With the monthly Friday Payroll Ritual lurking tomorrow morning, and having been focused on PMI estimates before it, a quick look at the ISM’s Non-manufacturing PMI especially its employment index to bridge the latter to the former. The update today for the month of December put the headline estimate at 62.0, down from 69.1 the month prior. Omicron? While a rather sharp and unexpected 7-point drop, other than the size of the decline at 62.0 there’s little to suspect anything really off. This one’s been the outlier anyway; even among sentiment indicators for services if not US services sentiment. . Compared to IHS Markit’s, for instance, the ISM is in a place by itself, though that hasn’t been anything unusual. Ever since around the end of 2017, the index has

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, economy, Featured, Federal Reserve/Monetary Policy, ism non-manufacturing, Markets, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| With the monthly Friday Payroll Ritual lurking tomorrow morning, and having been focused on PMI estimates before it, a quick look at the ISM’s Non-manufacturing PMI especially its employment index to bridge the latter to the former. The update today for the month of December put the headline estimate at 62.0, down from 69.1 the month prior.

Omicron? While a rather sharp and unexpected 7-point drop, other than the size of the decline at 62.0 there’s little to suspect anything really off. This one’s been the outlier anyway; even among sentiment indicators for services if not US services sentiment. |

. |

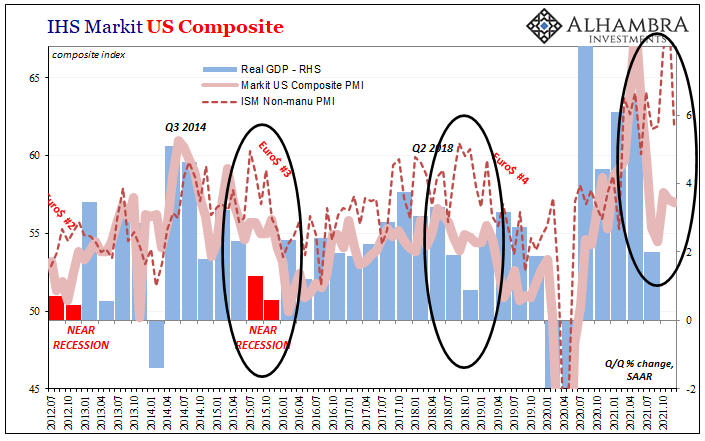

| Compared to IHS Markit’s, for instance, the ISM is in a place by itself, though that hasn’t been anything unusual.

Ever since around the end of 2017, the index has kept positioned perpetually elevated compared to its peers (below I’m showing it compared to Markit’s composite index, which includes that version of services sentiment along with manufacturing). The most glaring difference came in late in 2018 when other similar indications had already started lower for Euro$ #4’s globally synchronized downturn; the ISM NM among the tardiest to the synchronizing. It had actually performed similarly during the depths of Euro$ #3’s downturn, too. The index hit above 60 in July 2015 seemingly still on an upward trend even as the US part of the global economy was already mired in what would be a near recession; a downturn IHS Markit’s composite had already spotted coming the year before. |

. |

| Since this soft economic measure tends to be last to have reached each prior inflection, it calls into question the same divergence in recent months; and that’s on top of any unsettled issues with corona effects (both positive, as in reopening places, and negative, as in shutting down places again).

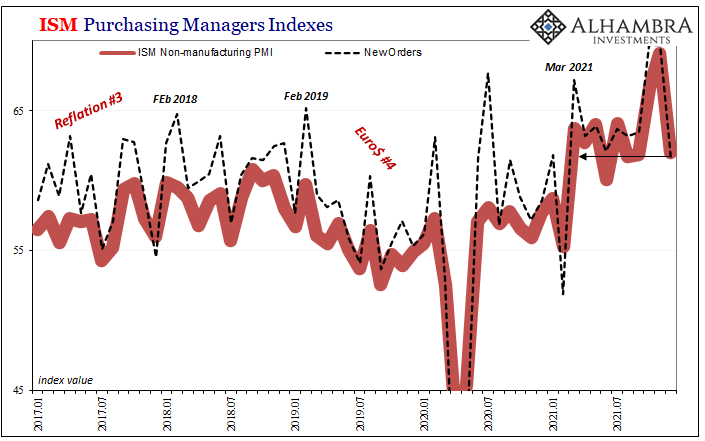

The New Orders segment was largely responsible for the headline miss, declining to 61.5 from 69.7 both October like November. Does it mean more that this index was still above 60 last month, or that at 61.5 this is the lowest since last February? |

