The “Fear Of Missing Out” has infected retail and hedge funds alike as they ramp up exposure to chase performance. We have previously discussed the near “mania” of retail investors taking on exceptional risk in various manners. From increasing leverage, engaging in speculative options trading, and taking out personal loans to invest, it’s all evidence of overconfident investors. However, that “risk appetite” is not relegated to retail investors alone. Professional managers, institutions, and hedge funds are “all in” as well. . Money Flows Are Huge The evidence of “professional investor” exuberance is the massive inflows of capital. The first half of 2021 outpaced every year since the Financial Crisis lows. . That surge in inflows came from a rotation of foreign

Topics:

Lance Roberts considers the following as important: 9) Personal Investment, 9a.) Real Investment Advice, Featured, Investing, newsletter, Technically Speaking

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The “Fear Of Missing Out” has infected retail and hedge funds alike as they ramp up exposure to chase performance.

We have previously discussed the near “mania” of retail investors taking on exceptional risk in various manners. From increasing leverage, engaging in speculative options trading, and taking out personal loans to invest, it’s all evidence of overconfident investors. However, that “risk appetite” is not relegated to retail investors alone. Professional managers, institutions, and hedge funds are “all in” as well. |

. |

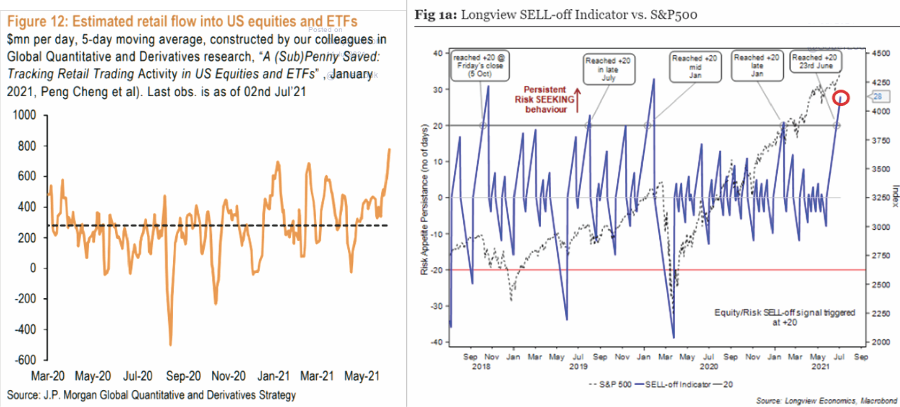

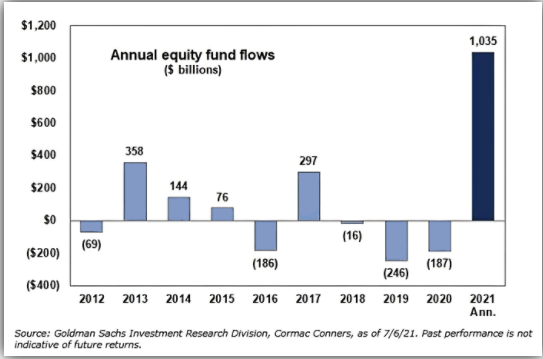

Money Flows Are HugeThe evidence of “professional investor” exuberance is the massive inflows of capital. The first half of 2021 outpaced every year since the Financial Crisis lows. |

. |

| That surge in inflows came from a rotation of foreign investors. The inflows are a function of expectations for more robust economic growth in the U.S. relative to their home country. The divergence in performance between the “Rest Of The World” and the U.S. represents the performance chase. |

