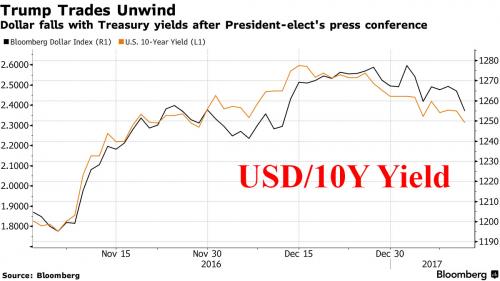

Risk assets declined across the globe, with European, Asian shares and S&P 500 futures all falling, while the dollar slumped against most currencies after a news conference by President-elect Donald Trump disappointed investors with limited details of his economic-stimulus plans, and the Trumpflation/reflation trade was said to be unwinding. "The risk was always that a president like Trump would end up upsetting that consensus (of faster U.S. growth, stronger dollar) view by introducing more political uncertainty," said asset manager GAM's head of multi-asset portfolios Larry Hatheway. The biggest mover, and perhaps the key driver of risk since the election, was the dollar which tumbled as much as 0.8%, falling below its 50DMA for the first time since the election, and back to where it was during the December 14 Fed rate hike announcement, while Treasuries gained alongside commodities, as Donald Trump’s press conference sent a wake-up call to the market about exalted expectations for fiscal stimulus in the U.S. "Overall, investors are wary ahead of Trump's inauguration – a case of buy the talk (Trumpflation), but sell the news," analysts at Societe Generale said in a note. However while negative for the US, that Trump did not mention possible tariffs against Chinese exports, was a relief for Asian share markets that have feared the outbreak of a global trade war.

Topics:

Tyler Durden considers the following as important: American people of German descent, ASX, ASX 200, B+, Bloomberg Dollar Spot, Bond, Borrowing Costs, Business, CAD, Central Intelligence Agency, China, Climate change skepticism and denial, Consumer Credit, Copenhagen, Copper, CPI, Crude, default, Default Rate, Donald Trump, Donald Trump presidential campaign, Dow 30, Dubai, Economic policy of Donald Trump, Equity Markets, European Central Bank, European Union, Exxon, Fibonacci, fixed, France, Freddie Mac, FTSE 100, Hang Seng 40, Hong Kong, Initial Jobless Claims, Italian Constitutional Court, Italy, Jim Reid, M2, Mike Pence, Money Supply, NASDAQ, Nasdaq Biotech, natural gas, Nikkei, Nikkei 225, Nomination, Obamacare, People's Bank Of China, Political positions of Donald Trump, Politics of the United States, Price Action, Reality, Renzi’s government, Rex Tillerson, S&P 500, S&P GSCI, S&P/ASX 200, South China, SPY, Stoxx 600, The Apprentice, trade deficit, Trade War, U.S. intelligence, U.S. Senate, United States Senate, US dollar, US Dollar Index, US Federal Reserve, World Trade Organization, Yen, Yuan, Zurich

This could be interesting, too:

Lance Roberts writes CAPE-5: A Different Measure Of Valuation

Lance Roberts writes CAPE-5: A Different Measure Of Valuation

Lance Roberts writes Estimates By Analysts Have Gone Parabolic

Lance Roberts writes The Impact Of Tariffs Is Not As Bearish As Predicted

Risk assets declined across the globe, with European, Asian shares and S&P 500 futures all falling, while the dollar slumped against most currencies after a news conference by President-elect Donald Trump disappointed investors with limited details of his economic-stimulus plans, and the Trumpflation/reflation trade was said to be unwinding.

"The risk was always that a president like Trump would end up upsetting that consensus (of faster U.S. growth, stronger dollar) view by introducing more political uncertainty," said asset manager GAM's head of multi-asset portfolios Larry Hatheway.

