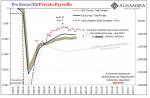

According to newly revised BLS benchmarks, the labor market might have been a little bit worse than previously thought during the worst of last year’s contraction. Coming out of it, the initial rebound, at least, seems to have been substantially better – either due to government checks or, more likely, American businesses in the initial reopening phase eager to get back up and running on a paying basis again. The JOLTS labor series annual revisions took about 300,000 off the estimated level of Job Openings (JO), one way to figure demand for labor, in each March and April 2020. Instead of a bottom just less than a 5 million pace, the government now thinks it was more like 4.63 million. JOLTS - Job Openings, SA 2017-2021 - Click to enlarge In terms of Hires

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, Deflation, economy, Featured, Federal Reserve/Monetary Policy, hires, hiring rate, hwol, inflation, Initial Jobless Claims, job openings, jobless claims, jolts, labor demand, Labor market, Markets, newsletter, online ads

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| According to newly revised BLS benchmarks, the labor market might have been a little bit worse than previously thought during the worst of last year’s contraction. Coming out of it, the initial rebound, at least, seems to have been substantially better – either due to government checks or, more likely, American businesses in the initial reopening phase eager to get back up and running on a paying basis again.

The JOLTS labor series annual revisions took about 300,000 off the estimated level of Job Openings (JO), one way to figure demand for labor, in each March and April 2020. Instead of a bottom just less than a 5 million pace, the government now thinks it was more like 4.63 million. |

JOLTS - Job Openings, SA 2017-2021 - Click to enlarge |

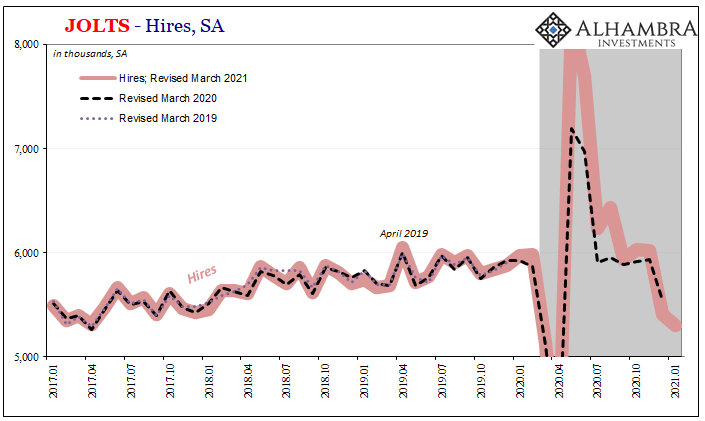

| In terms of Hires (HI), the revision was less, removing only 100k for April. |

JOLTS - Hires, SA 2017-2021 - Click to enlarge |

|

On the way back out the depths, though, now the BLS calculates HI in May had been simply astronomical; whereas previous they’d put the hiring rate during that month at an impressive 7.2 million, way above records as the flood of reopening worked out to more work, the agency now believes that rate had instead been nearly 8.3 million; an explosive 1.1 million upward revision. This overperformance on the company side remained for a few months toward the rest of the year in the new benchmarks, though becoming far, far less as 2020 wore on. While June’s HI rate was again a million better than previously figured, and in August still around 500,000 higher, by November the difference was less than 100,000 as the labor market cooled way too soon before it ever really got going. |