. |

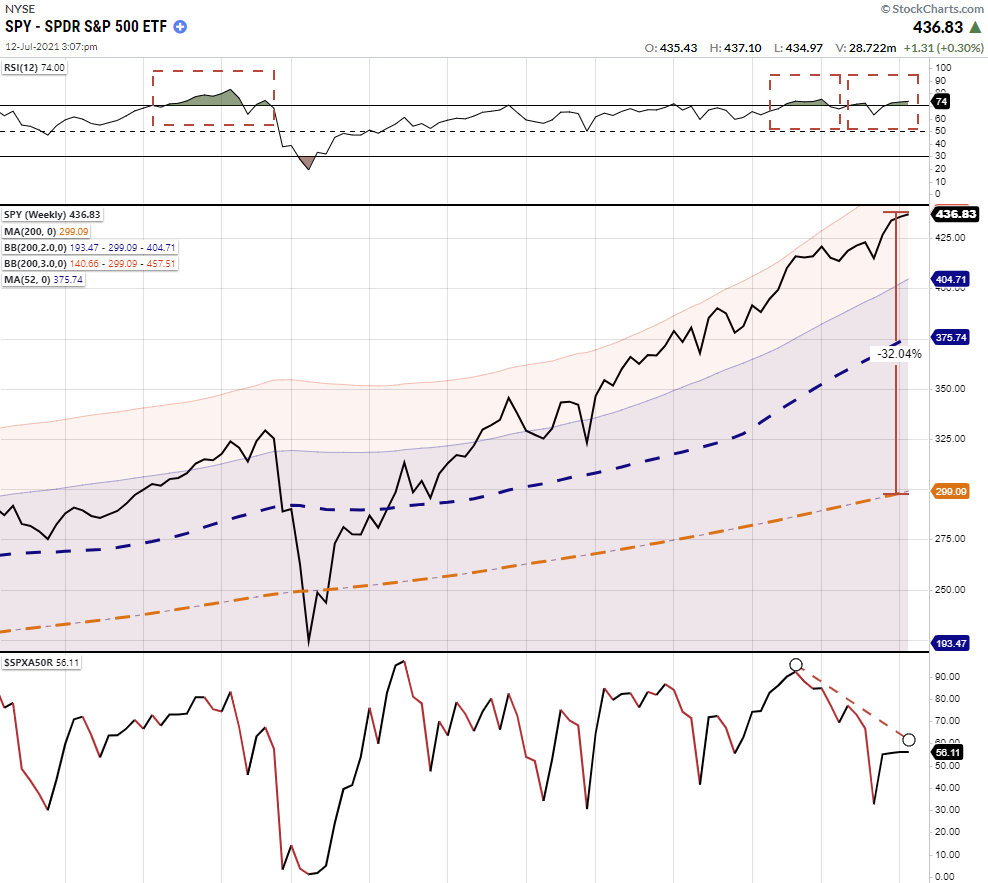

| One issue is the extreme overbought and deviated conditions of the U.S. market. Such conditions, when coupled with a deterioration of participation of stocks, remain a concern. (Bottom panel) |

. |

A Mental Formation

Nonetheless, given the $120 billion a month in “Quantitative Easing” by the Federal Reserve, it is not surprising to see the “performance chase” in action. As noted in “Market Will Soon Reach 4500,” it all comes down to the “psychology” of QE:

“The key to navigating Quantitative Easing! and Fed policy in general is to recognize that their effect on the stock market relies almost entirely on speculative investor psychology. See, as long as investors get inclined to speculate, they treat zero-interest money as an inferior asset, and they will chase any asset with a yield above zero (or a past record of positive returns). Valuation doesn’t matter because investors psychologically rule out the possibility of price declines in the first place.” – John Hussman

In other words, “Quantitative Easing” is a mental formation. Therefore, the only thing that alters the effectiveness of the Fed’s monetary policy is investor psychology itself.

Such was a point we made in the “Stability/Instability Paradox.”

“With the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the ‘instability of stability’ is now the most significant risk.”

Given professional managers are subject to “career risk,” they get forced to “chase performance.”

