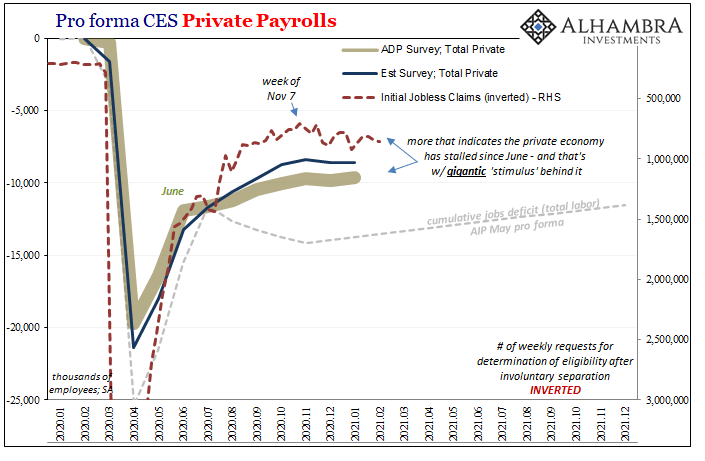

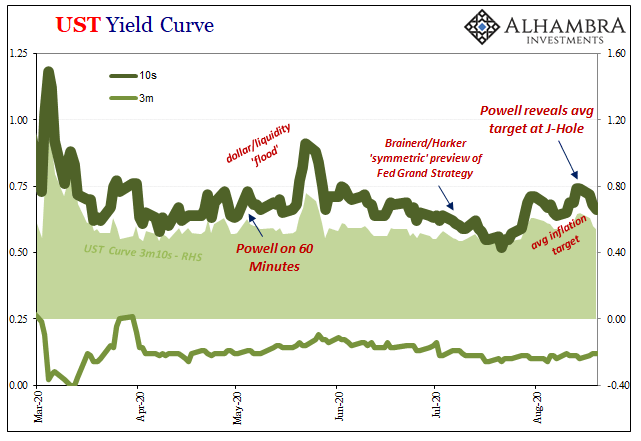

With the UST yield curve currently undergoing its own market-based twist, it’s worth investigating a couple potential reasons for it. On the one hand, the long end, clear cut reflation: markets are not, as is commonly told right now, pricing 1979 Great Inflation #2, rather how the next few years may not be as bad (deflationary) as once thought a few months ago. On the other hand, over at the short end, yields are dropping toward zero again. This steepening isn’t quite the “good” version. Supply issues are coming to T-bills, as we know, but anything else? Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge There’s been demand for these instruments which predates Janet Yellen resurfacing at the Treasury Department to unleash TGA drains and debt

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bonds, Collateral, currencies, Deflation, dollar roll, economy, Featured, Federal Reserve/Monetary Policy, inflation, Interest rates, Markets, mbs, newsletter, Reflation, Repo, steepening, T-Bills, tba market, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| With the UST yield curve currently undergoing its own market-based twist, it’s worth investigating a couple potential reasons for it. On the one hand, the long end, clear cut reflation: markets are not, as is commonly told right now, pricing 1979 Great Inflation #2, rather how the next few years may not be as bad (deflationary) as once thought a few months ago.

On the other hand, over at the short end, yields are dropping toward zero again. This steepening isn’t quite the “good” version. Supply issues are coming to T-bills, as we know, but anything else? |

Pro forma CES Private Payrolls, 2020-2021 - Click to enlarge |

| There’s been demand for these instruments which predates Janet Yellen resurfacing at the Treasury Department to unleash TGA drains and debt refunding.

I gave one longer-term explanation for heightened(ing) bill demand here (NPL’s and possible bank downgrades on an economy that stumbles rather than gets stimulated). I offered another technical possibility last Friday, one that would account for both sides of the yield twist:

|

UST Yield Curve, 2020-2021 - Click to enlarge |

| Given a choice, while these banks can use bank reserves to satisfy some surcharges, maybe they’d prefer selling off long end UST’s in favor of holding onto T-bills (or even buying more).

