When bubbles pop, it’s natural selection at its most unforgiving: “adapt or die,” and those who ignore or discount consequential asymmetries will have a very difficult time navigating the triage. After years of relative stability, it seems asymmetries, distortions and denial are playing out in unexpectedly destabilizing ways. These complex and often opaque dynamics are interacting with each other and reinforcing each other in difficult to predict ways. No wonder instability is the new stability. Asymmetry comes in many forms. Advantages and disadvantages, weaknesses and strengths–these terms describe asymmetry in terms of adaptive / selective pluses or minuses and in relative superiority or inferiority. Asymmetric dominance is not always an adaptive advantage, as

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

When bubbles pop, it’s natural selection at its most unforgiving: “adapt or die,” and those who ignore or discount consequential asymmetries will have a very difficult time navigating the triage.

After years of relative stability, it seems asymmetries, distortions and denial are playing out in unexpectedly destabilizing ways. These complex and often opaque dynamics are interacting with each other and reinforcing each other in difficult to predict ways.

No wonder instability is the new stability.

Asymmetry comes in many forms. Advantages and disadvantages, weaknesses and strengths–these terms describe asymmetry in terms of adaptive / selective pluses or minuses and in relative superiority or inferiority.

Asymmetric dominance is not always an adaptive advantage, as it nurtures a very dangerous over-confidence and hubris. Thus the many accounts of dominant tech companies being overtaken and consumed by small rivals whose asymmetric advantages were discounted or not recognized by the over-confident major power.

| This is the core concept in asymmetric warfare: turn the opponent’s dominance into a liability, and expose them to unexpected asymmetries they are unprepared to counter.

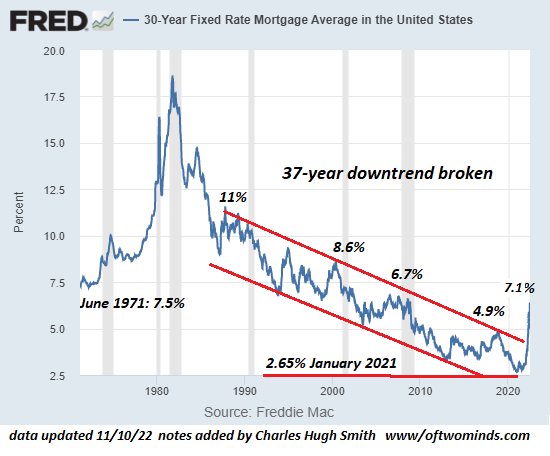

Then there are the stories of entities with asymmetric advantages which they fail to exploit, squandering opportunities to further or secure their dominance. There are also many accounts of apparent dominance resting on asymmetries of vulnerability in metrics such as training, pilot replacement, supply chains and various “glass jaws” which shatter on contact despite apparent superiority in quantity and quality. Distortions generate asymmetries of fragility as the pendulum eventually reaches a point where distorting forces can no longer advance or contain the inevitable snap-back as extremes revert to the mean and the pendulum swings to the other extreme: scarcities become gluts, etc. Denial plays a key role in furthering distortions and overplaying asymmetries. A common form of denying the risks of distortion is “this time it’s different,” but that doesn’t exhaust the human ingenuity invested in other forms of denial. Another common form is to remain confident that past dominance predicts the permanence of future dominance, when history suggests the opposite: hubris and passive over-confidence breed failure and collapse. Consider these dynamics in light of the global housing bubble. As the chart below shows, central banks suppressed interest rates (and thus mortgage rates) for decades as a distortion designed to foster growth. What it fostered were credit-asset bubbles and wealth/income inequality. Now the global housing bubble is popping as interest rates as distortions are never permanent. |

. |

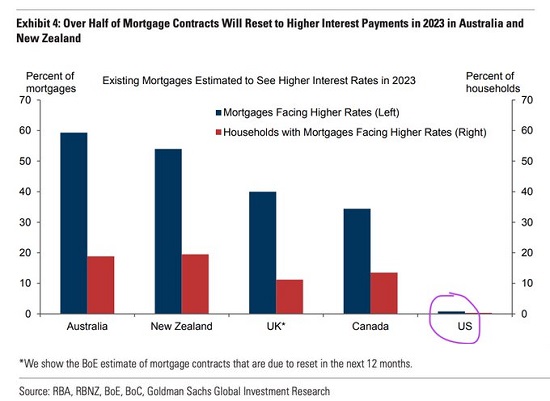

| As the second chart illustrates, the global housing bubble has numerous asymmetries, many of which are not yet recognized as being consequential. This chart displays the asymmetric dearth of mortgages in the U.S. that will adjust higher as rates rise and the consequentially larger share of mortgages in Australia, New Zealand, the U.K. and Canada that will adjust higher as rates rise.

The inevitability of the bubble popping was set aside (denial), while the financial distortions that inflated the bubble were deemed permanent. Beneath the confidence and faith in the permanence of distortions, asymmetries piled up, unrecognized or discounted. Now that the bubble is popping, those asymmetries will loom ever larger. The selective advantages of some asymmetries and the catastrophic fragilities created by others will play out in the years ahead. Some housing markets will deflate, others will crash. Some with stabilize and recover, some will cascade down to a new low and not recover. When bubbles pop, global capital flows tend to ignore ideologies, distortions and denial in favor of transparency, liquidity and stability. These global capital flows will fuel a new set of asymmetries that will reinforce the strengths of the most adaptable and the weaknesses of the least adaptable–the opaque, corrupt, sclerotic, illiquid. These asymmetries will become increasingly consequential, and only those who recognize the asymmetries for what they are will grasp the opportunities to escape doomed markets and situations and secure stakes in the most adaptable markets and situations. When bubbles pop, it’s natural selection at its most unforgiving: adapt or die, and those who ignore or discount consequential asymmetries will have a very difficult time navigating the triage. |

. |

Tags: Featured,newsletter