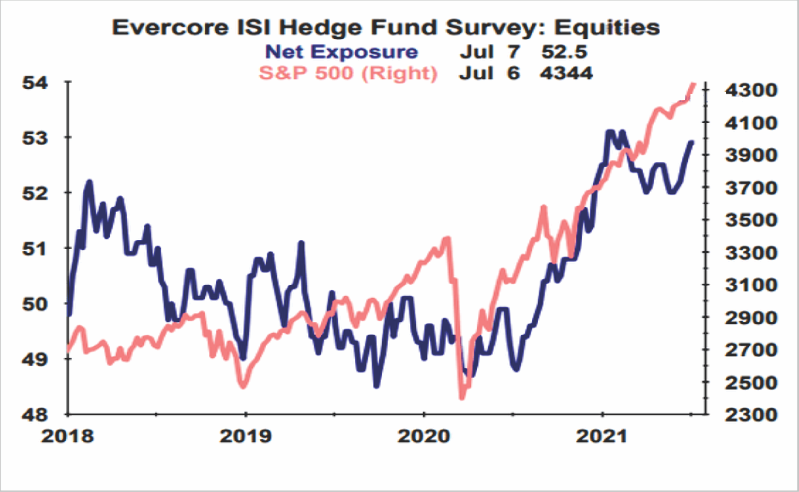

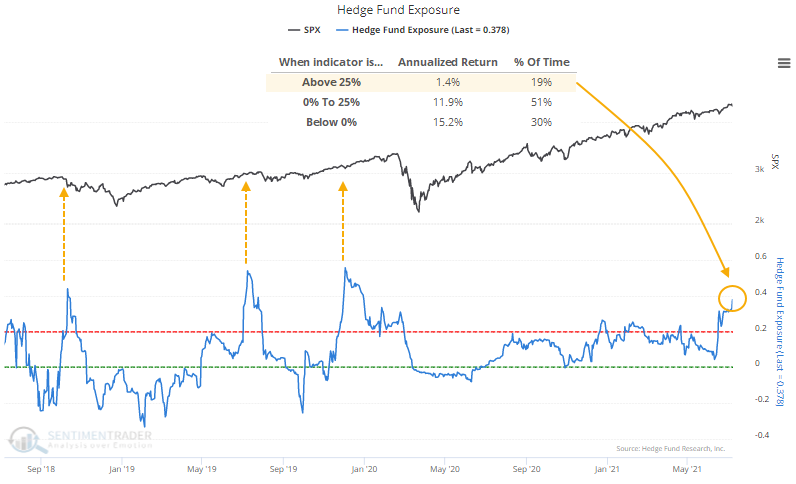

Hedge Funds Are All InHedge fund managers are now extremely long “risk” exposure. As stated, that “career risk” has professional managers chasing performance after suffering a rough start to the year. The need to make up lost ground, or risk losing assets to better-performing managers, rises with the market. Per the Wall Street Journal:

|

. |

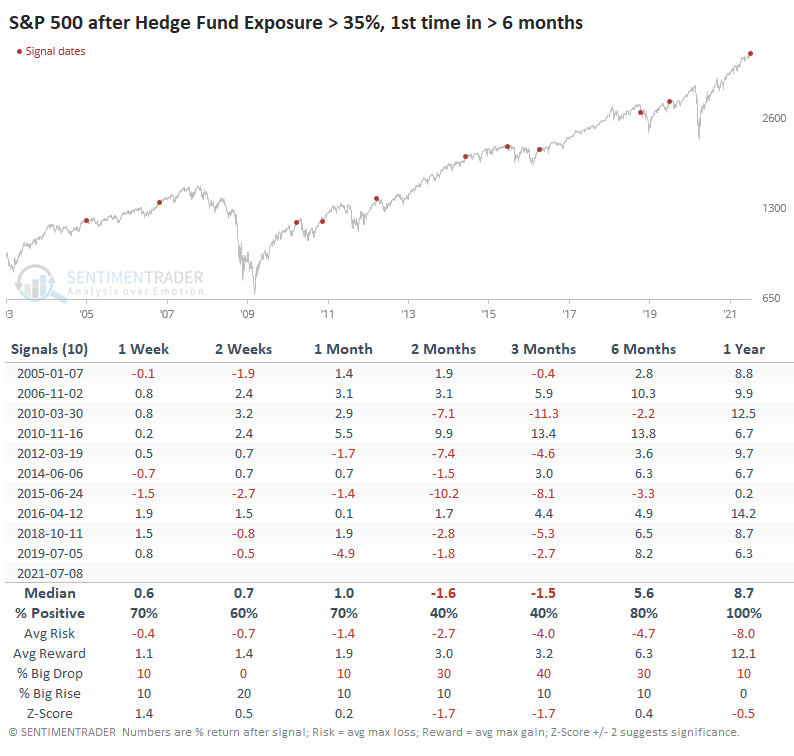

Sentiment Trader had an excellent piece of data to this point:

