The market selloff into January rattled investors as concerns of “So Goes January, So Goes The Year” began to dampen expectations. Combined with a more aggressive stance from the Federal Reserve, rising inflation, and a reduction in liquidity, investor concerns seem to be well-founded. As discussed last week in “Passive ETFs Are Hiding A Bear Market,” the “blood bath” in the high-beta stocks is particularly humbling for the retail crowd that piled into risk with reckless abandon last year. “Probably one of the best representations of the disparity between what you see ‘above’ and ‘below’ the surface is the ARKK Innovation Fund (ARKK). While the S&P 500 index was up roughly 27% in 2021, ARKK is down more than 20%. That is quite a performance differential but

Topics:

Lance Roberts considers the following as important: 9) Personal Investment, 9a.) Real Investment Advice, Featured, Investing, newsletter, Technically Speaking

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The market selloff into January rattled investors as concerns of “So Goes January, So Goes The Year” began to dampen expectations. Combined with a more aggressive stance from the Federal Reserve, rising inflation, and a reduction in liquidity, investor concerns seem to be well-founded.

As discussed last week in “Passive ETFs Are Hiding A Bear Market,” the “blood bath” in the high-beta stocks is particularly humbling for the retail crowd that piled into risk with reckless abandon last year.

|

. |

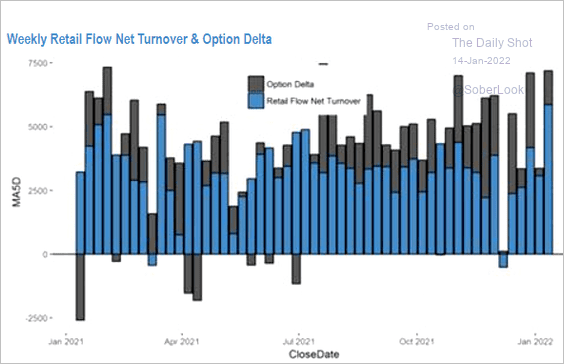

During the market selloff in the first two weeks of January, things did not improve for that group of stocks. However, retail traders have now set their sights on a new target: “value stocks.”

Despite the market selloff to start to the New Year, Wall Street continues to push overly optimistic projections of year-end returns. But, as noted, reality will likely be something entirely different. |

. |

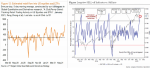

So Goes JanuaryFor now, let’s set aside assumptions of year-end outcomes and focus on the statistical evidence. From this analysis, we can potentially respect the risks that might lay ahead. According to StockTrader’s Almanac, the direction of January’s trading (gain/loss for the month) has predicted the course of the rest of the year 75% of the time. Starting from a broad historical perspective, the chart below shows the January performance from 1900. |

