(Disclosure: Some of the links below may be affiliate links) Having a personal finance routine can help save time and money! For a lot of people, having a strict routine will help them remember essential things. It is the case for me. Each month, I am following the same personal finance routine for my budget. In this article, I am going to describe the steps I am doing every month. It is great to have a routine. It helps you get more efficient, and like this, you do not forget to do anything. And once you start doing it routinely, it becomes automatic, and you will save time. And time is your most important resource. And following a personal finance routine will help you avoid mistakes and maybe save money in the process! Of course, you do not need to follow the

Topics:

Mr. The Poor Swiss considers the following as important: 9) Personal Investment, 9) The Poor Swiss, Featured, Financial Independence, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

(Disclosure: Some of the links below may be affiliate links)

Having a personal finance routine can help save time and money! For a lot of people, having a strict routine will help them remember essential things. It is the case for me. Each month, I am following the same personal finance routine for my budget. In this article, I am going to describe the steps I am doing every month.

It is great to have a routine. It helps you get more efficient, and like this, you do not forget to do anything. And once you start doing it routinely, it becomes automatic, and you will save time. And time is your most important resource. And following a personal finance routine will help you avoid mistakes and maybe save money in the process!

Of course, you do not need to follow the same steps as me. You should probably not have the same steps. Every people can have different things to do based on the way they are investing or based on their situation.

But I would encourage you to define least a monthly routine clearly. You can use mine as a base template if you want. And why not even a weekly routine?

So, here are the 13 steps of my monthly personal finance routine.

1. Pay my monthly bills (after salary)

Once I receive my salary, the first of my personal finance routine steps is to pay my monthly bills for next month. I do this with the Neon mobile app.

These bills are my mortgage interests, taxes, insurances, credit card bills, and sometimes exceptional bills like Billag or some bi-annual bills. My salary goes into my checking account. I also receive some bills in my mailbox that I pay at the end of the month.

Why am I doing this first?

For the simple reason that I want to know how much I have left for next month. And I want to know how much money I can invest this month. I do not believe in the “Pay Yourself First” philosophy. It does not make any sense. If you save as much as you can, there will be something left to pay yourself. Pay yourself first makes you complacent, thinking you cannot save more.

2. Check my emergency fund

I always keep about two months of monthly expenses in my emergency fund. My emergency fund holds about 10’000 CHF.

I directly keep my emergency fund in my checking account. If you have access to high-interest savings accounts, you should use them instead. But in Switzerland, we do not get any interest in bank accounts.

So, once I have paid my monthly bills, I am checking how much I can move to my broker. I always keep about 10’000 CHF in my checking account. I invest everything higher than that. So, if I have 16’700 CHF left, I will invest 6’700 CHF this month. It cannot get simpler than that!

3. Invest my extra savings

Once I know how much I can invest, I directly transfer this money to my broker account. It generally takes one working day for the money to arrive at Interactive Brokers. After I receive the money in my broker account, I directly invest it. For instance, I can invest all the money in my VT ETF.

I am using the new amount to rebalance my portfolio. I am investing in the fund that is the most below its allocation. It is how I am doing balancing month by month. I never rebalance my portfolio. It is in check with my overall investment strategy.

Currently, the stock market is my only investment. But if I were to make other investments, I would split the money between the stock market and the alternatives.

4. Check my spending and budget

At the beginning of each month, I look back at the budget of the past month. I try to do this as early as possible, ideally on the first day of the month. I check every expense and earning for mistakes. Once I am sure of my expenses, I take note of my savings rate (can still change with the next two steps).

I am doing my budget in a straightforward way with multiple categories and an amount per category. What matters to me is that I have an accurate view of all our expenses.

And most importantly, I take a look at how much we spend on every category. I try to understand what went well and what did not go well. It will help me improving month after month.

If you aim to improve your budget a little each month, your budget will be much better after a year already!

5. Check my credit cards

I am also checking that all the expenses from my credit cards are in my budget. I also check every credit card expense for a possible mistake. Several times I forgot to add small expenses to my budget from my credit card. The biggest benefit is making sure that there are no errors or frauds on my credit card statements.

It is also an excellent time to check if I could buy more things with my credit card. Now that I have several credit cards, it is good to check if some expenses are not using the correct credit card. I want to minimize my fees as much as possible. And maximize the small bonus I get for spending with my credit card.

But if you want to keep it simple, you can also not bother with credit cards and use your bank cards! It will not make a huge difference.

6. Check all my accounts

After my credit cards, I check all my accounts. My goal is to get the current value of each of them.

Fortunately, I do not have many accounts. I have a checking account, one at Migros Bank and another one at Neon Bank. For each of my checking accounts, I verify all the transactions. I also make sure I have put each of these transactions in my budget. It is generally the only account that is moving significantly.

I also check my third pillar at VIAC and Finpension 3a. I also have an account at Interactive Brokers for my investment. I check the value of each of my investments. Once I have all these values, I can carry on to my next step.

