Fueled by unprecedented quantitative easing, central bank asset purchases, and various stimulus packages, the money supply growth rate ballooned in April to an all-time high. The growth rate has never been higher, with the 1970s as the only period that comes close. It was expected that money supply growth would surge in recent months. This usually happens in the wake of the early months of a recession or financial crisis. The magnitude of the growth rate, however, was unexpected. During April 2020, year-over-year (YOY) growth in the money supply was at 21.30 percent. That’s up from March’s rate of 11.3 percent, and up from April 2019’s rate of 1.94 percent. Historically, this is a very large surge in growth both month over month and year over year. It is also

Topics:

Ryan McMaken considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

RIA Team writes The Importance of Emergency Funds in Retirement Planning

Nachrichten Ticker - www.finanzen.ch writes Gesetzesvorschlag in Arizona: Wird Bitcoin bald zur Staatsreserve?

Nachrichten Ticker - www.finanzen.ch writes So bewegen sich Bitcoin & Co. heute

Nachrichten Ticker - www.finanzen.ch writes Aktueller Marktbericht zu Bitcoin & Co.

Fueled by unprecedented quantitative easing, central bank asset purchases, and various stimulus packages, the money supply growth rate ballooned in April to an all-time high. The growth rate has never been higher, with the 1970s as the only period that comes close. It was expected that money supply growth would surge in recent months. This usually happens in the wake of the early months of a recession or financial crisis. The magnitude of the growth rate, however, was unexpected.

|

During April 2020, year-over-year (YOY) growth in the money supply was at 21.30 percent. That’s up from March’s rate of 11.3 percent, and up from April 2019’s rate of 1.94 percent. Historically, this is a very large surge in growth both month over month and year over year. It is also quite a reversal from the trend that only just ended in August of last year, when growth rates were nearly bottoming out around 2 percent. In August, the growth rate hit a 120-month low, falling to the lowest growth rates we’d seen since 2007. The money supply metric used here—the “true” or Rothbard-Salerno money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2. The Mises Institute now offers regular updates on this metric and its growth. This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits, traveler’s checks, and retail money funds). The M2 growth rate also increased to historic highs in April, growing 18.01 percent compared to March’s growth rate of 10.95 percent. M2 grew 4.0 percent during April of last year. The M2 growth rate had fallen considerably from late 2016 to late 2018, but has been growing again in recent months. As of March, it is following the same trend as TMS. |

YoY Change in money supply, 1998-2019 - Click to enlarge |

| Money supply growth can often be a helpful measure of economic activity. During periods of economic boom, money supply tends to grow quickly as banks make more loans. Recessions, on the other hand, tend to be preceded by periods of slowdown in rates of money supply growth. However, money supply growth tends to grow out of its low-growth trough well before the onset of recession. As recession nears, the TMS growth rate climbs and becomes larger than the M2 growth rate. This occurred in the early months of the 2002 and the 2009 crises. February 2020 was the first month since late 2008 that the TMS growth rate climbed higher than the M2 growth rate. The TMS growth rate again exceeded M2 in March and April 2020. As of mid-April 2020, it does appear that the decline in money supply growth has again preceded a recession. Although some observers will likely claim that the current economic crisis is a result solely of the COVID-19 panic and resulting government-forced shutdowns, several indicators do suggests that the economy was primed for a recession. The decline in TMS is one of these indicators, as is the late 2019 liquidity crisis in the repo markets. The Fed’s moves to drop interest rates and to once again grow its balance sheet speak to the weakness of the economy leading up to April 2020.

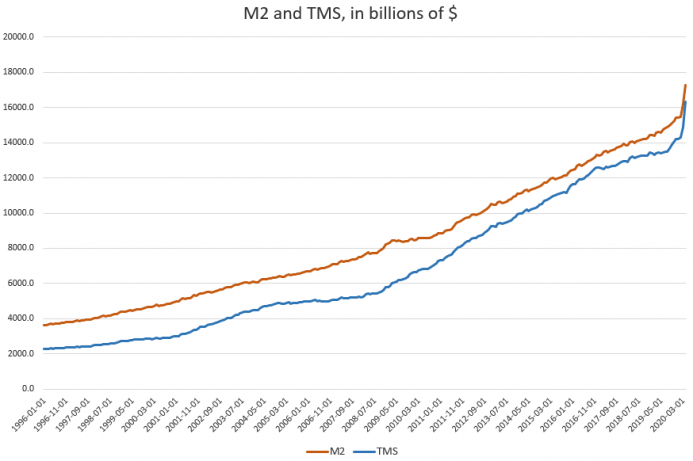

The overall M2 total money supply in February was $17.2 trillion and the TMS total was $16.3 trillion. |

M2 and TMS, in billions of $, 1996-2020 - Click to enlarge |

| The growth in the money supply in recent months is in part tied to the fact that the Federal Reserve grew more accommodative in late 2019 and embraced unprecedented monetary stimulus in March and April. The Fed drove down the target key interest rate to 0.25 percent and began broad and unprecedented new “quantitative easing” programs. The Federal Open Market Committee (FOMC) cut the target fed funds rate more than once in the months preceding March 2020, but in response to government-forced shutdowns of several sectors of the economy, it cut the federal funds rate by 150 basis points in less than a month. The Fed has flooded markets with new money by purchasing a variety of assets from US government debt to securities. The Fed’s balance sheet is now at an all-time high.

