But when the Fed’s fundamental powerlessness is revealed and the buy-the-dippers have been forced to liquidate, the true meaning of “mild” contagion will become apparent. Since I’d rather not be renditioned to a rat-infested, freezing cell in an unnamed ‘stan, I’m circumspect about viruses in general. (The WiFi signal is probably weak due to all the masonry walls and metallic torture devices, and as for the food–grilled rat, anyone?) My essay Virus Z: A Thought Experiment (July 1, 2021) encapsulates my thoughts on viruses (reading between the lines recommended). But as a punter–oops, I mean investor–I’m free to discuss risk and consequence in markets. Yes, yes, I know there’s there’s no risk “because the Fed,” but last I checked the Fed’s god-like powers

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

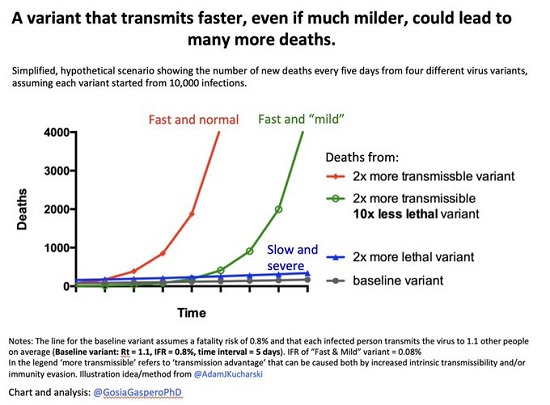

But when the Fed’s fundamental powerlessness is revealed and the buy-the-dippers have been forced to liquidate, the true meaning of “mild” contagion will become apparent. Since I’d rather not be renditioned to a rat-infested, freezing cell in an unnamed ‘stan, I’m circumspect about viruses in general. (The WiFi signal is probably weak due to all the masonry walls and metallic torture devices, and as for the food–grilled rat, anyone?) My essay But as a punter–oops, I mean investor–I’m free to discuss risk and consequence in markets. Yes, yes, I know there’s there’s no risk “because the Fed,” but last I checked the Fed’s god-like powers didn’t extend to the natural world, and so the chart below of how viral contagiousness can affect the consequences as measured in hospitalizations and deaths may be worth a glance. Note that the chart explicitly states that the data is a simplified, hypothetical scenario that isn’t based on any specific viral variant. It is a generalized depiction of the consequences of big numbers: a virus that is terrifically contagious but not terribly lethal (i.e. “mild”) still ends up killing far more people than the more severe but less contagious variants because the number of infected people becomes consequentially large very quickly. |

. |

To demonstrate the basic concept, consider a hypothetical Variant A that is only mildly contagious, i.e. each infected person ends up infecting 1.2 other people, but with high lethality, i.e. 1% of those infected die within a few months of contracting the pathogen.

If 10 million people eventually contract the disease, 100,000 (1%) will lose their lives.

Now consider a severely contagious Variant B, i.e. each infected person ends up infecting 3.5 other people, that is “mild” in terms of lethality, killing 0.5% of all those infected.

If this far more contagious variant eventually infects 100 million people, 500,000 will die–five times the number of those who died from the much more lethal variant A.

These outsized consequences of a highly contagious “mild” virus manifest not just in deaths but in hospitalizations and long-term disabilities generated by the viral disease.

Right now the stock market is wafting gently on the feel-good buzz of the word “mild”,

which is taken to mean not just mild consequences of the illness on individuals but near-zero consequences for the economy and markets.

It doesn’t take much imagination to project human behavior should a highly contagious variant start spreading with alarming speed through a population. Traveling in sealed metal tubes and ships and joining indoor crowds loses appeal, and risk-off precautionary behaviors take precedence over risk-laden “fun,” especially should the body count start climbing a few weeks into the “mild” contagion.

Any systems-level analysis should incorporate three principles: 1) ask cui bono, to whose benefit? For example, does what passes as “public health” in the U.S. actually benefit the many or does it mostly benefit the few reaping gargantuan profits from the system? 2) does maximizing the private gains of the few at the top of the power pyramid trigger immense losses for the powerless majority? and 3) what are the system’s constraints?

In healthcare, one constraint is the number of hospital beds and ICU facilities, and another is number of healthcare staff who have the requisite experience and energy to treat not just those suffering from the viral disease but all the patients with other conditions which can no longer receive care due to overcrowding.