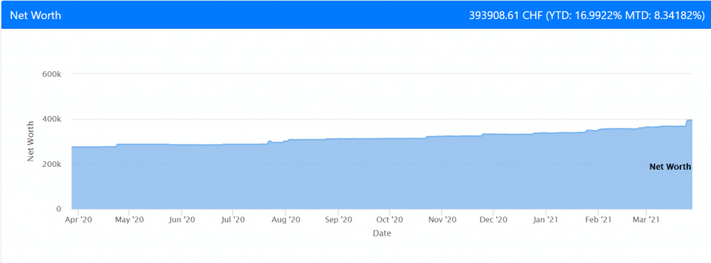

7. Update my net worthNow, I got the values of all my accounts and all my investments. It is time to put them together in my net worth tracking application. Once it is done, I get my new net worth! I can see how much the net worth increased (or decreased) compared to last month. I also keep track of how much my net worth grew from the beginning of the year. For me, these are important personal finance metrics to keep in mind. |

Our Net Worth as of March 2021 |

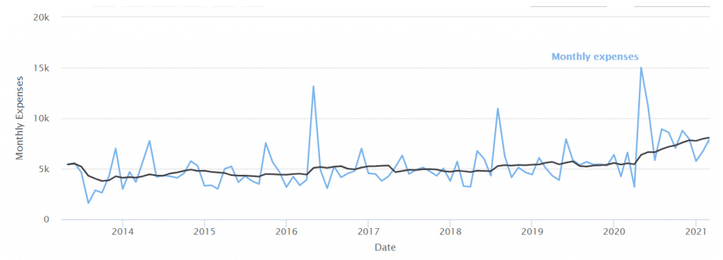

8. Keep track of the trendsOne thing I also like is to compare the trend of several things. In the previous step, I can compare the direction of my net worth. It should, of course, go up. But it should ideally accelerate its ascent. I also check the trend of my expenses. For instance, I keep track of the pattern of my expenses over time. One thing that is very important for me is the 12-months average. For example, for my expenses (in black): |

Expenses over time |

| Ideally, I would like the average to go down to 4500 CHF. But these days it is not great. I cannot even keep it below 5000 CHF. The average is more important than the value of each month. Because you may have some lousy months and some perfect months, but the average should stabilize. I am also checking the trend of my income. And very importantly, I am reviewing the trend of my savings rate. It is the most important trend for me.

Since I started to improve my finances in 2017, my average savings rate has been consistently going up. It is an excellent sign. I also check the rate of my income and earnings. Most of my income is very regular since it is my salary. But I also get some little income from this blog. And I like to check how earnings are going. |

Savings Rate over Time |

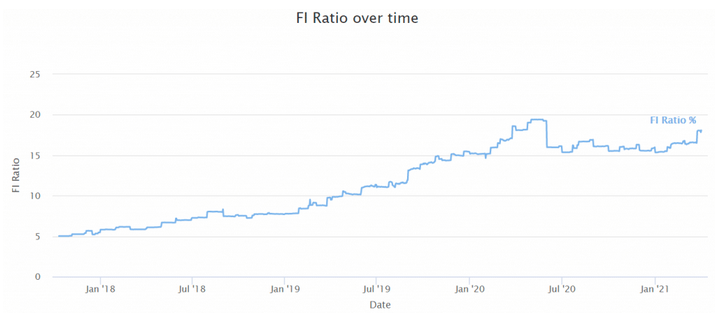

9. Check my Financial Independence (FI) RatioAfter I am done with all the data, it is time to get the final numbers out. I can check my savings rate, of course. And its trend as seen in the previous section. But the last value I am checking is my Financial Independence (FI) Ratio. This metric tells me how far away I am from being Financially Independent. I can also check the trend: My FI ratio should always go up. For now, it is increasing quite slowly. I am working on making it grow faster. But I am not stressed as to when I will be able to retire. Currently, our expenses are not yet very stable, so this causes our FI ratio to jump all over the place. |

FI Ratio over time |

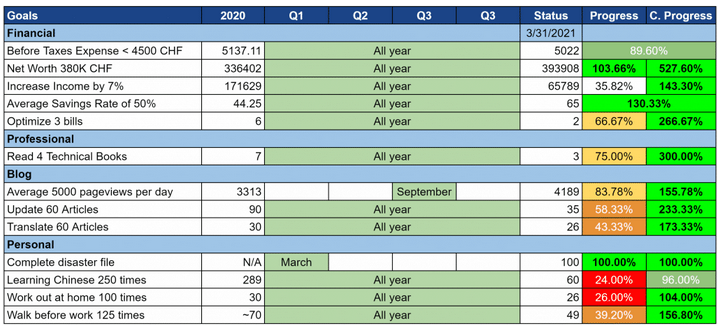

10. Update our goalsFinally, I now have all my numbers. It is time for me to check the current status of my goals. Every year, I try to set a few goals for the entire year. And every month, I am checking how the goals are going. For instance, here is one recent update of my goals. It helps me to have a good idea of where I am. It also helps me see what I should do better to reach my goals. |

Our Goals as of March 2021 |

11. Set next month goals

Once I have finished inspecting my yearly goals, I set a few goals for the next month. For instance, if I have spent too much one month, I set a very strict limit on spending in the following one. I am also setting soft goals such as:

- Research credit cards to find a better one

- Research bank accounts to find a better one

And so on. I try to put 4-5 goals for each month. I do not always report them on the blog. Generally, I write them down on a piece of paper.

