[Editor’s Note: this article is adapted from a 2003 essay in the Quarterly Journal of Austrian Economics entitled “New Keynesian Monetary Views: A Comment.” As economists abandon theory in favor of makeshift plans to flood the economy with stimulus, Hülsmann here provides some helpful reminders of the fundamental problems behind the current economic consensus on money.] The essential fallacy of John Maynard Keynes and his early disciples was to cultivate the monetary equivalent of alchemy. They believed that paper money was a suitable means to alleviate the fundamental economic problem of scarcity. The printing press was, at any rate, under certain plausible conditions of duress, a substitute for hard work, savings, and cutting prices (Hazlitt 1959, 1960). The

Topics:

Jörg Guido Hülsmann considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

[Editor’s Note: this article is adapted from a 2003 essay in the Quarterly Journal of Austrian Economics entitled “New Keynesian Monetary Views: A Comment.” As economists abandon theory in favor of makeshift plans to flood the economy with stimulus, Hülsmann here provides some helpful reminders of the fundamental problems behind the current economic consensus on money.]

The essential fallacy of John Maynard Keynes and his early disciples was to cultivate the monetary equivalent of alchemy. They believed that paper money was a suitable means to alleviate the fundamental economic problem of scarcity. The printing press was, at any rate, under certain plausible conditions of duress, a substitute for hard work, savings, and cutting prices (Hazlitt 1959, 1960).

The essential fallacy of John Maynard Keynes and his early disciples was to cultivate the monetary equivalent of alchemy. They believed that paper money was a suitable means to alleviate the fundamental economic problem of scarcity. The printing press was, at any rate, under certain plausible conditions of duress, a substitute for hard work, savings, and cutting prices (Hazlitt 1959, 1960).

The self-styled new Keynesians have not at all abandoned this fallacy, and they therefore do not differ in any essential respect from the old Keynesians, in spite of the pains they take to distinguish themselves from the latter. The new Keynesian recommendation for monetary policy is to “stabilize the growth of aggregate demand.” In plain language this means that the monetary authorities should never stop flooding the economy with paper money. This is recognizably the core tenet of the old Keynesian monetary program, which in itself had been nothing but even older fallacies clothed in the new language of aggregate analysis.

In many respects, new Keynesian views on monetary theory and policy seem to be even more fallacious than those of their predecessors. Whereas Keynes and his immediate followers were still trained in the old-fashioned art of economic reasoning, the new Keynesians are macroeconomic purebreds.1 Their expertise lies more or less exclusively in the field of modeling. As with the macroeconomics profession in general, they are devoted to a positivistic methodology, putting all their energies into modeling quantitative relationships among things that are the result of human action, rather than into the analysis of human action itself. Not surprisingly, therefore, their “science” of the economy resembles a hotchpotch of educated guesswork, conventions, and fictions, all designed to make the problems under consideration amenable to mathematical treatment. At one point in his exposition, Zimmermann briefly concludes that the optimal inflation rate should be zero. But then he goes on: “There is a consensus, however, that an inflation target between zero and two percent is optimal, allowing for measurement errors” (Zimmermann 2003, p. 7). Those who are bewildered by such turns of argument might also wonder how one can believe that policy recommendations derived from a mere consensus of academic economists have anything to do with science. Similar problems crop up with the frequent jumps between statements of facts and value judgments, and to new Keynesian uses of expressions such as “principles,” “first principles,” and so on. In the writings of Austrian economists these words have a completely different meaning.

Honest new Keynesians acknowledge that their models are not a realistic representation of parts of the observed economy. They admit that their reasoning is based on stipulations and conventions of a more or less fictional and therefore arbitrary character. But they believe that economic science cannot do any better than that, whereas Austrians think they know a better approach. As a consequence, from an Austrian perspective, new Keynesian policy prescriptions do not exactly stand on the firm ground of science. For example, is it really true that central bankers are supposed to be well-meaning economic tsars? And is it really true that central bankers seek to minimize deviations of output from potential output? More importantly still, even if we assume for the sake of argument that both of these questions can be answered in the affirmative, we still have still not even touched the fundamental problems of monetary policy analysis—problems that require sober examination before one can venture to make any “scientific” recommendations to policymakers? Here is one for a starter: How can central bankers, or for that matter anybody else, know the potential output of an economy at any point in time? And also: Can monetary policy close the gap between actual and potential output at all? Again the sober observer cannot fail to notice that new Keynesians have no genuine answers to these questions—they answer them (in the affirmative) by stipulation and by convention.