. |

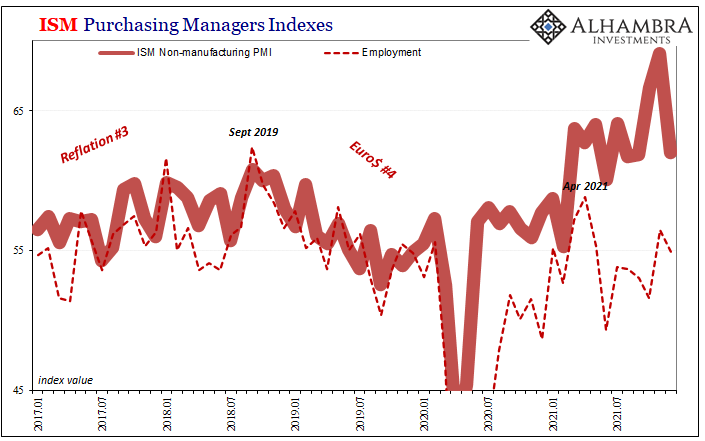

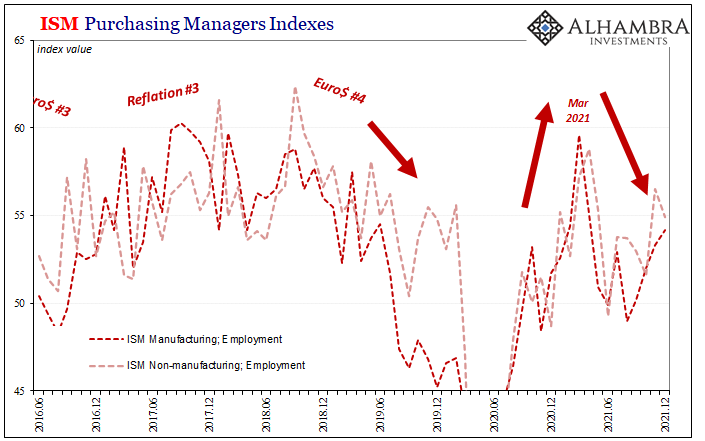

| Where I think it gets really interesting is the employment indicators; ISM’s for services as well as manufacturing. Neither have shown much improvement from earlier in the year, whether having dipped from the effects of delta COVID policies or other reasons. And for the non-manufacturing index, you can really see just how much the employment part of it has unusually lagged the overall headline during this post-2020 rebound.

It’s been in a different place altogether (above). Is this the alleged labor shortage? Perhaps, instead, businesses impacted by rising costs – one key reason why the headline index is so much higher – just aren’t able to pay the market-clearing wage for what is and would continue to be their largest input. In fact, even rebounding from mid-year, like a lot of these corona-impacted PMI numbers those in the latter half have been conspicuously less than what came up during 2021’s first few months up to around March and April. A brief peak before a possible if so far mild labor slowdown. |

. |

In fact, ever since April, the employment index for non-manufacturing has been more like 2019 or late 2015 than any other reflationary period.

With payrolls looming, it’s an interesting pre-release take on the employment situation from another perspective. As is the ISM Non-manufacturing overall which seems to be sticking with its historical biases, whatever you make of these December declines.

You Might Also Like

This Is A Big One (no, it’s not clickbait)

This Is A Big One (no, it’s not clickbait)

2021-12-02

Stop me if you’ve heard this before: dollar up for reasons no one can explain; yield curve flattening dramatically resisting the BOND ROUT!!! everyone has said is inevitable; a very hawkish Fed increasingly certain about inflation risks; then, the eurodollar curve inverts which blasts Jay Powell’s dreamland in favor of the proper interpretation, deflation, of those first two.