The biggest mover, and perhaps the key driver of risk since the election, was the dollar which tumbled as much as 0.8%, falling below its 50DMA for the first time since the election, and back to where it was during the December 14 Fed rate hike announcement, while Treasuries gained alongside commodities, as Donald Trump’s press conference sent a wake-up call to the market about exalted expectations for fiscal stimulus in the U.S.

"Overall, investors are wary ahead of Trump's inauguration – a case of buy the talk (Trumpflation), but sell the news," analysts at Societe Generale said in a note.

However while negative for the US, that Trump did not mention possible tariffs against Chinese exports, was a relief for Asian share markets that have feared the outbreak of a global trade war.

The lack of detail about a potential stimulus also put safety plays such as bonds and gold back in favor, cooling bets that have built in recent months on significantly higher global inflation and series of U.S. interest rate hikes. It was enough to send the dollar tumbling back below 114 yen for the first time in five weeks and brought some welcome relief to Brexit-bruised sterling and Turkey's lira, which has been badly beaten up this year. The USD/JPY broke below the prior session low of 114.25 to reach its weakest level in a month as broad assets position adjustments after recent rally continues to lower the pair’s range, said Satoshi Okagawa, senior global market analyst at Sumitomo Mitsui Banking Corp. in Singapore. Eventually the pair slid as low as 113.77 shortly after the European open before rebounding to just above 114.

The euro was back at $1.0650 for the first time in a month, shaky sterling climbed above $1.22 and Sweden's crown hit a four-month high and cracked its 200-day moving average against the euro after pacy inflation data. It was also bliss for bond markets that have been in reverse since Trump's election fuel led bets on higher U.S. interest rates that tend to set the bar for global borrowing costs.

Gold spiked on the weak dollar, rising above $1,200 since November 23, and at the 38.2% Fibonacci of the Trump-Led slide.

With all eyes on the dollar, the U.S. currency slumped against most major and the 10-year Treasury yield touched the lowest since November as Trump’s first press conference since his election victory gave no details on policy.

European stocks headed for their lowest close since the end of 2016 and drugmakers across the globe sold off. Turkey’s currency climbed for the first time in six days as the nation’s central bank tightened lira liquidity. Gold advanced to a seven-week high and industrial metals rallied. The Stoxx Europe 600 Index lost 0.5 percent and the FTSE 100 fell 0.2 percent, halting a record streak of gains. Health-care shares headed for their biggest drop since November, deepening losses that began late yesterday.

As Bloomberg, and virtually everyone else has pointed out many times already, Trump’s press conference left investors with few specifics on the timing and scope of planned policies from infrastructure spending to trade pacts. Since his victory, the dollar and global equities have rallied, while bonds sold off, on bets inflation would pick up with growth. Health-care stocks were pressured Thursday as Trump said he’d force the pharmaceutical industry to bid for government business in the world’s largest drug market.

“Markets are disappointed by a lack of detail around the much touted stimulus plans,” said Michael McCarthy, Sydney-based chief market strategist at CMC Markets Plc. “There is a growing fear that recent positive moves are based on bombast, and could unravel very quickly.”

"The news conference was a far cry from the market friendly, pro-growth "presidential" comments that Trump delivered at his acceptance speech," wrote analysts at Westpac, adding it left a "veritable laundry list" of questions unanswered.

Futures on the S&P 500 Index fell 0.3 percent. The underlying gauge increased 0.3 percent on Wednesday, staging an afternoon rally and recouping losses of as much as 0.4 percent.

In rates, the benchmark 10-year Treasury yield fell five basis points to 2.32 percent, touching the lowest level since Nov. 30. German 10-year yields dropped three basis points to 0.29 percent, while those in the U.K. slid five basis points to 1.29 percent.