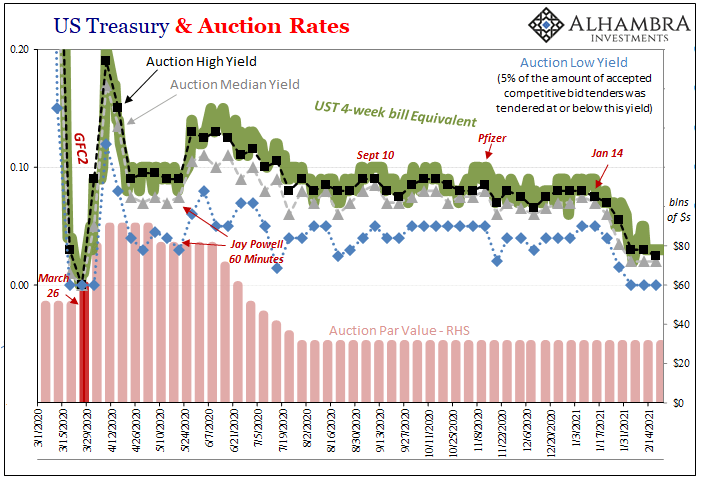

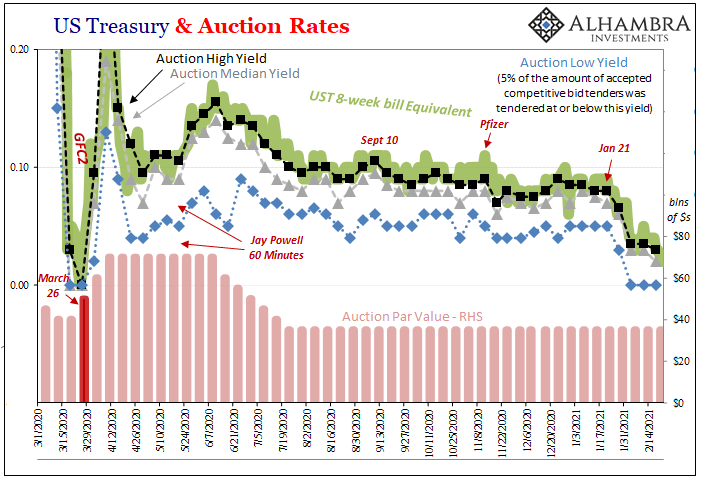

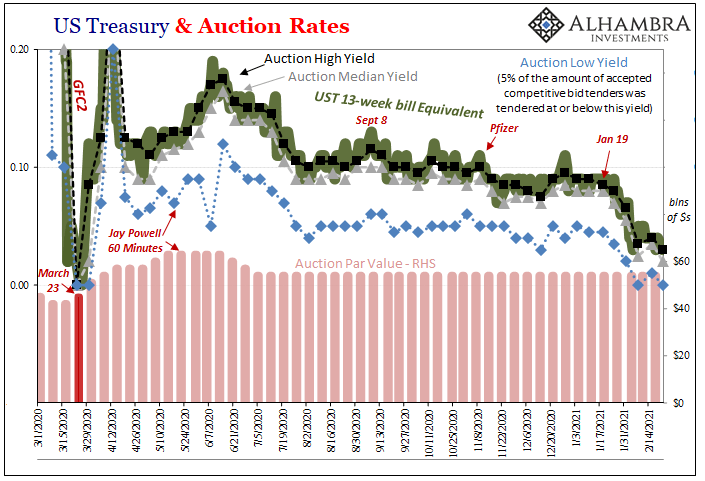

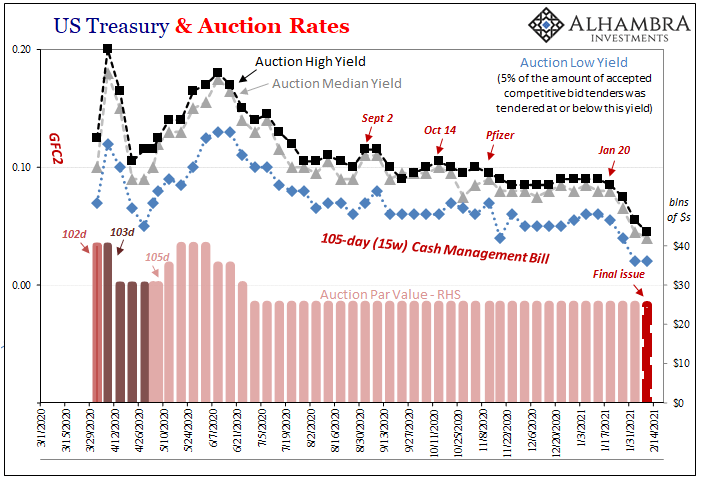

Looking into recent price/yield history, yeah, that’s in there: While November 10 represented Pfizer’s “stunning” vaccine announcement, it was also around that time jobless claims bottomed out therefore rising economic retrenchment risks; riskier in the short and intermediate terms with rising reflation potential if we can get beyond all that (which markets are becoming more complacent about the possibility). In early January, reflation was given another boost, allegedly, by the results of the Georgia Senate elections which cleared the path for more gigantic “stimulus.” Yet, bills weren’t performing that way at all; in fact, since around January 20 or even as early as January 14 (the latter for the 4-week bill; specific dates depend upon the specific maturity) that’s when bill rates really started to decline. |

US Treasury & Auction Rates, 2020-2021 - Click to enlarge |

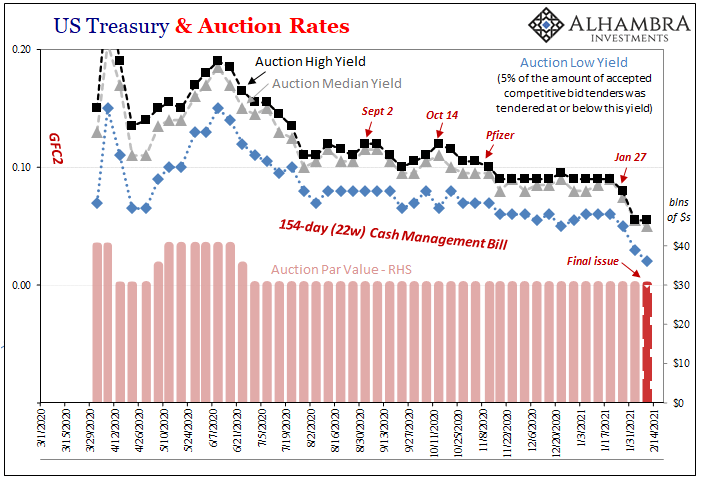

| That means for the past month we do find both how determined selling at the long end (reflation) really picked up pace and then an equal if not more determined buying frenzy registering up at the front – just as the SLR “cliff” scenario would figure. |

US Treasury & Auction Rates, 2020-2021 - Click to enlarge |

US Treasury & Auction Rates, 2020-2021 - Click to enlarge |

|

US Treasury & Auction Rates, 2020-2021 - Click to enlarge |

|

| There’s also another possibility from the bill end, however, which takes us back to 2013’s grossly misunderstood “taper tantrum.” Resetting the scene (which means going beyond the simple mainstream view of Bernanke’s “taper”, a word he never actually said, one that merely assumes monetary policy controls bonds the whole way down the curve), big repo problems as early as February (Fed buying OTR paper, and also doing some screwy things in mortgage TBA), and then in late June a real MBS blowout.

Here’s how I described it back in August 2014, a little over a year after the fact:

The rout around June 22 2013 was especially dramatic, with carnage being whispered as similar to that of certain days in 1994 (and other historic bond crashes). Not long after that, the major mortgage banks (which excludes Citi of the largest financial firms) began announcing rather large job cuts in their mortgage departments. |

US Treasury & Auction Rates, 2020-2021 - Click to enlarge |

| If you’re really interested in the nitty gritty granular details, you can read more about them in each of these cited articles: dollar rolls, TBA pipeline shortfalls, and therefore what sure seemed to have been a rather drastic, problematic MBS collateral shortage as a result.