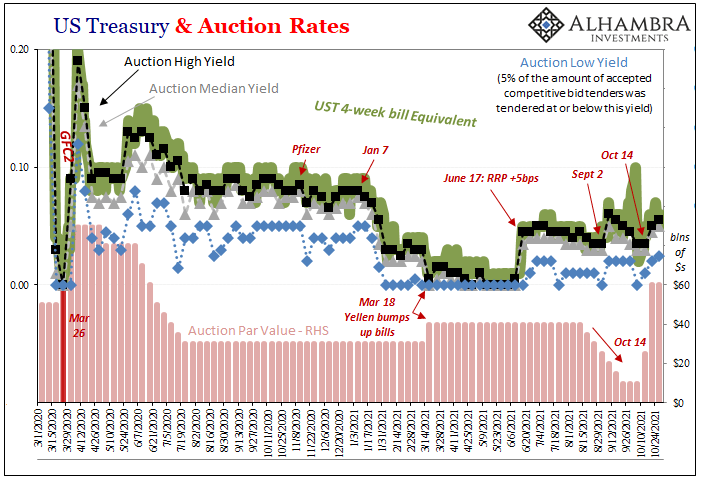

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

2021-11-02

Treasury Secretary Janet Yellen hasn’t just been busy hawking cash management bills, her department has also been filling back up with the usual stuff, too. Regular T-bills. Going back to October 14, at the same time the CMB’s have been revived, so, too, have the 4-week and 13-week (3-month). Not the 8-week, though.

An Anti-Inflation Trio From Three Years Ago

An Anti-Inflation Trio From Three Years Ago

2021-10-26

Do the similarities outweigh the differences? We better hope not. There is a lot about 2021 that is shaping up in the same way as 2018 had (with a splash of 2013 thrown in for disgust). Guaranteed inflation, interest rates have nowhere to go but up, and a certified rocking recovery restoring worldwide potential.

The Curve Is Missing Something Big

The Curve Is Missing Something Big

2021-10-21

What would it look like if the Treasury market was forced into a cross between 2013 and 2018? I think it might be something like late 2021. Before getting to that, however, we have to get through the business of decoding the yield curve since Economics and the financial media have done such a thorough job of getting it entirely wrong (see: Greenspan below).

Far Longer And Deeper Than Just The Past Few Months

Far Longer And Deeper Than Just The Past Few Months

2021-10-20

Hurricane Ida swept up the Gulf of Mexico and slammed into the Louisiana coastline on August 29. The storm would continue to wreak havoc even as it weakened the further inland it traversed. By September 1 and 2, the system was still causing damage and disruption into the Northeast of the United States.

Weekly Market Pulse: Perception vs Reality

Weekly Market Pulse: Perception vs Reality

2021-10-18

It was the best of times, it was the worst of times… Charles Dickens, A Tale of Two Cities Some see the cup as half empty. Some see the cup as half full. I see the cup as too large.

More About Less New Orders

More About Less New Orders

2021-10-03

The inventory saga, planetary in its reach. As you’ve heard, American demand for goods supercharged by the federal government’s helicopter combined with a much more limited capacity to rebound in the logistics of the goods economy left a nightmare for supply chains. As we’ve been writing lately, a highly unusual maybe unprecedented inventory cycle resulted (creating “inflation”).

Weekly Market Pulse: Buy The Dip, If You Can

Weekly Market Pulse: Buy The Dip, If You Can

2021-07-26

If you were waiting for a correction in stock prices to put some money to work, you got your chance last week. The Dow Jones Industrial Average was down nearly 1000 points at the low Monday and closed down 725, a loss of a little over 2%. The S&P 500 did a little better but closed down 1.5%.

Tags: currencies,economy,Featured,Federal Reserve/Monetary Policy,ism non-manufacturing,Markets,newsletter