|

. |

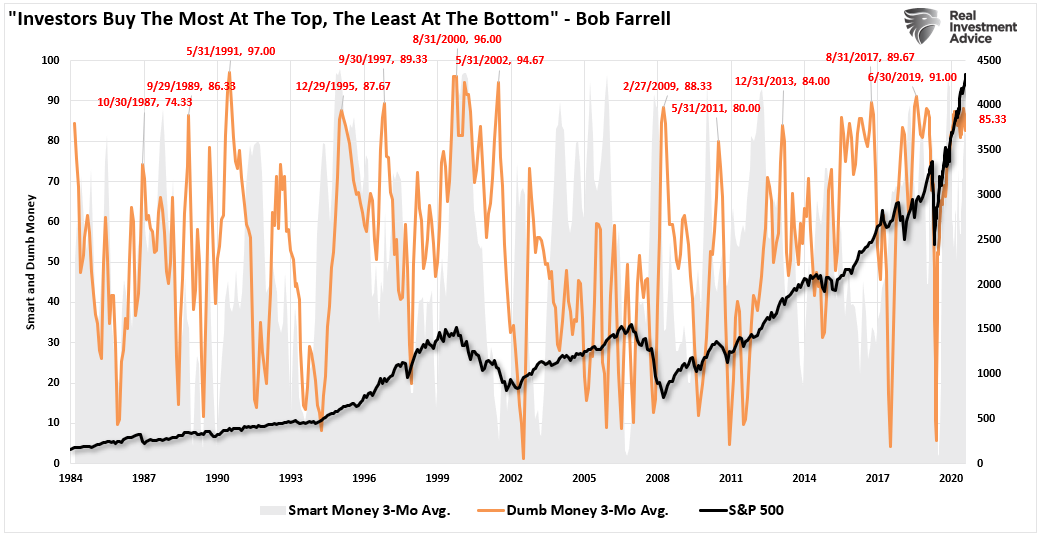

The point is that when professionals investors get “sucked” into performance chasing, it warrants being more “risk” aware. As Bob Farrell once quipped:

|

. |

Smart Vs Dumb MoneyNone of this should be of any surprise. After more than a decade of monetary interventions, the psychology of QE is now thoroughly ingrained. The problem eventually is that with investors very “long” the market, there will be few “buyers” when it comes time to sell. |

|

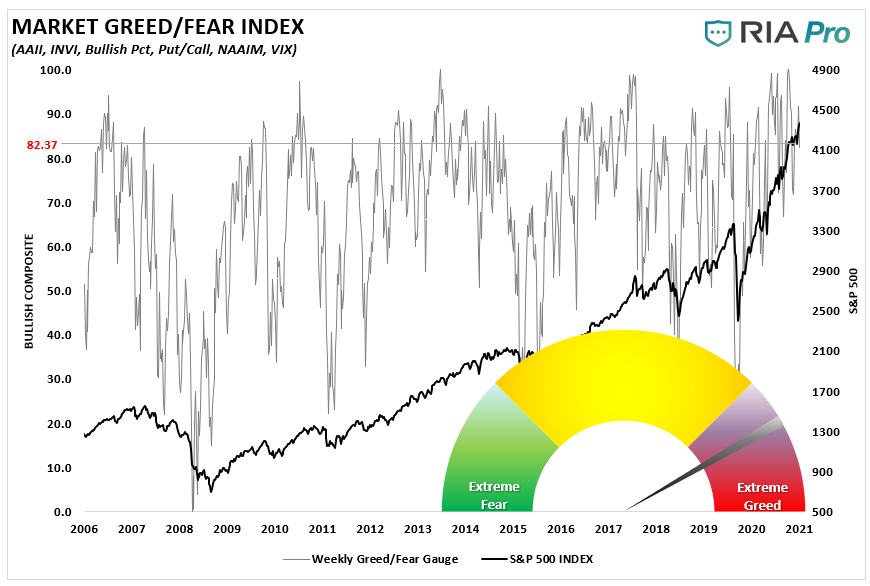

| The chart below combines investor positioning from both retail and professional investors. While there is room for investors to get even more exposed to “risk,” such levels have historically not lasted long or ended well. |