Once the staff is burned out or ill themselves and the beds are filled, the system cannot treat any other patients, and care for those patients drops to near-zero. As I have noted many times here, the Fed can conjure dollars out of thin air but it can’t conjure well-trained doctors and nurses out of thin air, or new ICU units out of thin air.

Put another way, risk-off is also contagious and can spread very quickly, with very large consequences for assets based on the permanence of risk-on euphoria. Consider a simple example: passive index funds start getting redemptions, i.e. owners start selling the funds and ETFs.

Index funds and ETFs that hold a basket of stocks must sell all the equities that make up the index or ETF by proportional weight, so the most heavily weighted (i.e. Mega-Tech) stocks get hit the hardest by selling.

Since margin debt is at nosebleed levels, and much of this debt is leveraged on risk-on meme stocks and “can’t lose” Mega-Tech stocks, as these start slipping, margin calls start hitting punters who have only experienced brief dips that generate Pavlovian buy the dip recoveries within hours.

Selling at a loss–and being forced to liquidate positions that one intended to hold with diamond hands–will be a new experience.

Since the smart money already liquidated their positions while touting stocks at all-time over-valuations, there’s nobody left to buy as over-margined and over-leveraged retail punters are forced to sell.

Screaming that “this is the greatest company in the world” won’t stop that company from losing $1 trillion in market cap as its outsized heft in passive funds and ETFs causes mass liquidation as everyone tries to lock in profits at the same time.

As for the Fed, rising supply-side inflation is a systemic constraint for which the Fed has no answer, supply-side inflation which will only increase should harbors, etc. close down under the relentless spread of a highly contagious variant. If supply dries up faster than demand, inflation can double overnight and the Fed has zero power over the supply-chain constraints.

Those slavishly worshiping at the altar of the Fed will discover they have been worshiping false gods, and the karmic reversal of all that falsity and fraud will be both monumental and richly deserved.

The political blowback as the bottom 90% are eviscerated and hung out to dry by inflation will put the Fed’s usual financial trickery (free money for financiers and corporations) on the chopping block, and everyone who thought they had an easy field goal of gains will realize they’re now deep in their own end zone and several large, fast and very aggressive linebackers are chasing them down.

Risk off begets risk off, and once the “buy the dip” crowd runs out of cash and gets hit with margin calls, the leak of selling turns into a flood. Those with no experience of cascading declines will naturally hold on as their margin calls pile up, expecting the Fed to save the day or the buy-the-dippers to rescue everyone with yet another manic rally.

But when the Fed’s fundamental powerlessness is revealed and the buy-the-dippers have been forced to liquidate, the true meaning of “mild” contagion will become apparent, too late for those who thought being fully invested was a can’t-lose strategy.

You Might Also Like

Xi’s Gambit: China at the Crossroads

Xi’s Gambit: China at the Crossroads

2021-12-10

If Xi’s gambit succeeds, China could become a magnet for global capital. If success is only partial or temporary, China may well struggle with the structural excesses that are piling up not just in China but in the entire global economy.

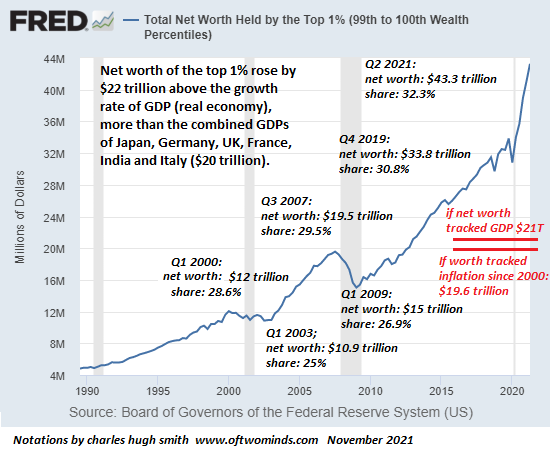

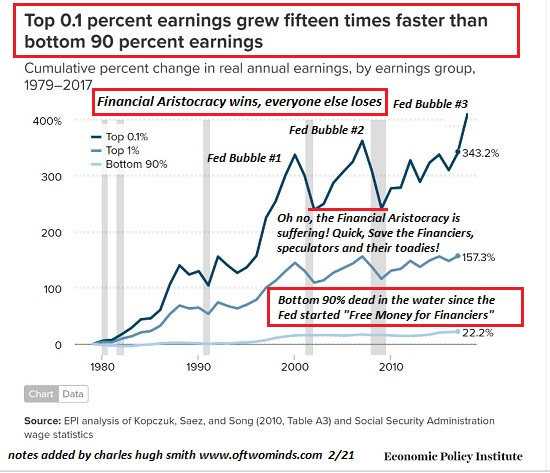

Top 1% Gains More Wealth Than the Combined GDPs of Japan, Germany, UK, France, India and Italy, Bottom 50%–You Get Nothing

