Key Takeaways and Actionable Insights Consider these findings from a 2017 report from the G20 Global Partnership For Financial Inclusion, titled Alternative Data: Transforming SME Finance. Access to financing remains one of the most significant constraints for the survival, growth, and productivity of micro, small and medium enterprises (SME’s). Digital SME finance, using alternative data, offers an extraordinary opportunity for addressing…this problem. The world’s stock of digital data will double every two years through 2020. Every time SME’s and their customers use cloud-based services, conduct banking transactions, make or accept digital payments, browse the internet, use their mobile phones, engage in social media, buy or sell electronically, ship

Topics:

Hunter Hastings, Dusty Wunderlich considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Key Takeaways and Actionable Insights

Consider these findings from a 2017 report from the G20 Global Partnership For Financial Inclusion, titled Alternative Data: Transforming SME Finance.

Access to financing remains one of the most significant constraints for the survival, growth, and productivity of micro, small and medium enterprises (SME’s).

Digital SME finance, using alternative data, offers an extraordinary opportunity for addressing…this problem.

The world’s stock of digital data will double every two years through 2020. Every time SME’s and their customers use cloud-based services, conduct banking transactions, make or accept digital payments, browse the internet, use their mobile phones, engage in social media, buy or sell electronically, ship packages, or manage their receivables, payables and record-keeping online, they create digital footprints. This real-time and verified data can be mined to determine both capacity and willingness to pay loans.

A rapidly growing crop of technology-focused SME lenders are putting the use of SME digital data, customer needs and advanced analytics at the center of their business models, setting forth new blueprints for disrupting the SME lending status quo.

| The report refers to 800+ innovative digital SME lenders. Colloquially, we can refer to them as FinTech.

Dusty Wunderlich, a subject matter expert and seasoned investor in the FinTech field, discusses this lending landscape. Entrepreneurs need capital in the present to deliver goods and services to consumers and customers in the future.Entrepreneurs take scarce resources and apply them to what they believe the consumer will want at a future date. In order to do that entrepreneurs need capital in the present so they can deliver on those goods and services to the consumer in the future in the hope that their forecasting is correct. That’s why entrepreneurs need to understand capital financing and modern day capital markets.Access to capital has historically been difficult and expensive. Today, it’s becoming easier and less expensive, aided by the digital data revolution referred to in the report quoted above. It’s important for entrepreneurs to be familiar with the new field of FinTech and how to navigate it. |

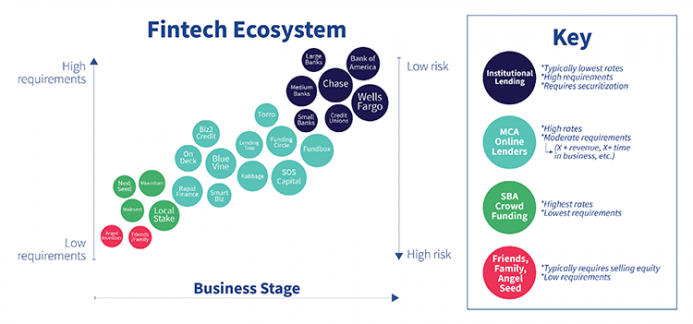

Fintech Ecosystem Download the full PDF graphic at Mises.org/E4E_63_PDF. - Click to enlarge |

Dusty Wunderlich suggests that entrepreneurs map out the financing alternatives on the axes of their own business stage versus the cost of capital.

Cost of capital refers not just to interest rates and fees, but to the requirements that lenders can impose on entrepreneurial borrowers. At the very earliest stages, “friends and family” lenders, angel investors and seed stage venture funds will all require equity stakes, and ratchet up those stakes via deferred interest and debt-to-equity conversion requirements. These early investors perceive themselves as taking a high amount of risk, and the start-up entrepreneur typically has little or no collateral or leverage in negotiation. The best negotiation stance is to generate competition among investors with the quality of the customer value proposition and the business plan and revenue model.

Fintech financing is now available at the earliest of entrepreneurial growth stages.

Today, from the very outset of the business journey, start-ups and small businesses can access a range of financing types – debt, convertible notes, equity and SAFE’s (Simple Agreement For Future Equity) – via crowdfunding platforms like nextseed and others like it. Marketing your business to investors on platforms like these taps into your existing skills in marketing and social media, and doesn’t require you develop capabilities in pitching your business that you might not have mastered.

As you advance along the growth curve, FinTech options expand and may offer you the best-priced capital on the market.