Bulletin Headline Summary from RanSquawk

- European equities trade in the red, albeit modestly so as Europe continues to digest the fallout from Trump's press conference

- Some sweeping moves in the USD this morning, and all spurred by the lack of substance in yesterday's press conference by president elect Trump

- Looking ahead, highlights include ECB meeting minutes, US import and export prices, Fed's Yellen, Bullard and Kaplan

Market Snapshot

- S&P 500 futures down 0.3% to 2264

- Stoxx 600 down 0.2% to 364

- FTSE 100 down 0.2% to 7273

- DAX down 0.5% to 11582

- German 10Yr yield down 1bp to 0.32%

- Italian 10Yr yield up 1bp to 1.88%

- Spanish 10Yr yield up less than 1bp to 1.42%

- S&P GSCI Index up 0.8% to 398

- Nikkei 225 down 1.2% to 19135

- Hang Seng down 0.5% to 22829

- Shanghai Composite down 0.6% to 3119

- S&P/ASX 200 down less than 0.1% to 5767

- US 10-yr yield down 5bps to 2.32%

- Dollar Index down 0.62% to 101.15

- WTI Crude futures up 0.6% to $52.55

- Brent Futures up 0.9% to $55.58

- Gold spot up 1% to $1,204

- Silver spot up 1.2% to $16.93

Top News

- Obamacare Repeal Effort Clears First Big Hurdle in U.S. Senate: the U.S. Senate took the first step toward repealing Obamacare in a razor-thin vote early Thursday

- U.S. Said to Prepare WTO Complaint Against China on Aluminum: case focusing on loans said to be unveiled as soon as Thursday; global glut of aluminum threatening remaining U.S. capacity

- Alphabet Says It Shut Down Titan Drone Internet Project: similar project pursued by Facebook has also faced setback

- Blackstone Said to Vie With Warburg, Chinese Group for GLP: Blackstone considering offer for GLP, potentially pitting it against Warburg Pincus and a separate Chinese group

- J&J, Actelion Said to Reach Tentative Agreement on Price: discussions now said to focus on valuing separated R&D unit; companies could reach a final deal as soon as this month

- VW Officials Destroyed Files, E-Mails as Diesel Scheme Unraveled: co. pleads guilty, 5 more charged in emissions cheat

- Tillerson Says China Can’t Have Access to South China Sea Isles: U.S. Secretary of State nominee says China must be denied access to artificial islands built in disputed water

- U.S. Intelligence Chief Tells Trump He’s Dismayed by Leaks: Clapper said leak likely didn’t originate from spy agencies

- HSBC to Pay $45 Million to Settle Euribor Price-Fixing Case

- Floor & Decor Said to Revive IPO With >$1b Valuation: Reuters

- Jawbone Said to Be Looking for Funds After Fitbit Approach: FT

- CVC Capital Said in Advanced Talks to Buy MSC Software: Reuters

- Apax Partners Sells 48% Stake in GlobalLogic For $1.5b: ET

Looking at regional markets, we start in Asia where stock markets traded lower across the board to shrug off the positive lead from Wall Street as Trump's press conference led USD lower and as the surge in oil markets lifted the energy names. Nikkei 225 (-1.2%) underperformed on a firmer JPY as USD/JPY broke below 115.00, while comments in the US session from Trump criticising the healthcare sector led the pharmaceutical sector lower by around 3%. ASX 200 (-0.1%) pared early gains despite higher commodity prices, as a second day of double digit loss for Bellamy's and near 2% declined in the health care sector weighed the index. In China, Shanghai Comp (-0.6%) and Hang Seng (-0.4%) were lower amid a lack of news-flow and yet another reserved liquidity operation by the PBoC. 10yr JGBs traded marginally higher amid the risk averse tone in the region, while the curve flattened amid outperformance in the long end.

