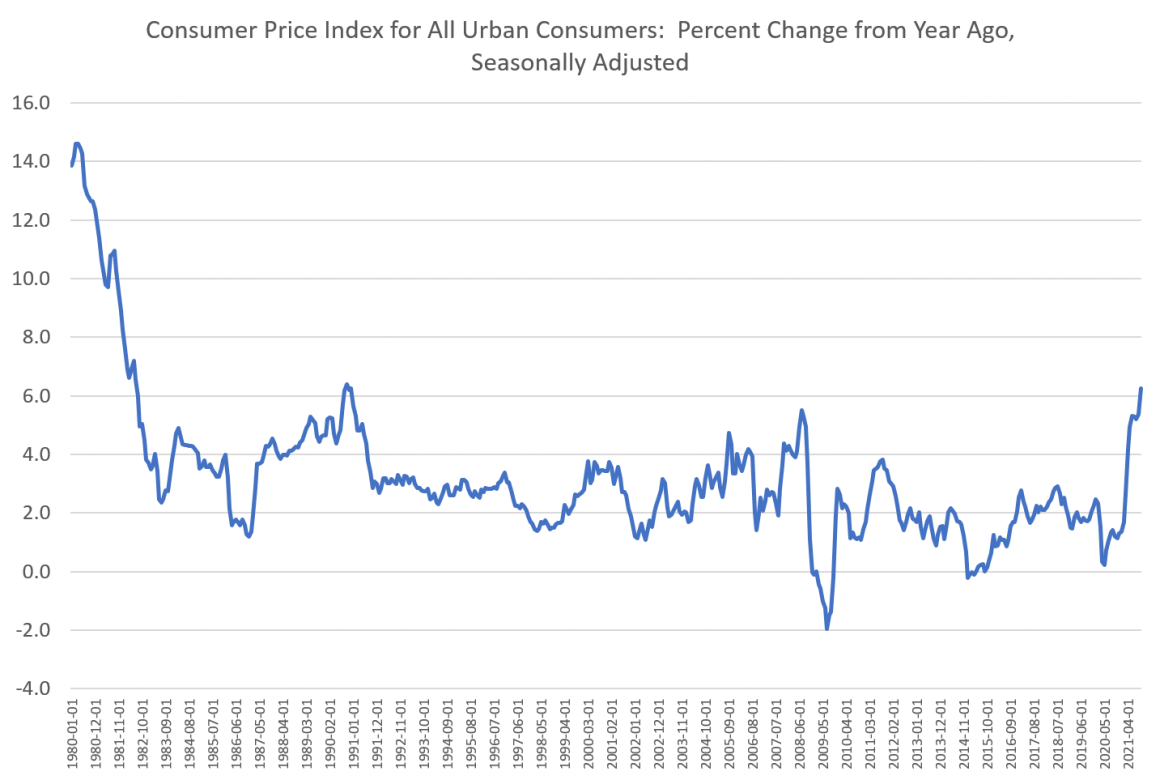

The Bureau of Labor Statistics reported Wednesday morning that prices rose 6.2% on a year-over-year basis in October. That’s the highest YOY rate since December 1990 when the CPI was also up 6.2 percent. October’s rate was up from 5.3 percent in September, and remains part of a surge in the index since February 2021 when year-over-year growth was still muted at 1.6 percent. Not surprisingly, producer prices surged in October as well. The producer price index for commodities in October was up 22.2 percent, year over year, reaching a 48-year high. We must go back to November 1974 to find a higher PPI increase—at 23.4 percent. Asset price inflation has naturally continued unabated at well, with the result being rising housing costs. In addition to the CPI’s 31-year

Topics:

Ryan McMaken considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| The Bureau of Labor Statistics reported Wednesday morning that prices rose 6.2% on a year-over-year basis in October. That’s the highest YOY rate since December 1990 when the CPI was also up 6.2 percent.

October’s rate was up from 5.3 percent in September, and remains part of a surge in the index since February 2021 when year-over-year growth was still muted at 1.6 percent. Not surprisingly, producer prices surged in October as well. The producer price index for commodities in October was up 22.2 percent, year over year, reaching a 48-year high. We must go back to November 1974 to find a higher PPI increase—at 23.4 percent. Asset price inflation has naturally continued unabated at well, with the result being rising housing costs. In addition to the CPI’s 31-year high, home prices in the second quarter surged near to a 42-year high. According to the Federal Housing Finance Agency’s home price index, home price growth reached 11.9 percent in the second quarter of this year. Since 1979, only the second quarter of 2005—also with 11.9 percent growth—showed home-price growth as high. This is troubling information indeed, given that average real weekly earnings have turned negative this year, with inflation-adjusted earnings down 0.5 percent from September to October. It is increasingly clear that wages are not keeping up with rising prices for a great many Americans. |

. |

None of this means policymakers will diagnose the problem properly, however. We should expect the discussion around inflation in Washington to keep missing the point and denying any connection to the central bank or to monetary inflation.

