Swiss Economicblogs.org

Swiss Economicblogs.org

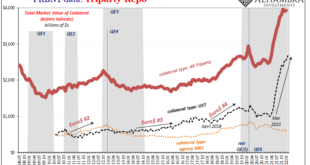

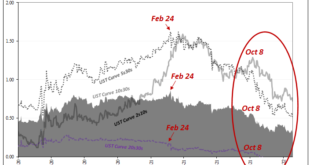

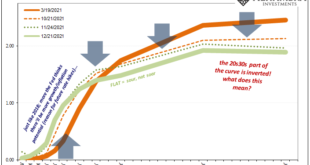

Securities lending as standard practice is incredibly complicated, and for many the process can be counterintuitive. With numerous different players contributing various pieces across a wide array of financial possibilities, not to mention the whole expanse of global geography, collateral for collateral swaps have gone largely unnoticed by even mainstream Economics and central banking. This despite the fact, yes, fact, securities lending was the epicenter of the 2008...

Read More »There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]