And once I have my goals completed, I try to make a small plan of what I can do to improve my goals.

12. Study the analytics of the blog

This blog is my only side hustle. So, I am incorporating it into my monthly personal finance routine. If you have other side hustles, it would be good to check them every month as well.

I am checking how much traffic this blog got and comparing this to the previous month. I am using Google Analytics for this. If some pages are getting more traffic than usual, I am trying to understand why. And if the traffic is going down, I am also trying to understand why.

I am also checking if my blog consumes too much power on my hosting plan. I am using SiteGround to host this blog. Since I am using one of their cheap plans, I need to make sure I do not use too much. If I use too much, the decreased performance will impact the experience of the readers negatively. If it is too high, it means it is time to go to a higher hosting plan.

I also check the income I got during the month. But this is currently not my focus on the blog.

13. Post on the blog

Finally, my personal finance routine’s last item is to post my monthly report on this blog. If you do not have a blog, you may write a small report on your computer. Or you could keep track of the numbers for the next month.

For instance, you can check out the most recent monthly report. This post has the details of my expenses and income. It also contains the current status of my goals. And of course, some information about things that happened during the month. And my expectations for next month.

Why am I doing this?

I am mostly doing this for myself. I want to keep track of my financial status. I also believe it makes me more accountable. And it helps to keep me motivated. And since I like reading monthly reports, maybe some people will enjoy reading mine!

What I do not do

You may have seen that there are also some things I do not do.

First, even though I check the value of my funds, I do not plan any action for them. I do not want to sell or buy based on the price of the funds. I buy as soon as the money reaches my broker account. And I do not sell as long as I do not need the money. It is essential for long-term passive investing.

You have also have seen that my personal finance routine is entirely manual. I do not automate any of my money things. I think that automating your personal finances is a mistake. I much prefer to be in control.

Conclusion

Here you have it! My 13-steps monthly personal finance routine system!

Following this system helps me being very aware of what is going on with my finances. What is good and what is bad. I want to have as much information as possible with my budget. And I want to avoid missing a step. I very rarely make a money mistake with my personal finance routine. And since I do the same steps every month, I also save time.

These steps are personal. Of course, not everybody will have the same. However, I believe everyone should have a bit of a personal finance routine. Even with you have only a few steps, it helps to do them regularly and each month.

Enough about me! What about you? Do you have a personal finance routine? How many financial steps you do each month?

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-04-26

Update April 26 2021: SNB intervening. Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.2 bn. compared to last week.

How Much We Spent in 2020 – Full Expense Report

How Much We Spent in 2020 – Full Expense Report

2021-02-28

I keep track of all my expenses. And monthly, I publish my expenses on this blog. But once a year, I also a full analysis of my expenses for the past year. It helps me put things in perspective. And it also gives me an idea of where my expenses are going for an entire year.

Emergency Fund – Do you Really Need One in 2021?

Emergency Fund – Do you Really Need One in 2021?

2021-02-22

If you are interested in personal finance, you probably have come across the concept of emergency funds. An emergency fund is simply some money available directly that you can use for emergencies. Most people will advise you to get such an account. And they will insist heavily on this subject.

How to manage your finances as a couple?

How to manage your finances as a couple?

2021-02-16

Today’s post is a guest post by Yasi Zhang from Fast Track, talking about the very important subject of how to manage your finances as a couple. I am very happy to have her as a guest writer today.

The Simple Path to Wealth Book Review

The Simple Path to Wealth Book Review

2020-12-11

I have recently ordered a few more non-fiction books, and I have just finished The Simple Path To Wealth. This book was on my reading list for a very long time. The Simple Path To Wealth, by Jim L. Collins, is about investing simply to amass enough money to reach Financial Independence.

Free by 40 in Switzerland – Book Review

Free by 40 in Switzerland – Book Review

2020-11-27

I just finished reading Free by 40 in Switzerland, a book about financial independence, in Switzerland, by fellow blogger Mr. Mustachian Post, alias Marc Pittet. Mr. MP was kind enough to send me a version that I could review before the release date. So I can have this review ready now that the book is available!

The 4 Stages of Wealth

The 4 Stages of Wealth

2020-11-25

During your financial life, you will go through several stages of wealth. Maybe you have already crossed several of them, or maybe you are at the first stage of wealth. Regardless of where you are, it is important to know what is ahead and prepare for your future stages of wealth. There are many things you can do to prepare your future financial stages.

What is The Best Credit card in Switzerland for 2020?

What is The Best Credit card in Switzerland for 2020?

2020-11-24

A credit card is a powerful personal finance tool. But it is only a good tool if used correctly. And unfortunately, many people are not using credit cards correctly. The first important thing is to choose a card with no annual fee. You should focus on that first.

Tags: Featured,Financial Independence,newsletter