For example, rising prices are so obvious now that not even the administration can ignore them anymore. Today, the White House released a statement in which President Biden admitted: “… today’s report shows an increase over last month. Inflation hurts Americans pocketbooks”

Yet the administration continues to be very much in denial about the causes of price inflation. The Biden statement continues:

I have directed my National Economic Council to pursue means to try to further reduce these costs, and have asked the Federal Trade Commission to strike back at any market manipulation or price gouging in this sector.

As if “price gouging” were the cause of nationwide price inflation!

If it were “gouging,” we’d be seeing increases only in the areas where so-called gouging is taking place. Moreover, that would mean a decline in spending—and thus price deflation—in areas where the gouging isn’t taking place. The overall effect would be price stability.

Similarly, the administration has also tried to blame inflation on a lack of childcare. In an incoherent series of non sequiturs, Secretary of Transportation Peter Buttigieg this week claimed that paid family leave is “part of the administration’s tool kit to fight inflation.” Buttigieg simultaneously claimed that paid family leave means more people can take time off from work, and yet this somehow will also translate into more people going back to work. While it’s true more workers could help temper—to some extent—upward pressure on prices, more paid family leave would contribute nothing to this “solution” to price inflation. Rather, it’s apparent the memo went out at the administration that every policy must now be tied into some kind of plan to fight inflation—no matter how tenuous the connection.

Yet we should expect more of this sort of blind grasping at excuses for our economic malaise as time goes on. The same strategy was used by the Ford administration in the dark days of the mid1970s and the “Whip Inflation Now” campaign. The administration then claimed that the American public should fight inflation through strategies such as planting a vegetable garden at home.

Then, as now, the regime refused to admit that rising monetary inflation had anything to do with rising prices. Instead, we’re told it must be a lack of daycare services or “price gouging.”

A Second Strategy: Total Denial

But some in the administration are sticking to their narrative that there’s nothing at all to see here. Janet Yellen, for example, declared on Tuesday that “I’d expect price increases to level off, and we’ll go back to inflation that’s closer to the 2% that we consider normal.” She insists the Fed is very much in control of the situation and won’t allow 1970’s style inflation to occur.

What Yellen fails to mention is that even if inflation rates of, say, four to six percent, last only a year, middle class workers won’t make up these losses later just because inflation falls again at some point to “to the 2% that we consider normal.” After all, this year’s declines in real average weekly wages means real hardship for many people, even if Janet Yellen will be just fine with her private driver shuttling her from her luxury home to opulent cocktail parties all the while.

But not everyone is as uninterested in the effects of inflation as Janet Yellen. As MSNBC reports:

“For now, inflation is going to continue to run above very solid wage growth,” said Joseph LaVorgna, chief economist for the Americas at Natixis and former chief economist for the National Economic Council during the Trump administration. “This is why when you look at consumer confidence, it’s really taking a beating. Households do not like the inflation story, and rightly so.”

For at least one MSNBC columnist, though, people don’t know how good they have it. On Monday, James Surowiecki insisted everyone is better off and discussion of inflation amounts to little more than fear mongering. He writes:

… any discussion of inflation needs to include the context in which it’s happening. Historically, recessions have left Americans poorer, not better off. But the Covid recession was different. As people shifting their habits drastically in response to the pandemic, they spent much less and saved more. Even though millions of Americans lost their jobs, enhanced unemployment benefits and stimulus payments left many of them better off, not worse. And the stock market, after initially falling, boomed.

Surowiecki goes on to claim American consumers “are relatively speaking, flush” and high prices are nothing more than the result of the fact the economy is booming and everyone is getting so much richer so fast. He claims Americans are enjoying “robust wage growth” and are piling us savings in their bank accounts.

It’s difficult to guess what universe Surowiecki phoned in his column from, but it’s apparently not this universe where real wage growth is negative and the personal savings rate has collapsed over the past six months. It could be Surowiecki is just stuck in the past when new money was flooding into the economy, but prices had not yet adjusted to new monetary realities. Of course people felt richer back then. But that’s not where we are now.

