Swiss Economicblogs.org

Swiss Economicblogs.org

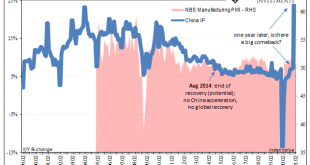

The Chinese were first to go down because they had been first to shut down, therefore one year further on they’ll be the first to skew all their economic results when being compared to it. These obvious base effects will, without further scrutiny, make analysis slightly more difficult. What we want to know is how the current data fits with the overall idea of recovery: is it on track, perhaps going better than thought, or falling short. Another set of huge positives...

Read More »Looking Past Gigantic Base Effects To China’s (Really) Struggling Economy