. |

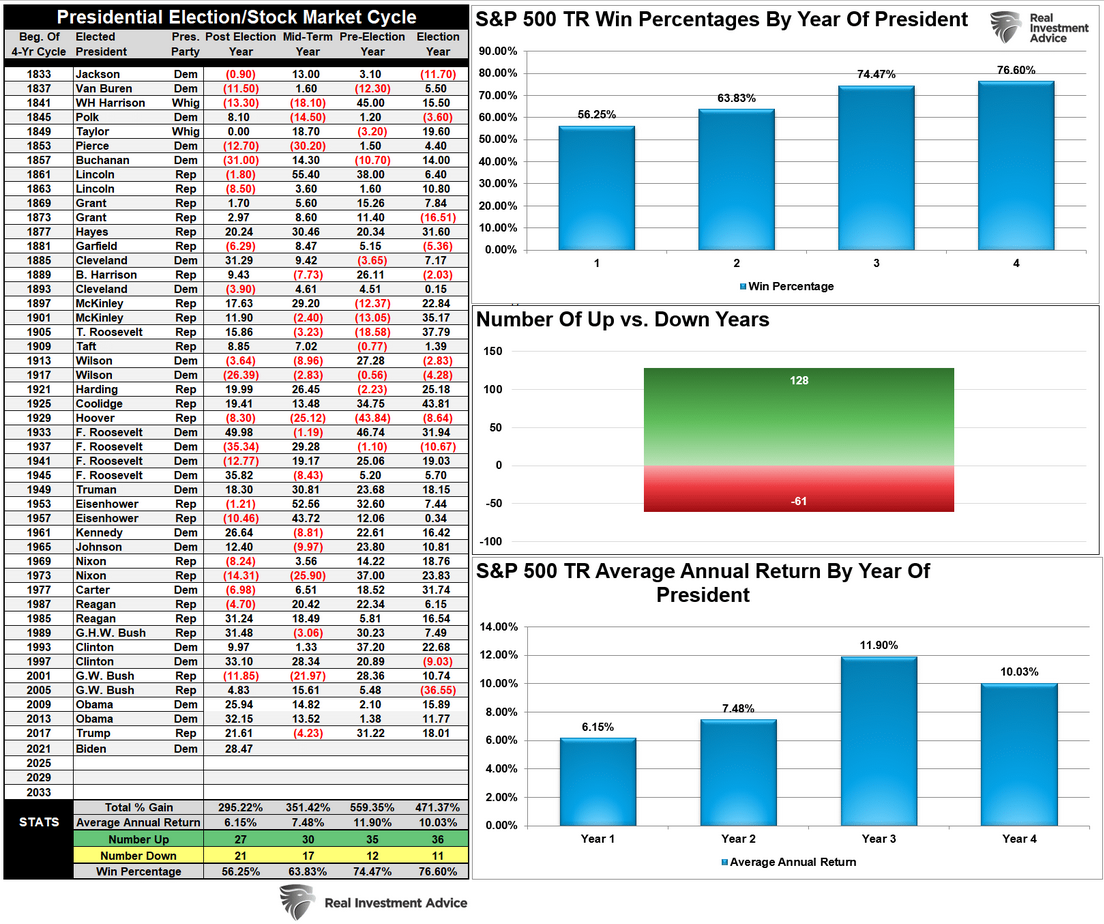

| Furthermore, thirteen of the last seventeen presidential election years followed January’s direction. Speaking of Presidential election years, the second year of the Presidential cycle statistically has the second-lowest average return rate with roughly a 63% chance of being a positive year.

Of course, unlike most years since 1980, this year, stocks will be dealing with the highest inflation rate since the late 1970s, excessively high valuations, and an aggressive policy change by the Fed. While that doesn’t necessarily mean poor outcomes for investors, it certainly increases the risk. |