The simple version (written in January 2014):

Some reasons why (written in May 2014, just as Euro$ #3 was breaking itself out in repo):

|

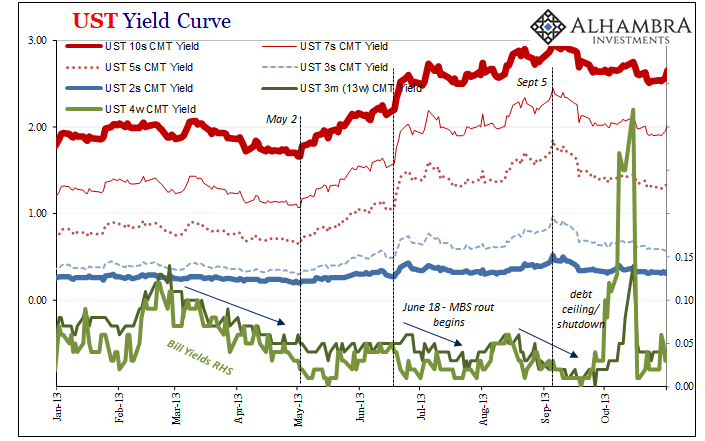

UST Yield Curve, 2013 - Click to enlarge |

| Dealers were, and remained, curiously absent from any or all securities lending channels which should have offered collateral-side support – if that had been during the pre-crisis era. That’s really the whole thing; dealer willingness and capacity.

Given their absence, this 2013 shortage of collateral would, you’d think, spillover from MBS and dollar rolls into other highly pristine forms like T-bills: There it is; bill yields falling from before the period in question (back several months to late February 2013) and then the same sort of “twisting” (falling front rates, rising back end yields) once the MBS market was hit with material liquidity problems even as the long UST “rout” continued selling reflation. These diverging trends continued until almost the end of 2013, with mainstream focus on only the one side. But then, right from the start of 2014, Euro$ #3 became more and more apparent (CNY and long end UST yields, spike in the overall dollar and commodity crash by mid-year), the entire global system increasingly synchronized with the 2013 view from bills (and repo collateral) rather than the sunny side of reflationary “tapering.” |

The Short End Money Equivalents, 2017 - Click to enlarge |

A similar situation, though produced from somewhat different conditions, rematerialized in the latter half of 2017 (Reflation #3, or “globally synchronized growth”), too, when long end rates backed up while bill yields, though up nominally, too, they were conspicuously “too low” in their own way (dropping and remaining below the RRP “floor”; see: above). What inevitably followed ended up being, like the prior Euro$ cycle, consistent with the bill story (Euro$ #4) and would prove the whole thing yet another reflationary disappointment.

Whether an SLR cliff or other possible reasons (including technical hardships as interest rates rise, which wouldn’t be hardships if recovery was the real deal), action at the front can and has – several times – suggested “dollar” shortage when quite a lot of everything else, including the long end, is declared to be steadfastly, unambiguously on the side of surefire reflation and even inflation to the moon.

It may seem any dollar shortage idea is hard to find right now, with everyone screaming about governments having done way, way too much money-wise. It’s actually not that hard to find; that’s really all these reflationary trends have been. The dollar shortage becomes acute and impossible not to notice (Euro$ #n), and then recedes into the background (Reflation #n) allowing for these periods of mistaken identification.

The system’s still exhibiting key symptoms (the same, sadly) of being broken down, just not nearly as uniformly and openly as it had been during last year. That’s not quite the same thing as inflationary overshoot, though, is it?

What might this ultimately mean, beyond the more obvious? That’s next.

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

Weekly SNB Sight Deposits and Speculative Positions: SNB buying euros at high prices

2021-02-22

Update February 22 2021: SNB intervening. Sight Deposits have risen by +0.1 bn CHF, this means that the SNB is intervening and buying Euros and Dollars: The change is +0.1 bn. compared to last week.

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

2021-02-19

It’s worth taking a look at a couple of extremes, and the putting each into wider context of inflation/deflation. As you no doubt surmise, only one is receiving much mainstream attention. The other continues to be overshadowed by…anything else.

They’ve Gone Too Far (or have they?)

They’ve Gone Too Far (or have they?)

2021-01-10

Between November 1998 and February 1999, Japan’s government bond (JGB) market was utterly decimated. You want to find an historical example of a real bond rout (no caps nor exclamations necessary), take a look at what happened during those three exhilarating (if you were a government official) months.