Top 1% Gains More Wealth Than the Combined GDPs of Japan, Germany, UK, France, India and Italy, Bottom 50%–You Get Nothing

2021-11-18

Given that political power in America is a pay-to-play auction in which the highest bidder wins, how this incomprehensibly lopsided ownership of wealth plays out is an open question.

Eight Reasons Scarcities Will Increase Rather Than Evaporate

Eight Reasons Scarcities Will Increase Rather Than Evaporate

2021-11-09

Who knew it would be so easy? All we have to do is collect urine and we’ll be flying our electric air taxi tomorrow! While the private-jet crowd is busy selling a future of 1 billion electric vehicles, 1 billion windmills, 1 billion solar arrays, hundreds of thousands of electric aircraft, thousands of new nuclear power plants and trillions more in "wealth" accumulating in their bloated ledgers, reality is intruding on their technocratic fantasies.

Software Ate the World and Now Has Indigestion

Software Ate the World and Now Has Indigestion

2021-10-19

As for all those automated systems we have to navigate–do any of them work so well that those profiting from them actually use them? Of course not.

Have We Reached “Peak Self-Glorifying Billionaire”?

Have We Reached “Peak Self-Glorifying Billionaire”?

2021-07-22

Perhaps we should update Marie Antoinette’s famous quip of cluelessness to: “Let them eat space tourism.” As billionaires squander immense resources on self-glorifying space flights, the corporate media is nothing short of worshipful. Millions of average citizens, on the other hand, wish the self-glorifying billionaires had taken themselves and all the other parasitic, tax-avoiding, predatory billionaires with them on a one-way trip into space.

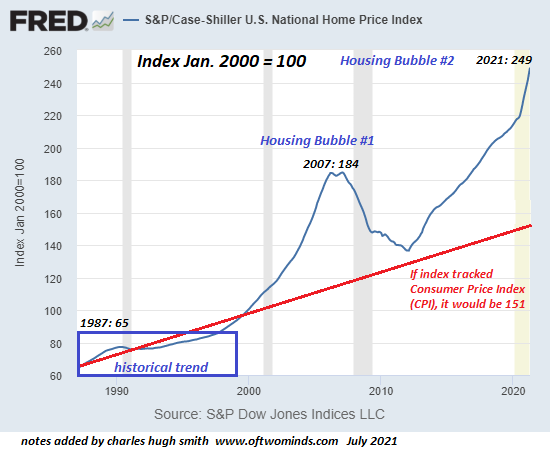

Housing Bubble #2: Ready to Pop?

Housing Bubble #2: Ready to Pop?

2021-07-10

The expansion of Housing Bubble #2 is clearly visible in these two charts of house valuations, courtesy of the St. Louis Federal Reserve database (FRED). The first is the Case-Shiller Index, which as you recall tracks the price of homes on an “apples to apples” basis, i.e. it tracks price movements for the same house over time. Note that this is an index chart where the index is set at 100 as of January 2000. It is not a chart of median housing prices.

Virus Z: A Thought Experiment

Virus Z: A Thought Experiment

2021-07-04

Let’s run a thought experiment on a hypothetical virus we’ll call Virus Z, a run-of-the-mill respiratory variety not much different from other viruses which are 1) very small; 2) mutate rapidly and 3) infect human cells and modify the cellular machinery to produce more viral particles.

When Expedient “Saves” Become Permanent, Ruin Is Assured

When Expedient “Saves” Become Permanent, Ruin Is Assured

2021-07-01

The belief that the Federal Reserve possesses god-like powers and wisdom would be comical if it wasn’t so deeply tragic, for the Fed doesn’t even have a plan, much less wisdom. All the Fed has is an incoherent jumble of expedient, panic-driven “saves” it cobbled together in the 2008-2009 Global Financial Meltdown that it had made inevitable.

Tags: Featured,newsletter