Top Asian NEws

- China Credit Growth Exceeds Estimates as Lending Remains Robust: aggregate financing was 1.63 trillion yuan in December; Broad M2 money supply increased by 11.3% percent, PBOC says

- Macau Casinos Lead Declines in Hong Kong Amid Revenue Concerns: Casino stocks dragged Hong Kong’s benchmark equity index lower by the most in three weeks

- Pimco Says China’s Next Big Shock May Be a Yuan Free Float: It would lead to a knee-jerk tumble, exacerbating capital outflows and sending shockwaves through global markets

All of the major European bourses trade in the red this morning with many analysts stating that President elect Trumps failure to mention any fiscal spending plans could be the main reason for the subdued sentiment. In company specific news, Tesco (-2.3%) shares are trading soft after broad sector strength earlier in the week. Elsewhere, Healthcare shares have been hit this morning after Trump stated that healthcare companies should be allowed to get away with charging extortionate prices. Luxury names have been trading well with Burberry (+1.3%) trading higher in sympathy with Richemont (7.6%) who reported a strong set of earnings pre-market. In Fixed income markets, Bunds opened higher in tandem with their US counterparts performance overnight, although prices have pulled away from best levels as markets take the opportunity to book profits. Elsewhere, supply from Europe has come in the form of Italian BTPs and a UK 2025 Gilt auction with UK paper relatively unfazed by a firm b/c of 2.52 and small yield tail.

Top European News

- German Economic Growth Accelerated in 2016 on Domestic Spending: German economic growth accelerated more than analysts forecast in 2016 to its fastest pace in 5 years

- Richemont Reports Unexpected Sales Gain as Watches Improve: 3Q sales +5% after falling 12% in 1H; better own-store watch sales good sign for wholesale: analysts

- Swatch Gains; Positive Read-Across from Richemont, Short Squeeze

- European Broadcasters Hook Up in Web Push as Viewers Move Online: Mediaset, TF1 invest in ProSiebenSat.1’s Studio71 unit

- UBI Climbs After Offering 1 Euro to Buy 3 Rescued Small Banks; UBI plans to raise as much as EU400m through a rights offer to purchase three “good banks” at a symbolic price

- Tesco Falls as Sales Growth Fails to Satisfy Investors; investor hopes had been raised by Wm Morrison Supermarkets’ results earlier in week

In currencies, there have been some sweeping moves in the USD this morning, and all spurred by the lack of substance in yesterday's press conference by president elect Trump. This is all the talk at the moment, so there is everything to suggest that this may continue to a modest degree, with USD dip buyers likely to limit and significant moves from current pullback levels. USD/JPY has taken out 114.00, but still looks vulnerable to a deeper correction which sees the potential for 113.00 base on the charts. Support from here stretches down to 111.45-50 before we can start talking of a reversal. This is very much the case in EUR/USD, where sellers have come in around 1.0650-60, but the risk for a move to 1.0700-1.0800 remains as rising EU inflation raises the prospect on greater consideration of (ECB) tapering. GBP has also benefitted from the turn in the USD as we have seen 1.2300 tipped in Cable this morning. Brexit related fears will keep a lid on any major recoveries — especially against the USD — as yield differentials also dictate. EUR/GBP price action will also reflect a clearer picture, but sentiment USD based for now. USD/CAD is now threatening a move on 1.3000 on the downside, with Oil prices having held up well over the last 24 hours. The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, fell 0.8 percent at 10:01 a.m. London time. It’s flat since the Fed’s rate decision on Dec. 14.

In commodities, the big mover in the commodity complex is Gold, taking out USD 1,200 as the USD was hit hard during president elect Trump's ineffective press conference yesterday. Resistance levels here into the mid USD1200's worth noting as USD dip buyers likely. Oil prices have performed well in the last 24 hours, and indeed over last night's key events. WTI above USD50.00 looks comfortable for now. Base metals mixed, but stable despite the lack of focus on infrastructure spending in the US. Anticipated China demand supports Copper which added 2.2% to $5,842 a metric ton, the highest in a month after Indonesia confirmed a halt to concentrate exports. Zinc rose 2.1 percent and nickel gained 1.5 percent. U.S. natural gas rose 3% to $3.32 per million British thermal units as a Bloomberg survey showed inventories probably fell by 141 billion cubic feet last week. U.K. natural gas rose 1.3 percent to 56.70 pence a therm, a fourth day of gains amid forecasts for cold weather.

