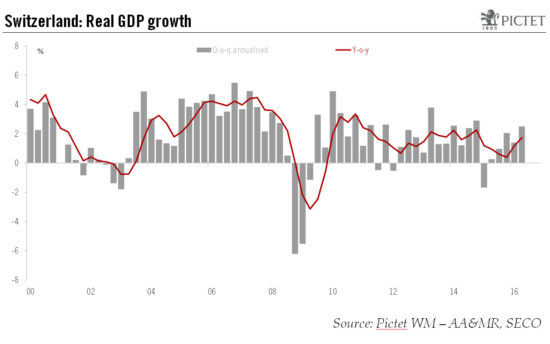

Macroview Stronger-than-forecast growth means the central bank is unlikely to alter monetary policy this month Swiss real GDP growth data surprised on the upside in Q2, expanding by 0.6% q-o-q (and 2.5% q-o-q annualised). In addition, growth in the three previous quarters was revised significantly higher. As a result, our GDP growth forecast for growth in Switzerland rises mechanically from 0.9% to 1.5% for 2016.GDP breakdown by expenditure component was less upbeat than the headline number and underlying growth dynamics remain broadly weak. (For example, household spending stagnated during the second quarter, fixed investment fell and export performance was patchy).Nevertheless, even accounting for some weakening in growth in Switzerland in the second half, the carryover effect from the latest GDP numbers means that Swiss growth should average 1.3% this year, even if the economy is flat for the rest of the year.We expect activity in Switzerland to weaken slightly in the second half of 2016, but the latest GDP figures mechanically push our GDP growth forecast up from 0.9% to 1.5% for 2016.The better-than-expected GDP growth figures are unlikely to alter current Swiss National Bank (SNB) monetary policy. At its next policy meeting, scheduled for September 15, the SNB is likely to maintain its interest rate on sight deposits at -0.

Topics:

Nadia Gharbi considers the following as important: Macroview, SNB monetary policy, Swiss economy, Swiss National Bank, Switzerland

This could be interesting, too:

Fintechnews Switzerland writes Top 12 Fintech Courses and Certifications in Switzerland in 2025

Claudio Grass writes “Does The West Have Any Hope? What Can We All Do?”

Dirk Niepelt writes “Pricing Liquidity Support: A PLB for Switzerland” (with Cyril Monnet and Remo Taudien), UniBe DP, 2025

Dirk Niepelt writes “Report by the Parliamentary Investigation Committee on the Conduct of the Authorities in the Context of the Emergency Takeover of Credit Suisse”

Stronger-than-forecast growth means the central bank is unlikely to alter monetary policy this month

Swiss real GDP growth data surprised on the upside in Q2, expanding by 0.6% q-o-q (and 2.5% q-o-q annualised). In addition, growth in the three previous quarters was revised significantly higher. As a result, our GDP growth forecast for growth in Switzerland rises mechanically from 0.9% to 1.5% for 2016.

GDP breakdown by expenditure component was less upbeat than the headline number and underlying growth dynamics remain broadly weak. (For example, household spending stagnated during the second quarter, fixed investment fell and export performance was patchy).

Nevertheless, even accounting for some weakening in growth in Switzerland in the second half, the carryover effect from the latest GDP numbers means that Swiss growth should average 1.3% this year, even if the economy is flat for the rest of the year.

We expect activity in Switzerland to weaken slightly in the second half of 2016, but the latest GDP figures mechanically push our GDP growth forecast up from 0.9% to 1.5% for 2016.

The better-than-expected GDP growth figures are unlikely to alter current Swiss National Bank (SNB) monetary policy. At its next policy meeting, scheduled for September 15, the SNB is likely to maintain its interest rate on sight deposits at -0.75% and to reiterate its willingness to intervene on the foreign exchange market to deal with short-term appreciation of the Swiss franc.