Nonetheless, it is entirely possible that inflation rates could quickly turn downward again in coming months. That could occur if recession sets in with businesses and households unable to pay off their debts. If that happens, monetary deflation will set in and demand will decline, leading to a real drop in price inflation. Of course, that won’t exactly do wonders for real wages, either.

You Might Also Like

Why Worrying about Everything Is Bad Foreign Policy

Why Worrying about Everything Is Bad Foreign Policy

2021-10-10

The subtitle of John Mueller’s excellent new book suggests that something unusual is in store for the reader. If someone is called complacent, he is hardly being complimented; how then can there be a “case for complacency”? In brief, Mueller thinks that most of the threats and dangers that confront nations are really not that much to worry about, if they are not altogether imaginary.

How to Cheat with Cost-Benefit Analysis: Double Count the Benefits

How to Cheat with Cost-Benefit Analysis: Double Count the Benefits

2021-09-10

Because my economics courses focus on public policy, I often deal with benefit-cost analyses (BCA) in them. While little discussed, the central idea is simply to identify and include all the relevant benefits and costs of a decision, do our best to estimate their values, then choose the option that provides the greatest net benefits. Hardly a radical idea. It can be useful in disciplining our thinking to be more consistent. Benjamin Franklin employed a version of it.

The Terrible Economic Ignorance Behind Covid Tradeoffs: My Speech to the Ron Paul Institute

The Terrible Economic Ignorance Behind Covid Tradeoffs: My Speech to the Ron Paul Institute

2021-09-10

Some of you may know the name Alex Berenson, the former New York Times journalist who comes from a left-liberal background. He has been absolutely fearless and tireless on Twitter over the past eighteen months, documenting the overreach and folly of covid policy—and the mixed reality behind official assurances on everything from social distancing to masks to vaccine efficacy.

Separation Over Persuasion with Jeff Deist

Separation Over Persuasion with Jeff Deist

2021-09-09

My guest this week is the President of the Mises Institute, Jeff Deist. We discuss one of the biggest silver linings that can be taken from 2020 and the Covid moment. It’s time to take stock in what has happened and realize that getting a Rand Paul or a Thomas Massie elected at the Presidential level isn’t time and money well spent.

Bretton Woods and the Spoliation of Europe

Bretton Woods and the Spoliation of Europe

2021-08-20

Having marked the quinquagenary of the destruction of the gold standard Sunday, August 15, it is natural to be a little nostalgic for the Bretton Woods system. After all, it might not have been the classical gold standard, but at least it wasn’t as bad as the fiat standard that succeeded it.

Per Bylund on Sweden

Per Bylund on Sweden

2021-08-14

A major “Democratic Socialist” argument is to bring up Nordic countries. In this clip from Episode #69 Per Bylund explains the reality of Sweden and their economic system

“They Said What?!” John Lennon edition

“They Said What?!” John Lennon edition

2021-08-06

Bob unveils a new recurring series, in which he gives the context of infamous quotations. In this episode, he covers two allegedly shocking quotes from John Lennon, John Maynard Keynes’ "in the long run we’re all dead," Trump on Nazis being very fine people, Dan Quayle misspelling potato, Obama’s "you didn’t build that," and Bohm-Bawerk on Karl Marx.

Andrew Moran Evadé d’un tribunal anglais, arrêté en Espagne.

Andrew Moran Evadé d’un tribunal anglais, arrêté en Espagne.

2021-06-26

#Replay #Reportage #ReplayTv #belgium

#Police_Belge #Belgique #policebelges #France

#gendarmesfrançais #Gendarmes_français #Police

#100_jours avec #la_police #reportage,#reportage2021,#reportage_choc,#reportagem,#reportage_francais,

#reportage_complet,#reportage_comique,#reportage_documentaire,#documentaire,

#documentaire_français, #documentaire_politique, #reportage#complet_en_francais,

#reportage_complet_fr 2021 #nouveauté,#enquete_exclusive 2016, #francais,

#reportage_police,#drogue,#violence,#armée,#guerre,#enquete d’actualité,#cannabis, #magazine,#enquetes,#Enquete_EXclusive #Gendarmes,#Gendarmes2021,#cambrioleurs #reportages2021.

film telefilm complet en francais,

film telefilm thriller,

film telefilm complet en francais 2019,

film

Tags: Featured,newsletter