It’s one of those things which everyone just accepts because everyone says it must be true. If the US$ is rising, what else other than the Federal Reserve. In particular, the Fed has to be raising rates in relation to other central banks; interest rate differentials. A relatively more “hawkish” US policy therefore the wind in the sails of a “strong” dollar exchange regime. How else would we explain, for example, the euro’s absolute plunge since around May last year? Everything since would seem to agree with the conventional theory; the Fed has turned ultra-hawkish whereas the ECB has time and again very publicly stated it will resist the same temptation to chase CPIs. As a result, expectations for much higher ST rates here versus there, therefore the euro’s

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, Alan Greenspan, bonds, Collateral, currencies, Dollar, ECB, economy, Euro, EuroDollar, Featured, Federal funds, Federal Reserve, Federal Reserve/Monetary Policy, Interest rates, Markets, newsletter, T-Bills

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It’s one of those things which everyone just accepts because everyone says it must be true. If the US$ is rising, what else other than the Federal Reserve. In particular, the Fed has to be raising rates in relation to other central banks; interest rate differentials. A relatively more “hawkish” US policy therefore the wind in the sails of a “strong” dollar exchange regime.

How else would we explain, for example, the euro’s absolute plunge since around May last year? Everything since would seem to agree with the conventional theory; the Fed has turned ultra-hawkish whereas the ECB has time and again very publicly stated it will resist the same temptation to chase CPIs. As a result, expectations for much higher ST rates here versus there, therefore the euro’s plunge. But why didn’t the same happen the last time both central banks went through this very same exercise? |

. |

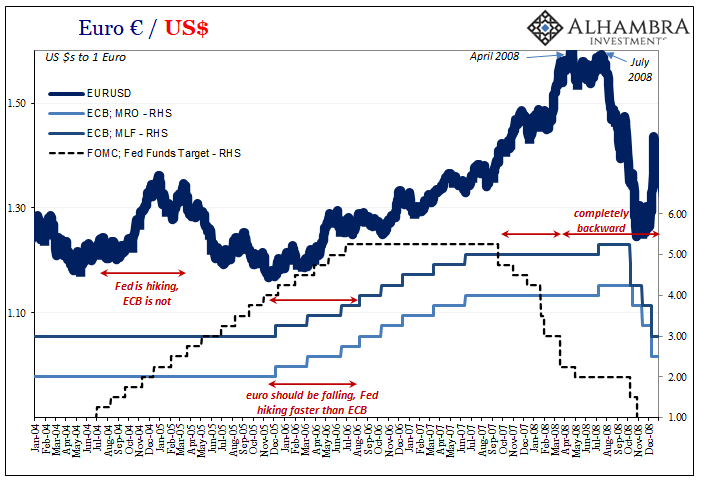

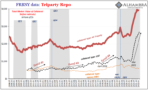

| Just like this time, Alan Greenspan’s Fed turned hawkish long before Trichet’s ECB would. The FOMC voted its initial rate hike in June 2004, while it would take Europe’s policymakers all the way until December 2005 to get started.

When all was said and done, Greenspan then Bernanke would raise fed funds well above the European policy corridor (the top half of it represented by the space between the MRO and MLF, where Eonia used to trade). Farther and faster, yet it was the euro not the dollar which rose in that period. You could make the case (I wouldn’t) that the ECB was catching up after the Fed’s final hike and that accounts for a “stronger” euro particularly middle of 2006 onward. Then once American officials began to cut rates in September 2007, the Europeans held steady and even, (in)famously, raised rates in July 2008. Euro went up. But that doesn’t really make sense, either. While the first part could, up to April 2008, thereafter interest rate differentials grew more and more in the euro’s favor yet the euro not the dollar started to go down. By July 2008, just a week or so after Trichet’s embarrassing rate hike, the euro would absolutely crash. |

. |

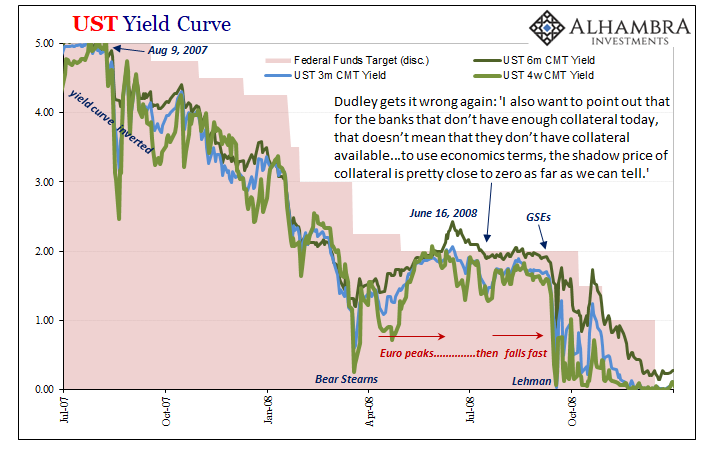

| That last part was very clear, at least, when the dollar was forced skyward by the arrival and eruption of Euro$ #1 going global; it had nothing whatsoever to do with interest rates on either side of the Atlantic or the currency equation.