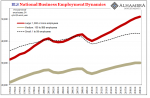

JOLTS - Job Openings, SA 2000-2020 - Click to enlarge |

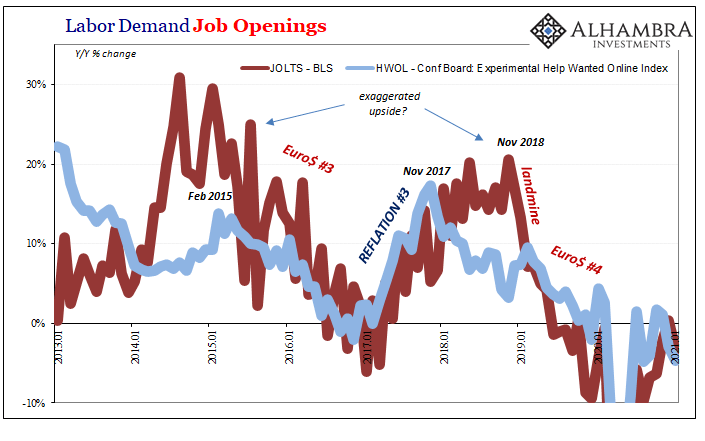

Labor Demand Job Openings, 2013-2021 - Click to enlarge |

|

| Job Openings, by contrast, were revised slightly upward toward the end of last year which only brings up the same discrepancies that have plagued these two JOLTS series for several years now. According to JO, companies seem to be posting a lot more online ads for positions they don’t appear intent to fill; or, most likely, they are that much more difficult to fill.

In 2021, the latest update (including benchmarks) for January, the level of JO while better than previously thought are still less than the same month last year (this is also true of the unrelated Conference Board Help Wanted Online index, or HWOL). |

JOLTS - Hires, SA 2000-2020 - Click to enlarge |

| But while indicated labor demand happened to be slightly less than pre-recession, the hiring rate in January was more than 11% below the year earlier period even with new benchmarks. Using them anyway, the hiring rate in December was actually revised downward by 100k and then for January the estimate dropped by another 100k. These figures are substantially weaker than even the not-so-good headline payroll numbers of the Establishment Survey for the same months (note: benchmark revisions for the CES were already released and, unlike JOLTS, did not indicate major changes).

In other words, the labor market’s rebound got off to a tremendous start (as we knew) but by the end of the year it had actually ended pretty badly. |

. |

| Why didn’t the better-than-believed momentum carry much further on?

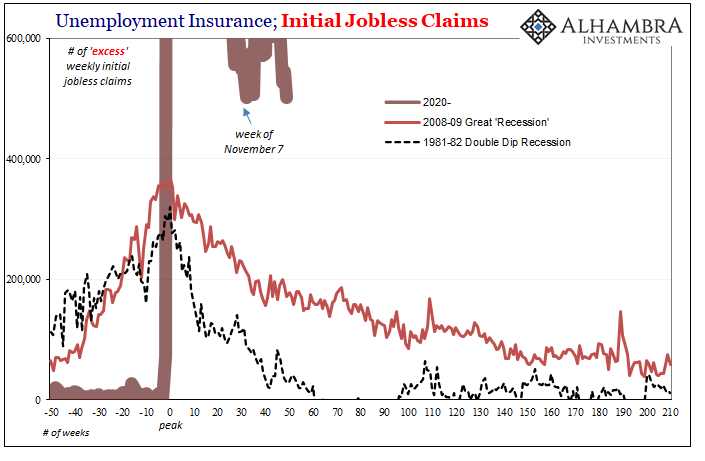

The fact that it didn’t has been simply overshadowed by hopes placed on vaccines and the promises of still more government helicopter drops (one completed late December/early January, no help to either help wanted ads or hiring intentions; the second to begin once the bill is signed tomorrow). Perhaps a touch more optimistically, initial jobless claims for the week of March 6 declined to 712,000. That’s the second lowest since the recession began, yet still the 51st consecutive week at more than 700,000 (no week previous to last March had ever been that high). |

Unemployment Insurance, Initial Jobless Claims, 1981-2020 - Click to enlarge |

| On the one hand, like the payroll data for February, there’s an inkling of more reopening but questions abound as to the vastly more consequential reawakening. Despite more “stimulus”, if it’s only reopening that contributes and underlying that remains dormant labor demand (meaning hires however many online ads need to be posted to secure them) there’s only going to be a limit on what Uncle Sam’s politically-motivated generosity can achieve.