. |

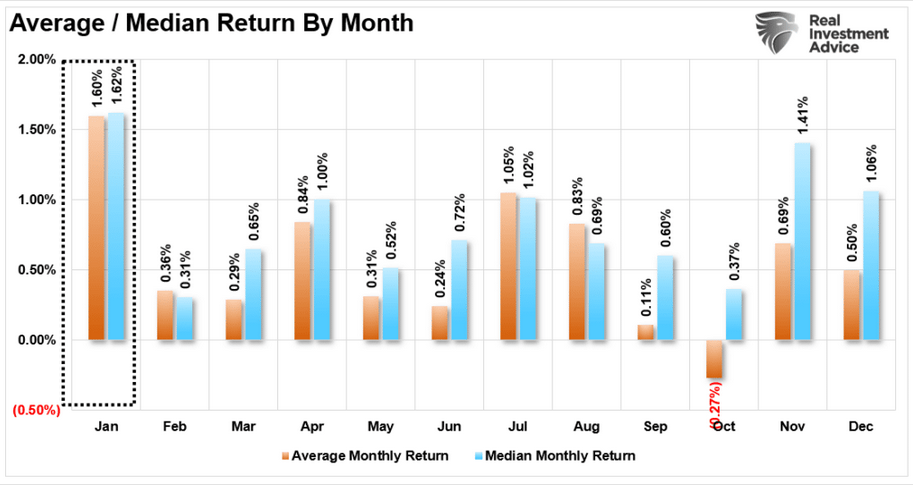

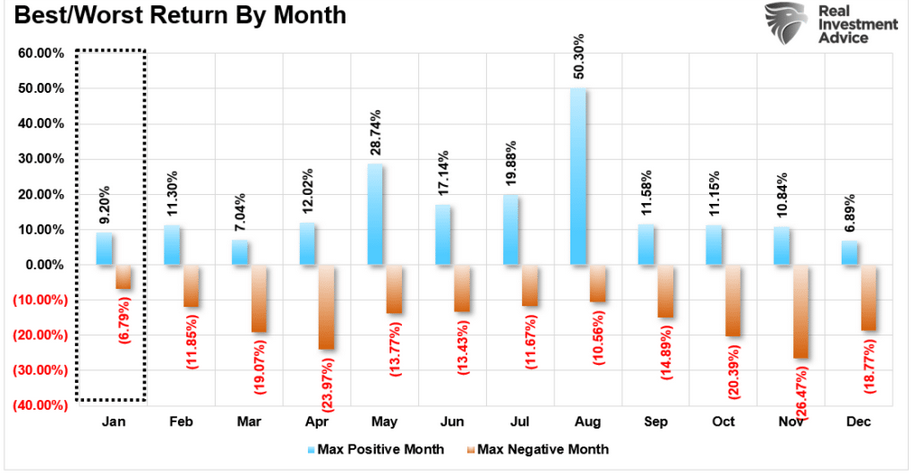

Digging InThe table and chart below show the statistics by month for the S&P 500. As you will notice, there are some significant outliers like August with a 50% one-month return. These anomalies occurred during the 1930s following the crash of 1929. |

. |

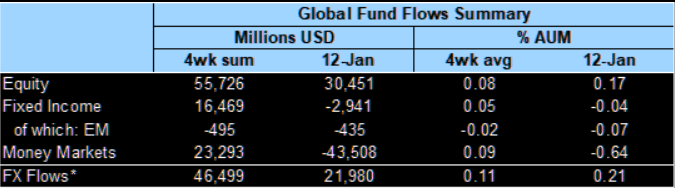

| The critical point is that January tends to be one of the best return months of the year. January also sees the most inflows into equities as asset managers put cash to work. Last week, Net flows into global equity funds remained strong (+$30bn vs +$26bn in the prior week). |

. |

| However, while fund inflows remain positive, January is significantly underperforming the long-term median and average, so far. |

. |

| While January also holds the title for the most favorable return months since 1900, followed only by December and April, negative returns occur about 33% of the time. Such is a high enough risk not to get ignored.

But January is not always a winner. While the statistical odds are high, it does not always end that way, even with a strong start. It is worth noting that while January’s maximum positive return is 9.2%, the maximum drawdown for the month was the lowest for all months at -6.79%. |

. |

| However, that is history. Let’s talk about where we are now. |

. |

A Rough StartAs noted, it has been a rough start to the new year so far as the market selloff caught investors off-guard. As shown below, the market failed to hold December’s gains, negating most of the “Santa Claus” rally. However, on Friday. the market successfully tested and maintained the lower trend line from last October. |

. |

| Risk is still prevalent. With sell-signals still intact, and the market not back to short-term oversold levels, there is still downside pressure on stocks.

As shown, the current correction has already retraced 38.2% of the rally following the October correction. A full correction would wipe out all of the gains since December by completing a 61.8% retracement. While not shown, the 200-dma currently resides around 4400 on the S&P index, which would encompass roughly a 10% correction from the peak. |

. |

| With earnings season kicking into gear this week, it would not be surprising for the market to hold current support, given that earnings should be reasonably robust. In addition, given we are looking at earnings for the 4th quarter of 2021, where there was still substantial liquidity in the system and the Fed was still highly accommodative. However, as we get into the later quarters of 2022, the support for earnings will fade considerably.