Looking at today’s calendar, in the US the data docket contains the import price index reading for last month, last week’s initial jobless claims and the December monthly budget statement. Away from the data we’ll get the latest ECB minutes from last month’s policy meeting as well as a number of Fed speakers including Harker, Evans and Lockhart at 8.30am GMT, Bullard at 1.15pm and Kaplan at 1.45pm.

* * *

US Event Calendar

- 8:30am: Import Price Index MoM, Dec., est. 0.7% (prior -0.3%)

- 8:30am: Initial Jobless Claims, Jan. 7, est. 255k (prior 235k)

- 8:30am: Fed’s Harker Speaks in Malvern, Pennsylvania

- 8:30am: Fed’s Evans and Lockhart Take Part in Panel in Naples, Florida

- 9:45am: Bloomberg Consumer Comfort, Jan. 8 (prior 45.5)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 12pm: Monthly World Agriculture Supply and Demand Estimates

- 1:15pm: Fed’s Bullard Speaks in New York on U.S. Outlook

- 1:45pm: Fed’s Kaplan Speaks at Dallas Regional Chamber Event

- 2pm: Monthly Budget Statement, Dec., est. -$26.0b (prior - $136.7b)

Government Calendar

- 9:30am: Senate Armed Services Cmte hearing on nomination of retired Gen. James Mattis for defense secretary

- 10am: Senate Banking, Housing and Urban Affairs Cmte hearing on nomination of Ben Carson for HUD secretary

- 10am: Senate Foreign Relations Cmte second hearing on nomination of former Exxon Mobil CEO Rex Tillerson for sec. of state

- 10am: Senate Intelligence Cmte hearing nomination of Mike Pompeo for CIA director

- 2pm: House Armed Services Cmte holds mark up of waiver measure

DB's Jim Reid concludes the overnight wrap

Morning from Zurich. I listened to President-elect Trump's press conference on Bloomberg radio yesterday while on the tarmac waiting to take off from Oslo to Copenhagen. I must admit that whilst there was nothing much of substance for financial markets to take from it there's no doubting it was compelling stuff and it was one of the rare times I really didn't want a flight to take off and lose signal. I've never known anything like it from an incoming or sitting leader anywhere in the world. For a start you don't often have cheering and clapping at a press conference which came from a contingent of Mr Trump's supporters at the event. We also had a fierce exchange between the future President and a CNN reporter who was refused a question due to his organisation's reporting of Trump's alleged relationship with Russia.

We also learnt that Mr Trump turned down $2 billion last week from a Dubai developer and also a discussion over his trip to Russia to work on Miss Universe. Not the everyday stuff of governmental press conferences but when you see some of the bland stage managed versions around the world who is to say it's the wrong approach.

There was also a very brief mention of a “major border tax on companies leaving the US” and that Obamacare will be repealed and replaced “almost simultaneously” but overall markets were disappointed at the lack of substance around policy in particular. This was most apparent in FX where the US Dollar index finished the day -0.23% (and is down another -0.22% this morning) but was actually down as much as -1.62% from the intraday high at one stage. Over in rates 10y Treasury yields were down close to 5bps at one point, touching an intraday low in yield of 2.327%, before paring that move late into the close to finish more or less unchanged around 2.373%. Meanwhile equity markets posted modest gains but in reality were propped up by the +2.81% rebound for WTI Oil – despite some bearish inventory data - which helped the energy sector to outperform. Indeed the S&P 500 closed +0.28% and the Dow +0.50% but healthcare names took a bit of hit with Trump critical of drug pricing and saying that the industry needs “more competitive drug bidding” and that its currently “getting away with murder”. The Nasdaq Biotech index tumbled -2.96% as a result and had its worst day since October 11th.

