHF 24 billion, CHF 10 billion more than in the same quarter of 2020. The increase was mainly attributable to the significantly higher receipts surplus in goods trade. This surplus was due to traditional goods trade (foreign trade total 1), non-monetary gold trading, as well as to merchanting.

Monetary policy assessment of 16 December 2021: Swiss National Bank maintains expansionary monetary policy

Monetary policy assessment of 16 December 2021: Swiss National Bank maintains expansionary monetary policy

2021-12-17

The SNB is maintaining its expansionary monetary policy. It is thus ensuring price stability and supporting the Swiss economy in its recovery from the impact of the coronavirus pandemic. It is keeping the SNB policy rate and interest on sight deposits at the SNB at −0.75%, and remains willing to intervene in the foreign exchange market as necessary, in order to counter upward pressure on the Swiss franc.

Swiss National Bank, Banque de France and BIS conclude successful cross-border wholesale CBDC experiment

2021-12-09

Central bank digital currencies (CBDCs) can be used effectively for international settlements between financial institutions, as shown in the newest wholesale CBDC experiment concluded by the Swiss National Bank (SNB), the Banque de France (BdF) and the Bank for International Settlements (BIS).

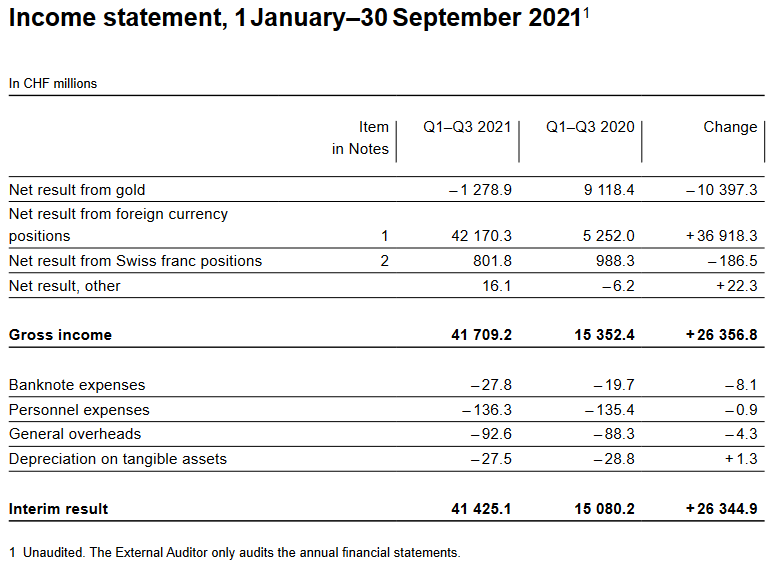

Interim results of the Swiss National Bank as at 30 September 2021

Interim results of the Swiss National Bank as at 30 September 2021

2021-10-29

The Swiss National Bank reports a profit of CHF 41.4 billion for the first three quarters of 2021. The profit on foreign currency positions amounted to CHF 42.2 billion. A valuation loss of CHF 1.3 billion was recorded on gold holdings. The profit on Swiss franc positions amountedto CHF 0.8 billion.

Mosambik-Kredite: FINMA schliesst Verfahren gegen Credit Suisse ab

Mosambik-Kredite: FINMA schliesst Verfahren gegen Credit Suisse ab

2021-10-20

Die Credit Suisse hat im Zusammenhang mit Kreditgeschäften aus dem Jahr 2013 mit Staatsunternehmen aus Mosambik schwer gegen das Organisationserfordernis und die geldwäschereirechtliche Meldepflicht verstossen. Die Eidgenössische Finanzmarktaufsicht FINMA schliesst in diesem Zusammenhang ein Enforcementverfahren ab und belegt das Kreditneugeschäft mit finanzschwachen Staaten der Credit Suisse mit Auflagen.

Swiss balance of payments and international investment position: Q2 2021

Swiss balance of payments and international investment position: Q2 2021

2021-09-23

In the second quarter of 2021, the current account surplus amounted to almost CHF 11 billion, CHF 7 billion higher than in the same quarter of 2020. The rise was mainly attributable to a higher receipts surplus in goods trade.

Tags: Featured,newsletter