. |

As discussed in “There Is No Way, This Doesn’t End Badly,” virtually every measure of fundamental analysis suggests the markets are expensive.

However, in the short term, investors are trapped by the “fear of missing out.” While there is plenty of logic for sitting out of an overvalued, exuberant and stretched market, there is a consequence to “missing out.” While a bear market does indeed destroy capital, not participating in a bull market has an equal impact on ending results. It’s a terrible choice. |

. |

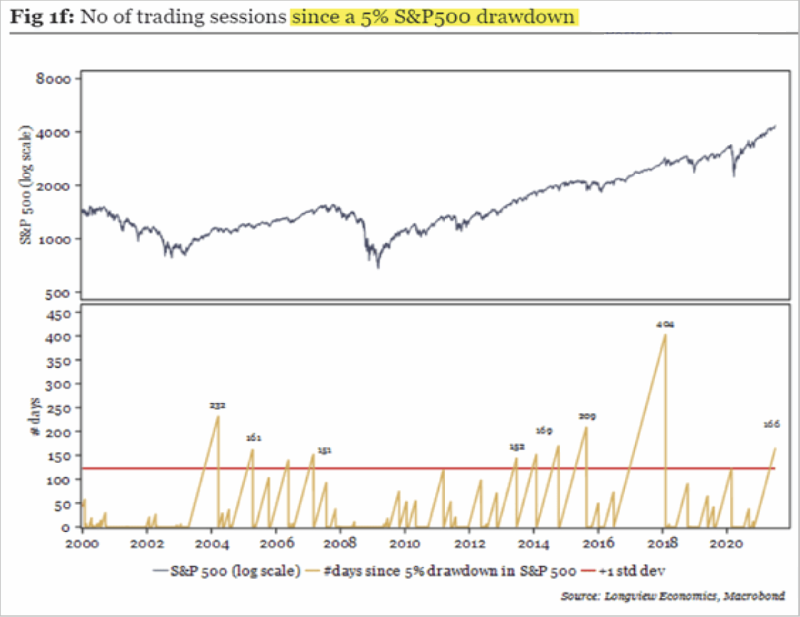

ConclusionA correction is coming. I have no idea when or what will cause it. However, the markets are currently in a very long advance without a 5% correction or more. So when it occurs, for whatever reason, it will “feel” worse than it is. That is due to the high level of complacency investors have developed in this market. While we are only expecting a correction in the near term, you cannot dismiss a “real bear market” either. It may not be today, next month, or even next year. But there is one truth in a market with all the signs of exuberance.

All bull markets die eventually. We never know the cause in advance. Ignoring history won’t make the damage any less catastrophic. Historically, we find that when both valuations and prices have extended well beyond their intrinsic long-term trendlines, subsequent reversions BEYOND those trend lines have ensued. Every Single Time. |

. |

Importantly, these reversions have wiped out a decade or more in investor gains. Think about this. If the next correction begins in 2022 and ONLY reverts to the long-term trendline, investors will reset portfolios to levels not seen since 2008.

A decade of gains will get wiped out.

Such tends to have a very negative impact on an individual’s retirement plans.

If you think that can’t happen, talk to anyone who was thinking about retiring in 2000 or 2008. I am sure they have an interesting story to share with you.

The post Technically Speaking: Hedge Funds Ramp Up Exposure appeared first on RIA.