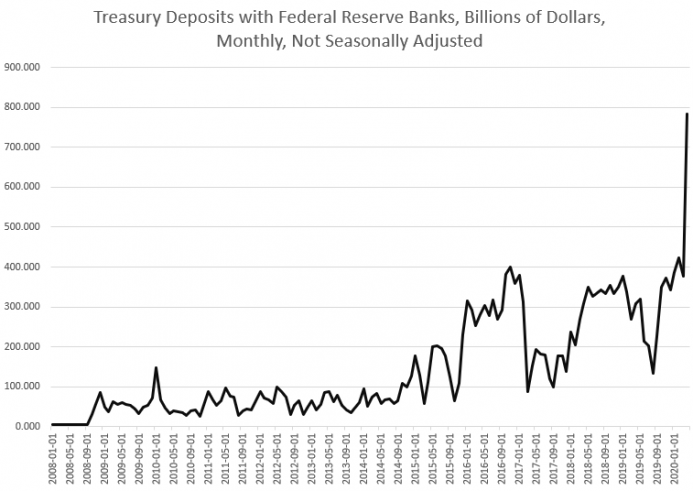

Another change partially driving the increase in the TMS is the large increase in Treasury deposits at the Fed that we’ve seen in recent months. In April 2020, this sum surged to a new all-time high of $783 billion. This is well in excess of the previous high of $423 billion reached during February of this year. |

Treasury Deposits with Federal Reserve Banks, 2008-2020 - Click to enlarge |

You Might Also Like

Crisis or Opportunity? To Politicians, It’s the Same Thing

Crisis or Opportunity? To Politicians, It’s the Same Thing

Forget performing William Shakespeare’s Macbeth. The real art form is politicking. They sport taxpayer-funded windbreakers, speak with authority and urgency, and lead a brigade of specialists. When a crisis unfolds, whether it is a hurricane or a virus outbreak, politicians stand before the cameras, appearing to be in control of the situation—but they see an opportunity.

How Bad Is It?

How Bad Is It?

How bad is it? That is the question on everyone’s mind as we come to grips with the economic carnage caused by global economic shutdowns, supply chain disruptions, and ongoing quarantines of million of people. Do we face another Great Depression, or simply a deep recession more like 2008? And equally important, are soft Americans prepared for either? Have we started to process all of this psychologically?

Ludwig von Mises & “Circulation Credit” Theory of the Trade Cycle

Ludwig von Mises & “Circulation Credit” Theory of the Trade Cycle

[This article is part of the Understanding Money Mechanics series, by Robert P. Murphy. The series will be published as a book in late 2020.] Starting with Carl Menger’s undisputed role in the “marginal revolution,” which ushered in subjective value theory, the Austrian school has made important contributions that have been absorbed into standard economic theory.

How Central Banks and Lockdowns Are Making the Crisis Worse

How Central Banks and Lockdowns Are Making the Crisis Worse

What typifies the phenomenon of the boom-bust cycle is that it is recurrent. What is the reason for this? Loose monetary policies set the platform for various activities that would not emerge without the easy monetary stance. What loose monetary policy does here is to engineer the transfer of real savings from wealth generating activities to artificially stimulated activities, which we can label as bubble activities.

How Words Like “Essential” and “Need” Are Abused by Politicians

How Words Like “Essential” and “Need” Are Abused by Politicians

Over the years, one of the most common trump cards used to justify government treating people differently, rather than equally, has been the word need. And when used to override individuals’ ownership of themselves and what they produce, its usage has created confusion rather than clarity. In public discussion, “need” has increasingly morphed into one of its synonyms—essential, as in “essential jobs.” But it still suffers from many of the same analytical problems.

How Modern Economics Has Lost Its Way: It’s All About the “Unseen”

How Modern Economics Has Lost Its Way: It’s All About the “Unseen”

Economics has lost its way and the study has become both impotent and lacking in relevance. It’s easy to see how and why once we recognize that proper economic thinking takes place two steps beyond the apparent. Noneconomists typically take none of these steps, while modern economics has lost the ability to go beyond the first.

Economics in Two Lessons: Why Markets Work So Well, and Why They Can Fail So Badly

Economics in Two Lessons: Why Markets Work So Well, and Why They Can Fail So Badly

Economics in Two Lessons: Why Markets Work So Well, and Why They Can Fail So BadlyJohn QuigginPrinceton: Princeton University Press, 2019xii + 390 pp. Abstract: John Quiggin’s Economics in Two Lessons alleges a failing in Henry Hazlitt’s Economics in One Lesson: the absence of a discussion of market failure.

Let’s Hope Deflation Is Headed Our Way

Let’s Hope Deflation Is Headed Our Way

The yearly growth rate of the US consumer price index (CPI) fell to 0.4 percent in April from 2 percent in April last year while the annual growth of the producer price index (PPI) plunged to –1.2 percent last month against 2.4 percent in April 2019.

Tags: Featured,newsletter