Even the JO data backs up all the reasons why Americans have opted to save the vast majority of these helicopter payments; the labor market is coming back, for sure, but way, way too slowly to do anything other than hinder rather than amplify rebound or reflationary processes. Companies may be posting a bit more online ads advertising work, but is there actually that much work needing to be done? Is there really even that much demand for labor? As with February payrolls (hours in particular):

This isn’t to say that the US economy appears in looming danger of falling back into contraction like Europe; rather, there isn’t really any distinction. We’ve already got the recession and, contrary to original hype (now increasingly backed by May/June JOLTS data), there have to be reasons why it never went any further. Those may tell us something important about what comes next (inflation vs. more of the same, for example). COVID doesn’t answer for the summer slowdown and its stubbornness – exhibited by payroll estimates, JOLTS series, and jobless claims altogether. |

CES Index of Aggregate Weekly Hours, 2008-2021 - Click to enlarge |

You Might Also Like

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

Weekly SNB Sight Deposits and Speculative Positions: SNB selling euros and dollars

2021-03-15

Update March 15 2021: SNB selling euros and dollars. Sight Deposits have fallen: The change is -0.3 bn. compared to last week, this means the SNB is selling euros and dollars.

What Gold Says About UST Auctions

What Gold Says About UST Auctions

2021-03-11

The “too many” Treasury argument which ignited early in 2018 never made a whole lot of sense. It first showed up, believe it or not, in 2016. The idea in both cases was fiscal debt; Uncle Sam’s deficit monster displayed a voracious appetite never in danger of slowing down even though – Economists and central bankers claimed – it would’ve been wise to heed looming inflationary pressures to cut back first.

What Might Be In *Another* Market-based Yield Curve Twist?

What Might Be In *Another* Market-based Yield Curve Twist?

2021-02-23

With the UST yield curve currently undergoing its own market-based twist, it’s worth investigating a couple potential reasons for it. On the one hand, the long end, clear cut reflation: markets are not, as is commonly told right now, pricing 1979 Great Inflation #2, rather how the next few years may not be as bad (deflationary) as once thought a few months ago.

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

Two Seemingly Opposite Ends Of The Inflation Debate Come Together

2021-02-19

It’s worth taking a look at a couple of extremes, and the putting each into wider context of inflation/deflation. As you no doubt surmise, only one is receiving much mainstream attention. The other continues to be overshadowed by…anything else.

The Endangered Inflationary Species: Gazelles

The Endangered Inflationary Species: Gazelles

2021-02-11

Nevada is, by all accounts and accountants, in rough shape. Very rough shape. An economy overly dependent upon a single industry, tourism, in this case, is a disaster waiting to happen should anything happen to that industry. Pandemic restrictions, for instance.

Inflation Hysteria #2 (Slack-edotes)

Inflation Hysteria #2 (Slack-edotes)

2020-12-13

Macroeconomic slack is such an easy, intuitive concept that only Economists and central bankers (same thing) could possibly mess it up. But mess it up they have. Spending years talking about a labor shortage, and getting the financial media to report this as fact, those at the Federal Reserve, in particular, pointed to this as proof QE and ZIRP had fulfilled the monetary policy mandates – both of them.

Inflation Hysteria #2 (WTI)

Inflation Hysteria #2 (WTI)

2020-12-12

Sticking with our recent theme, a big part of what Inflation Hysteria #1 (2017-18) also had going for it was loosened restrictions for US oil producers. Seriously.

Don’t Really Need ‘Em, Few More Nails Anyway

Don’t Really Need ‘Em, Few More Nails Anyway

2020-12-06

The ISM’s Non-manufacturing PMI continued to decelerate from its high registered all the way back in July 2020. In that month, the headline index reached 58.1, the best since early 2019, and for many signaling that everything was coming up “V.”

Tags: currencies,Deflation,economy,Featured,Federal Reserve/Monetary Policy,hires,hiring rate,hwol,inflation,Initial Jobless Claims,job openings,jobless claims,jolts,labor demand,Labor Market,Markets,newsletter,online ads