You Might Also Like

The Lifeline of Markets – Liquidity Defined

The Lifeline of Markets – Liquidity Defined

2021-06-30

We recently read an analogy in which the author compares the current state of asset prices to an airplane flying at 50,000 feet. Unfortunately, we cannot find the article and provide a link. The gist is market valuations are flying at an abnormally high altitude. While our market plane cannot sustain such heights in the long run, there is little reason to suspect it will fall from the sky either.

Interview: Candid Coffee – Mid-Year Market Review

Interview: Candid Coffee – Mid-Year Market Review

2021-05-27

Last weekend, I joined Richard Rosso, CFP and Danny Ratliff, CFP to discuss the outlook for the markets for the rest of this year and take questions from our attendees.

2021-05-18

“The strong economic recovery will not get interrupted by inflation or a credit crunch, and the market will soon reach 4,500.” – Ed Yardeni via Advisor Perspectives. After discussing BofA’s view of why the market could drop to 3800, I thought it fair to discuss a more optimistic view.

Technically Speaking: If Everyone Sees It, Is It Still A Bubble?

Technically Speaking: If Everyone Sees It, Is It Still A Bubble?

2021-05-11

“If everyone sees it, is it still a bubble?” That was a great question I got over the weekend. As a “contrarian” investor, it is usually when “everyone” is talking about an event; it doesn’t happen.

As Mark Hulbert noted recently, “everyone” is worrying about a “bubble” in the stock market.

#MacroView: Are Stocks Cheap, Or Just Another Rationalization?

#MacroView: Are Stocks Cheap, Or Just Another Rationalization?

2021-05-07

Are stocks “cheap,” or is this just another bullish “rationalization.” Such was the suggestion by the consistently bullish Brian Wesbury of First Trust in a research note entitled “Yes, Stocks Are Cheap.” To wit:

“The Fed remains highly accommodative, there are trillions of dollars of cash on the sidelines, vaccines have reached over 50% of Americans, and the economy is expanding rapidly. Some valuations have been stretched, but the market as a whole remains undervalued. As a result, we remain bullish and are lifting our targets.”

Yes, it is true the Fed remains highly accommodative, which has undoubtedly pushed asset prices higher. In fact, financial conditions recently reached a historic low, which suggests elevated asset valuations ironically.

We have busted the “myth of cash on the

All Inflation Is Transitory. The Fed Will Be Late Again.

All Inflation Is Transitory. The Fed Will Be Late Again.

2021-05-02

In this issue of “All Inflation Is Transitory, The Fed WIll Be Late Again.“

Market Review And Update

All Inflation Is Temporary

The Fed Should Be Hiking Now

Portfolio Positioning

#MacroView: No. Bonds Aren’t Overvalued.

Sector & Market Analysis

401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

Market Review & Update

Last week, we said:

“The market is trading well into 3-standard deviations above the 50-dma, and is overbought by just about every measure. Such suggests a short-term ‘cooling-off’ period is likely. With the weekly ‘buy signals’ intact, the markets should hold above key support levels during the next consolidation phase.”

“As shown above, that is what is currently occurring. While

Seth Levine: Bitcoin Doesn’t Fix Defi, Defi Fixes Bitcoin

Seth Levine: Bitcoin Doesn’t Fix Defi, Defi Fixes Bitcoin

2021-05-02

Does Bitcoin Fix Defi (Definancialization)? “Bitcoin fixes this.” I cringe every time I see this popular meme. I find it worse than nails on a chalkboard. Bitcoin and other cryptocurrencies (crypto) supporters seem to wheel this tired trope out for every problem they see, particularly at economic ones. To their credit, they genuinely want to fix the financial system’s problems.

The Battle Royale: Stocks vs. Bonds (Which Is Right?)

The Battle Royale: Stocks vs. Bonds (Which Is Right?)

2021-04-28

The Battle Royale: Stocks vs. Bonds. The S&P 500 is at valuations higher than those in 1929 and rival those of 1999. Despite a recession, the index is 25% above where it was trading before the pandemic. The equity stampede is undoubtedly bullish about corporate earnings prospects and, by default, economic growth.

Tags: Featured,Investing,newsletter,Technically Speaking