As a result of the expansion of FinTech based on alternative digital data sources, the potential for connecting your particular business to a well-matched and well-priced source of capital is greater and more precise than ever. Dusty cited a couple of examples like Kabbage (where, incidentally, entrepreneurs can currently get help with PPP loans). There are several more. Because of the competition in the FinTech market and the quality of the information they utilize, capital from these lenders is well-priced – probably approaching Mises’ originary rate of interest, Dusty observes, in a testimony to Austrian free market principles.

It is when your business represents the least risk to lenders that big banks offer their high-requirements business loans.

At a later stage of your business journey, banks will lend money against collateral and will impose additional onerous requirements and loan covenants. The entrepreneurial embrace of uncertainty is not for them! Bank financing is at the top when it comes to cost of capital and is to be approached cautiously. It is with bank financing that entrepreneurs become entangled with the negative effects of Federal Reserve repression of interest rates, that can mislead them into making incorrect investment decisions.

The cost of bank financing for mature companies revolves more around terms and covenants than interest rate percentage points. Banks are transactional, whereas entrepreneurs are operationally minded. This can cause a lot of friction if covenants, terms and triggers are not properly set. Entrepreneurs must pay attention to every detail in the loan contract. Great businesses can be ruined because of draconian covenants and triggers banks put into their loan contracts.

Indicated action: Entrepreneurs will be well-rewarded for fully investigating and understanding the emerging world of FinTech and digital SME finance. Be sure to calculate the full cost of capital – not just interest rates – and weigh all options.

Additional Resource

“Financial Capital Options For Businesses At All Stages” (PDF): Mises.org/E4E_63_PDF

You Might Also Like

In an Age of Pandemics We Need More Freedom to Trade, Not Less

In an Age of Pandemics We Need More Freedom to Trade, Not Less

There are many who use the coronavirus crisis to blame freedom to trade for the current epidemic. And, of course, there are those who are already arguing for autarky, closing our borders, and producing everything locally.

How to Think About the Fed Now

How to Think About the Fed Now

[This text is excerpted from the introduction to The Anatomy of the Crash, a Mises Institute ebook to be released in April 2020.] The Great Crash of 2020 was not caused by a virus. It was precipitated by the virus, and made worse by the crazed decisions of governments around the world to shut down business and travel. But it was caused by economic fragility.

How Government Makes a Pandemic More Deadly

How Government Makes a Pandemic More Deadly

In the early days of the outbreak, pundits rushed to the ramparts of Twitter to proclaim that “there are no libertarians in a pandemic.” However, this glee at the apparent failure of markets was soon dashed as more evidence accumulated showing that government intervention was actually the main impediment to success.

Your Supermarket Overlords: Why Barbados Needs a Voluntary Quarantine

Your Supermarket Overlords: Why Barbados Needs a Voluntary Quarantine

On Wednesday, April 1, the acting prime minister of Barbados, Hon. Santia Bradshaw, came on the local news station to announce a mandatory partial shutdown to combat COVID-19. She announced that starting April 3, all “nonessential” businesses would remain closed until midnight April 14.

Why Markets Are Rallying as Millions Become Unemployed

Why Markets Are Rallying as Millions Become Unemployed

The US economy is imprisoned, most of the population is under house arrest, and the inmates in Washington are running the asylum. And yet while the nation appears to be walking the green mile, investors residing in the Wall Street cell block have been extended pardons from the market gods.

Business Owners Understand Why the Economy Can’t Just Be “Reopened”

Business Owners Understand Why the Economy Can’t Just Be “Reopened”

My oldest turned seventeen last month. To commemorate the occasion, she and I watched Once Upon a Time in Hollywood. I’d taken her to her first (allegedly) rated-R movie a couple years ago to see the quite good Baby Driver, but this was Tarantino.

Why Markets Are Rallying as Millions Become Unemployed

Why Markets Are Rallying as Millions Become Unemployed

Wouldn’t you feel great knowing that your stock picking is fully insured by the Fed? Billionaires and wealthy hedge fund managers know the feeling.

Central Banks and the Next Crisis: From Deflation to Stagflation

Central Banks and the Next Crisis: From Deflation to Stagflation

All over the world, governments and central banks are addressing the pandemic crisis with three main sets of measures: Massive liquidity injections and rate cuts to support markets and credit.Unprecedented fiscal programs aimed at providing loans and grants for the real economy.Large public spending programs, fundamentally in current spending and relief measures.

Tags: Featured,newsletter