As noted in this past weekend’s newsletter:

|

. |

A Year Of ChallengesFrom the mainstream media’s view, expectations are high that 2022 will continue 2021. Maybe such will be the case. However, as we laid out just recently, many of the headwinds that supported the ramp in speculative behaviors have, or will, reverse in the months ahead. To wit:

The media is correct that “Fed rate hikes” won’t cause a bear market. As is always the case, the event that changes the “bullish psychology” is always unknown. However, the eventual market reversion is almost always a function of changes in liquidity and a contraction in earnings. Such was a point I made Friday on Twitter: The biggest problem for investors is the bull market itself. When the “bull is running,” we believe we are more intelligent than we are. As a result, we take on substantially more risk than we realize as we continue to chase market returns allowing “greed” to displace logic. Like gambling, success breeds overconfidence as the rising tide disguises our investment mistakes. Unfortunately, our errors always return to haunt us. Always too painfully and tragically as the loss of capital exceeds our capability to “hold on for the long-term.” |

. |

Conclusion

I have no idea what this year holds. Maybe it will be another wildly bullish year where throwing caution to the wind pays off once again.

Maybe, it won’t be.

The current market selloff, and rotation to value, may undoubtedly be essential clues. With market valuations elevated, leverage high, and economic growth and profit margins set to weaken, investors should be paying close attention.

Pay attention; things are beginning to get interesting.

The post Market Selloff Into January appeared first on RIA.

You Might Also Like

Build Back Better Bust: Why the spending package ISN’T paid for, as promised

Build Back Better Bust: Why the spending package ISN’T paid for, as promised

2021-11-17

Markets are quietly going sideways ahead of Thanksgiving; we’re looking for the potential for a Santa Claus Rally; Janet Yellen is wrong; Build Back Better Plan is not paid for; reinstatement of SALT deduction; Questions & Answers from Candid Coffee; Outlook for Taxes in 2022; where to best invest?

——

0:00 – Market Commentary: All is Quiet before Thanksgiving, but then…

8:14 – Tax Changes coming for 2022: The Truth About the SALT Deduction

17:39 – Where are the best places to invest in 2022?

28:22 – Asset Allocation in an Under-Performing Market

Hosted by RIA Advisors Chief Investment Strategist Lance Roberts, CIO, w Senior Advisor Danny Ratliff, CFP

——–

Our Latest "Three Minutes on Markets & Money:

Stocks or Bonds? How to Invest When Correlations are High" is here:

Crypto’s Crash and Stocks Head Higher

Crypto’s Crash and Stocks Head Higher

2021-11-17

“Crypto’s Crash,” says some financial news headlines. The reality is Bitcoin, Ethereum and others are down about 10-15% in the last few days. The word “crash” may seem appropriate to describe the sharp decline, except 10%+ moves in a matter of days is the norm, not the exception for crypto.

Being “Green” is Great – But Who’s Going to Keep the Lights On?

Being “Green” is Great – But Who’s Going to Keep the Lights On?

2021-11-15

Why we’re write-in voting for Elon Musk for President: It’s the economy, stupid; the Infrastructure Bill will exacerbate inflation; paying more to "be green" is running headlong into keeping the lights on; Christmas Tree saga continues; the Fed’s stock market valuation warnings–crying "uncle?"

——

0:00 – Is it Time for A Billionaire’s Tax?

11:43 – The Real Impact of Inflation: Being Green vs Having Lights

23:05 -The Fed’s Stock Market Valuation Warning

Hosted by RIA Advisors Chief Investment Strategist Lance Roberts, CIO

——–

Our Latest "Three Minutes on Markets & Money: Record Level of Call Options Out–and they’re expiring this week!" is here:

&list=PLVT8LcWPeAujOhIFDH3jRhuLDpscQaq16&index=1&t=1s

——–

Our previous show, "CPI is "en fuego" –What does it mean for

What Happens if You Retire in Debt?