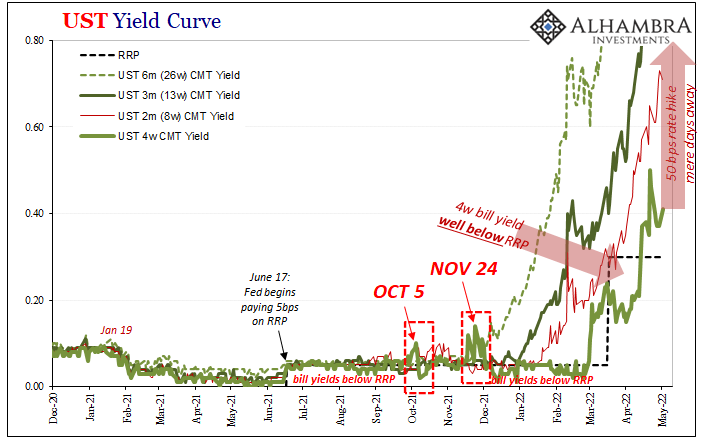

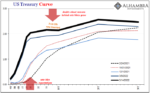

So, we have to ask again; why is the euro down so much 2021-22? Rather than care much about the Fed vs. ECB, maybe a better question to ask is this: why is the 4-week Treasury bill sitting there on May 2 yielding only 41 bps? While that’s finally above the current RRP, you’ll note that beginning tomorrow the FOMC will meet and by Wednesday almost certainly announce that is has raised the RRP by 50 bps. And even if policymakers do chicken out again, it will be a guaranteed twenty-five. In other words, the RRP by Thursday has to be 55 bps minimum, though far more likely 80 bps. Yet, the 4-week bill (and the 8-week) isn’t anywhere close to either of those when by every investment return consideration it should already be above the latter. Wouldn’t you know it, too, that from late May 2008 all the way into that second phase of Euro$ #1, T-bill rates began to drop has they had leading up to Bear Stearns. These did not go unnoticed by policymakers; they were, obviously, totally unappreciated though not in the financial system itself.

|

. |

| From July 2008 onward, the system – and the dollar’s value – went full-blown Euro$ #1 which included an increasingly desperate scramble for collateral. All that even before Lehman.

It’s true the Fed is hiking rates more aggressively than the ECB in 2022, but not all rates are rising all that fast. Maybe it is those we should pay more attention to rather than policies, and not just as it relates to the euro’s falling value. This doesn’t mean we are about to replay 2008, but it sure doesn’t indicate anything like the mainstream myth about the Fed, interest rate differentials, and what’s really goes on in the “dollar.” |

. |

You Might Also Like

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai

2022-04-25

What everyone is saying, because it’s convenient, is that China’s zero-COVID policies are going to harm the economy. No. Economic harm of the past is the reason for the zero-COVID policies. As I showed yesterday, the cracking down didn’t just show up around 2020, begun right out in the open years beforehand, born from the scattering ashes of globally synchronized growth.

Yield Curve Inversion Was/Is Absolutely All About Collateral

Yield Curve Inversion Was/Is Absolutely All About Collateral

2022-04-18

If there was a compelling collateral case for bending the Treasury yield curve toward inversion beginning last October, what follows is the update for the twist itself. As collateral scarcity became shortage then a pretty substantial run, that was the very moment yield curve flattening became inverted.Just like October, you can actually see it all unfold.

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)

2022-03-21

The Federal Reserve didn’t just raise the range for its federal funds target by 25 bps, upper and lower bounds, it also added the same to its twin policy tools which the “central bank” says are crucial to maintaining order in money markets thereby keeping federal funds inside the band where it is supposed to be. The FOMC voted to increase IOER from 15 bps to 40 bps, and the RRP from 5 bps to 30 bps.

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]

2022-03-18

Securities lending as standard practice is incredibly complicated, and for many the process can be counterintuitive. With numerous different players contributing various pieces across a wide array of financial possibilities, not to mention the whole expanse of global geography, collateral for collateral swaps have gone largely unnoticed by even mainstream Economics and central banking.

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 1]

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 1]

2022-03-17

With the 7s10s already inverted, and the 5s today mere bps away, making a macro case for the distortion isn’t too difficult. Despite China’s “upside” economic data today, even the Chinese are talking more about their downside worries (shooting/hoping for “stability”) than strength. In the US or Europe, no matter the CPIs in either place there are cyclical (not just inventory) warning signs all over the place.

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift

SWIFT Isn’t The ‘Nuclear Option’ For Russia, Because Russia can sell the dollars elsewhere and NOT via Swift

2022-03-01

As everyone “knows”, the US dollar is the world’s reserve currency which can only leave the US government in control of it. Participation is both required and at the pleasure of American authorities. If you don’t accept their terms, you risk the death penalty: exile from the privilege of the US dollar’s essential business.From what little most people know about that essential business, it seems like it has something to do with that thing called SWIFT. Thus, Russia. In fact, the White House’s statement from a few days ago confirms these things. At least, it seems to confirm what most people already believe:

First, we commit to ensuring that selected Russian banks are removed from the SWIFT messaging system. This will ensure that these banks are disconnected from the international

Sentiment v. Substance: Checking In On Collateral Via, Yes, The Fed

Sentiment v. Substance: Checking In On Collateral Via, Yes, The Fed

2022-01-13

The Federal Reserve, like other central banks around the world, it does lend out the securities it owns and holds. Sophisticated modern wholesale money markets are highly collateralized, so much so that collateral itself takes on the properties of currency.

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

Tags: Alan Greenspan,Bonds,collateral,currencies,dollar,ECB,economy,Euro,EuroDollar,Featured,federal funds,Federal Reserve/Monetary Policy,federal-reserve,Interest rates,Markets,newsletter,T-Bills