Thomas Costerg and Dong Chen

March 27, 2018

Perspectives Pictet

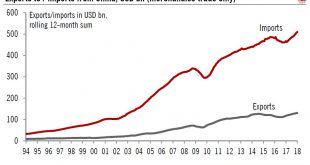

Trump’s trade tariffs should have a very small impact and may be a ploy to reach a trade agreement.The Trump Administration last week announced tariffs of 25% on USD 60bn worth of imports from China (out of USD 506bn of total Chinese merchandise imports). The list of products targeted still has to be thrashed out. The official aim is to sanction China for alleged theft of US firms’ intellectual property; the US Trade Representative (USTR) estimates the damage amounts to USD 50bn.But...

Read More »

Nadia Gharbi

March 27, 2018

SNB & CHF

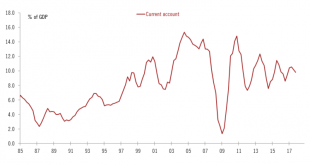

Following the Swiss National Bank’s (SNB) publication of Switzerland’s balance of payments data for Q4 2017, in this note we look deeper into the Swiss current account to try to find out why Switzerland persistently runs a surplus and whether or not the current account balance can be used to assess the fair value of the Swiss franc.

In 2017, the current account surplus stood at around 9.8% of GDP or CHF66bn. This was...

Read More »

Nadia Gharbi

March 27, 2018

Perspectives Pictet

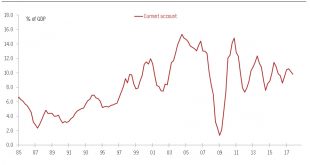

Switzerland’s high current account surplus is far from being a good proxy for assessing the fair value of the Swiss franc.Switzerland has run a current account surplus since the 1980s. In 2017, it stood at around 9.8% of GDP, CHF66bn. This was CHF4bn higher than in 2016.Economic theory suggests that a large current account surplus is a function of an undervalued currency. Based on this premise, there may be question marks over the SNB’s contention that the Swiss franc was “overvalued”.In a...

Read More »

Nadia Gharbi

March 27, 2018

Perspectives Pictet

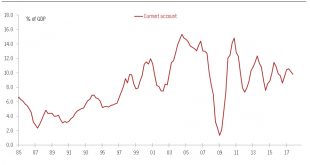

Switzerland’s high current account surplus is far from being a good proxy for assessing the fair value of the Swiss franc.Switzerland has run a current account surplus since the 1980s. In 2017, it stood at around 9.8% of GDP, CHF66bn. This was CHF4bn higher than in 2016.Economic theory suggests that a large current account surplus is a function of an undervalued currency. Based on this premise, there may be question marks over the SNB’s contention that the Swiss franc as “overvalued”.In a...

Read More »

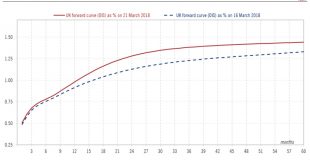

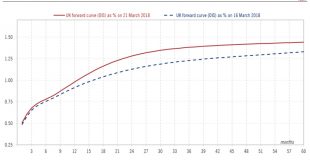

Luc Luyet

March 26, 2018

Perspectives Pictet

Recent positive developments in the United Kingdom may brush a supportive picture for sterling in the short term, but the long-term outlook remains cloudy at best.The transitional deal reached between the UK and the European Union (EU) on 20 March and the strong job market report on 21 March plead for a more positive short-term outlook for sterling than previously thought. We are therefore revising our projections upward for sterling over the next three, six and 12 months versus the USD....

Read More »

Luc Luyet

March 26, 2018

Perspectives Pictet

Recent positive developments in the United Kingdom may brush a supportive picture for sterling in the short term, but the long-term outlook remains cloudy at best.The transitional deal reached between the UK and the European Union (EU) on 20 March and the strong job market report on 21 March plead for a more positive short-term outlook for sterling than previously thought. We are therefore revising our projections upward for sterling over the next three, six and 12 months versus the USD....

Read More »

Frederik Ducrozet

March 24, 2018

SNB & CHF

Today’s first batch of euro area March business surveys looks worrying at first sight. The drop in the euro area composite PMI index, from 57.1 to 55.3 in March (consensus: 56.8), was the second one in a row and the largest monthly decline in six years. New orders fell to a 14-month low. The correction in business sentiment was predominantly driven by the manufacturing sector, which could reflect broader concerns of a...

Read More »

Frederik Ducrozet

March 23, 2018

SNB & CHF

Much of recent ECB dovish rhetoric has been building around the (not-sonew) idea that potential growth might be higher than previously thought, implying a larger output gap and lower inflationary pressure, all else equal. The argument is both market-friendly and politically welcome – what we are seeing is the early effects of those painful structural reforms implemented during the crisis. Inflation would be low for good...

Read More »

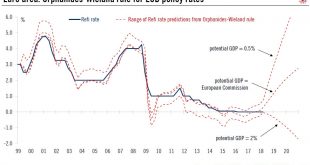

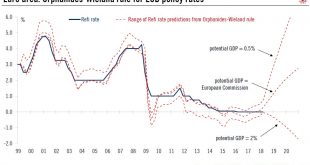

Frederik Ducrozet

March 23, 2018

Perspectives Pictet

ECB ‘higher potential’ rhetoric comes with some difficulties.Much of recent ECB dovish rhetoric has been building around the (not-so-new) idea that potential growth might be higher than previously thought, implying a larger output gap and lower inflationary pressure, all else equal. The argument is both market-friendly and politically welcome – what we are seeing is the early effects of those painful structural reforms implemented during the crisis. Inflation would be low for good reasons.We...

Read More »

Frederik Ducrozet

March 23, 2018

Perspectives Pictet

ECB ‘higher potential’ rhetoric comes with some difficulties.Much of recent ECB dovish rhetoric has been building around the (not-so-new) idea that potential growth might be higher than previously thought, implying a larger output gap and lower inflationary pressure, all else equal. The argument is both market-friendly and politically welcome – what we are seeing is the early effects of those painful structural reforms implemented during the crisis. Inflation would be low for good reasons.We...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org