Elsewhere Gold (+0.31%) notched up yet another gain however base metals generally eased off following the recent strong run. The European session had been a bit of a sideshow prior to Trump but markets still generally closed a touch firmer with the Stoxx 600 finishing +0.23%. The FTSE 100 (+0.21%) also notched up another gain and in doing so marked the first time the index has ever closed higher for 12 days in a row. That also coincided with Sterling at one stage touching a new 3-month low of $1.2039, before bouncing back into the close. The latest leg lower came as Governor Carney spoke and warned that Brexit could “amplify” four other dangers to the UK economy including the current account deficit, further weakness in Sterling, mounting consumer credit and a weaker commercial property market. On a related note, Scotland’s Nicola Sturgeon was dealt a bit of a blow yesterday after senior Norwegian politicians argued that it would be impossible for Scotland to move to a ‘Norway-style’ model for staying in the single market while also remaining part of the UK.

This morning in Asia it’s been another mixed start for markets. Most notable has been the decline for Japanese equities with the Nikkei (-1.26%) and Topix (-1.22%) tumbling with the healthcare sector and particularly those names with revenue exposure in the US notably underperforming following Trump’s comments about the sector. The Yen has also rallied about 2% since Trump spoke, which is also weighing. Meanwhile the Hang Seng (-0.33%) is also weaker, while the Shanghai Comp (+0.20%) and Kospi (+0.12%) are posting modest gains. The ASX is little changed.

Moving on. Yesterday we published our first Euro HY strategy monthly of the year. Since we published our 2017 Credit Outlook in late November we have seen some fairly impressive moves for EUR HY credit spreads. At this time we have no intention of changing our FY spread forecasts but given the strength of these moves we assess the implications for potential returns in 2017. At the time of the outlook our spread and default rate forecasts indicated that, whilst low, both excess and total returns should still be positive for 2017. Unsurprisingly given the positive performance in December and at the start of January we are now at a starting point where returns are likely to be negative for the coming year. Around -0.4% in terms of excess returns and -1.3% in total returns. We continue to think the intra-year range could be large for spreads and think there will be a better entry point into EUR HY than current levels even if this is not immediate. Please email [email protected] if you haven't received it.

Also yesterday we published a Credit Bite "Moody's Default Rates Tracker" (https://goo.gl/gCc5pU) detailing the agencies' latest 12-month-trailing high-yield default rates and their forecasts for the next 12 months. The default rate was 2.08% in Europe, 5.65% in the US and 4.41% globally. The baseline forecast for the next 12 months is 2.1% for Europe, 3.8% for the US and 3% globally

In our 2017 Outlook, we forecast 2.5% for Europe (https://goo.gl/BkHYrJ) and our US colleagues predict 5% for the US having revised down their earlier 7.25% forecast (https://goo.gl/3tWmf4). This is broadly in line with Moody’s view of a continued benign default environment in Europe and peaking of US defaults in the course of the year, although our US colleagues remain more cautious. Before we wrap up, in terms of the economic data yesterday the only releases of note came from the UK. Both industrial production (+2.1% mom vs. +1.0% expected) and manufacturing production (+1.3% mom vs. +0.5% expected) surprised to the upside, while the November trade deficit was reported as widening a little bit more than expected (to £12.2bn vs. £11.1bn expected). Carney also acknowledged yesterday that “the recent data would be consistent with a further upgrade of the forecasts” of the Bank.

Meanwhile over in Italy the Italian Constitutional Court rejected a request by the largest Italian union to force a referendum to overturn the core of the labour reform introduced by Renzi’s government in 2015, including the rejecting of the easing of redundancy rules for new hires. The ruling should come as some relief to new PM Gentiloni.

Looking at today’s calendar the only notable data due out in Europe this morning is the final revision to the December CPI report in France, Euro area industrial production in November and Germany’s first estimate of calendar year 2016 GDP growth. Over in the US the data docket contains the import price index reading for last month, last week’s initial jobless claims and the December monthly budget statement. Away from the data we’ll get the latest ECB minutes from last month’s policy meeting as well as a number of Fed speakers including Harker, Evans and Lockhart at 1.30pm GMT, Bullard at 6.15pm GMT and Kaplan at 6.45pm GMT.