Just Who Is, And Who Is Not, Selling T-Bills

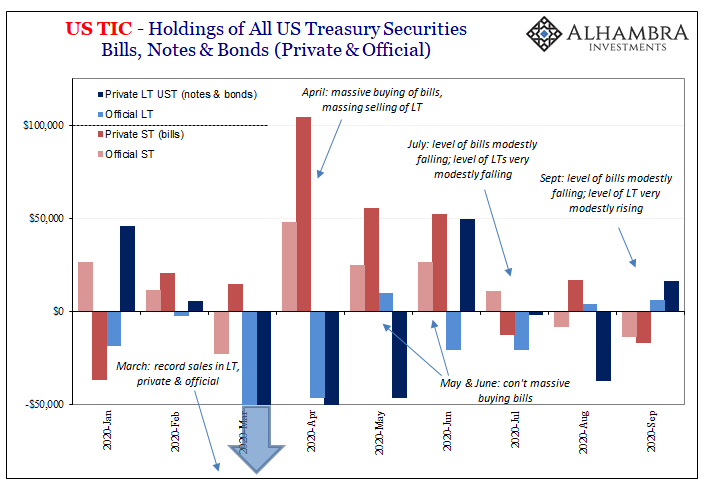

Just Who Is, And Who Is Not, Selling T-Bills

2020-11-29

Are foreigners selling Treasury bills? If they are, this would seem to merit consideration for the reflation argument. After all, the paramount monetary deficiency exposed by March’s GFC2 (and the Fed’s blatant role in making it worse) was the dangerous degree of shortage over the best collateral.

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

Why Aren’t Bond Yields Flyin’ Upward? Bidin’ Bond Time Trumps Jay

2020-10-02

It’s always something. There’s forever some mystery factor standing in the way. On the topic of inflation, for years it was one “transitory” issue after another. The media, on behalf of the central bankers it holds up as a technocratic ideal, would report these at face value. The more obvious explanation, the argument with all the evidence, just couldn’t be true otherwise it’d collapse the technocracy right down to the ground.And so it was also in the bond market. Inflation and their yields very much related, the lack of the former wasn’t ever used to explain the curious absence of the BOND ROUT!!! No, the US Treasury market has been beset by its own set of “transitory” factors, too. As ridiculous as some of the inflation excuses had been, Verizon’s unlimited wireless data plans the

If Dollar Is Fixed By Jay’s Flood, Why So Many TIC-ked At Corporates in July?

If Dollar Is Fixed By Jay’s Flood, Why So Many TIC-ked At Corporates in July?

2020-09-21

When the eurodollar system worked, or at least appeared to, not only did the overflow of real effective (if virtual and confusing) currency “weaken” the US dollar’s exchange value, its enormous excess showed up as more and more foreign holdings of US$ assets.

Re-recession Not Required

Re-recession Not Required

2020-09-12

If we are going to see negative nominal Treasury rates, what would guide yields toward such a plunge? It seems like a recession is the ticket, the only way would have to be a major economic downturn. Since we’ve already experienced one in 2020, a big one no less, and are already on our way back up to recovery (some say), then have we seen the lows in rates?Not for nothing, every couple years when we do those (record low yields) that’s what “they” always say and yet they only ever go lower the next time. But what do we mean by “the next time?”Before getting into it, the central bank simply doesn’t factor. Monetary authorities possess no monetary abilities therefore they follow along with what bond markets are already doing. Sometimes that means lowering their benchmarks, like Jay Powell’s

Powell Would Ask For His Money Back, If The Fed Did Money

Powell Would Ask For His Money Back, If The Fed Did Money

2020-09-05

Since the unnecessary destruction brought about by GFC2 in March 2020, there have been two detectable, short run trendline upward moves in nominal Treasury yields. Both were predictably classified across the entire financial media as the guaranteed first steps toward the “inevitable” BOND ROUT!!!!

Tags: Bonds,collateral,currencies,Deflation,dollar roll,economy,Featured,Federal Reserve/Monetary Policy,inflation,Interest rates,Markets,mbs,newsletter,Reflation,repo,steepening,T-Bills,tba market,Yield Curve