What Happens if You Retire in Debt?

2021-11-12

Johnson & Johnson’s announced division into three entities offers interesting options for investors; what happens if you retire in-debt? Rosso’s Inflation Station Blues; Transitioning from portfolio accumulation- to withdrawal-mode in retirement; thrift philosophies of Grandma Rosso.

——

0:00 – What Opportunities Does a J&J split offer investors?

8:48 – What if you retire in debt?

10:55 – Richard Rosso’s Inflation Station Blues

20:38 – Shifting from Accumulation to Withdrawal Mode in Retirement

31:56 – Grandma Rosso’s Thrift Philosophy

Hosted by RIA Advisors Director of Financial Planning, Richard Rosso, CFP w Sr. Relationship Mgr., Jon Penn, CFP

——–

Our Latest "Three Minutes on Markets & Money: Markets Smacked Down by Higher Inflation" is here:

10 Smart Money Moves to Make Right Now.

10 Smart Money Moves to Make Right Now.

2021-10-28

2021 isn’t over yet. So here are 10 smart money moves to make right now.

Saving money should be a year-round endeavor, but life gets in the way just like anything else. So with 2021 coming to a swift, thankful end, take advantage of the fourth quarter to accelerate your financial acumen, bolster your balance sheet and successfully springboard into the new year.

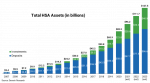

Tip One: Max Out HSA Contributions for 2021.

A Health Savings Account is a pre-tax savings miracle account. What other vehicle allows investors to sock money away triple tax-free? There’s no doubt HSAs have caught on with investors. According to Devenir’s latest survey, a national leader of investment solutions for Health Savings Accounts, the number of HSAs has now exceeded 30 million.

The popularity of HSAs

#MacroView: MMT – When Theories Collide With Reality

#MacroView: MMT – When Theories Collide With Reality

2021-08-08

Previously, we discussed Modern Monetary Theory (MMT) and its one limitation of inflation. However, as is always the case when “theories” collide with “reality,” the tenants of the theory are quickly discarded.

Technically Speaking: Hedge Funds Ramp Up Exposure

Technically Speaking: Hedge Funds Ramp Up Exposure

2021-08-03

The “Fear Of Missing Out” has infected retail and hedge funds alike as they ramp up exposure to chase performance. We have previously discussed the near “mania” of retail investors taking on exceptional risk in various manners. From increasing leverage, engaging in speculative options trading, and taking out personal loans to invest, it’s all evidence of overconfident investors.

The Delta-Variant Episode| The Real Investment Show (Full Show EDIT) 7/19/21

The Delta-Variant Episode| The Real Investment Show (Full Show EDIT) 7/19/21

2021-07-19

SEG-1: Markets Suffer Sell-off

SEG-2: This is not a Crash, a Correction

SEG-3: Investing vs Gambling: The Demise of Retail Investing

SEG-4: YouTube Q&A: Delta-variant Markets; What More Can the Fed Do?

——–

– Hosted by RIA Advisors Chief Investment Strategist Lance Roberts, CIO

——–

Articles Mentioned in this show:

https://realinvestmentadvice.com/knowledge-vs-experience-why-most-investors-wind-up-losing/

——–

Our previous episode on the new Child Tax Credits is here:

——–

Get more info & commentary:

https://realinvestmentadvice.com/newsletter/

——–

REGISTER for the next Candid Coffee on Financial Independence, July 24, 2021:

https://zoom.us/webinar/register/8516243846337/WN_GWlF7i_GRPSlWNs44_cm1g

——–

SUBSCRIBE to The Real Investment Show here:

Tags: Featured,Investing,newsletter,Technically Speaking