More to the point of monetary theory and policy, Austrian economists certainly agree with the commonplace [notion] that money is not neutral in the short run. But they would add that money is never neutral, neither in the short nor in the long run, because of the wealth effects that go in hand with any change in the money supply. Monetary policy therefore always has an impact on the economy, irrespective of whether the policy has been anticipated.2 Its impact on prices is not necessarily proportional, but in any case it permanently alters the distribution of wealth among the members of society and thereby affects the prices paid for the various consumer’s goods and producer’s goods. It makes some ventures profitable, and it makes other ventures unprofitable. It creates fortunes and elevated social positions on the one hand, and it destroys wealth and income on the other.

The fundamental question we have to confront in the theory of monetary policy is therefore not whether money affects the real economy—yes, it does, both in the short run and in the long run—but whether changes of the money supply can make society better off in the aggregate. Austrian economists who follow the approach of Mises and Rothbard believe that it cannot. By contrast, the intellectual edifice of Keynesianism—both old and new—rests squarely on the notion that money does alleviate the problem of scarcity for society as a whole. The entire case for monetary policy is based on the idea that “a decrease of inflation is followed by temporary output losses” (Zimmermann 2003, p. 6). At least in the short run, there is a tradeoff between inflation and unemployment.

But why should we believe that such a tradeoff is more than an accident of history—that is, why should we not believe that a decrease in inflation could with equal probability lead to temporary output gains ? At this point the new Keynesians essentially repeat the arguments of their predecessors, referring to sticky prices, the Phillips curve, and discontinuous price setting. But the Phillips curve at the very best is the statistical representation of contingent historical data (Phillips 1958; Fisher 1973). And even if we grant for the sake of argument that it faithfully represents certain historically contingent data, the fact remains that stickiness of prices is no fact of nature such as rainy weather or sunshine, but a variable that depends on political and cultural factors. On a free market, price stickiness is always as low as it can humanly be, and no monetary policy can reduce it further—as long as labor unions can hire economists trained in (new and old) Keynesian economics, at any rate (Mises 1931, 1958; Friedman 1968).

Similarly, there is no reason to assume that staggered nominal price setting per se induces disequilibria—”fluctuations in output” and “macroeconomic inefficiencies.” Contracts are always made for certain periods of time. In more or less many cases, one of the contracting parties may discover after the fact that the price stipulated in the contract was not adequate from his point of view. But how can this be said to be a general social problem? After all, the other party usually gains in such a situation, and thus there is no general problem. Most importantly, however, it is not at all clear how such problems can possibly be avoided or reduced through manipulations of the money supply. Is it really necessary to repeat all the insights about expectations and the dangers of inflation-induced moral hazard—insights that seem to have made it into large parts of the mainstream these past thirty years?

A final word on the Taylor principle: it does not rule out inflation spirals. Under certain conditions it is not enough to increase interest rates overproportionally, because even such an overproportional increase might not be sufficient to offset the other factors that cause an increase in the price level. These conditions seem to hold in many cases (Orphanides 2000). Moreover, and more importantly, the entire focus on inflation targeting and interest rate targeting in particular is misleading, as Austrians have long been arguing, because bubbles can build up even at stable prices and interest rates.3

Monetary theorists are well advised to regain the habit of discussing policy questions at a fundamental institutional level. It is relevant and useful to raise the question of whether we need central banks at all, and why. And it is relevant and useful to compare free market money with fiat money. Eclipsing such questions from the very outset might be convenient for those who derive income from the present institutions. But it is a disserve to science, and to society as a whole.

References

Barro, R.J. 1976. “Rational Expectations and the Role of Monetary Policy.” Journal of Monetary Economics 2: 1–32.

Borio, Claudio, and Philip Lowe. 2002. “Asset Prices, Financial and Monetary Stability: Exploring the Nexus.” Working paper no. 114, Bank for International Settlements, Basle, July 2002.

Clarida, Richard, Jordi Galí, and Mark Gertler. 1999. “The Science of Monetary Policy: A New Keynesian Perspective.” Journal of Economic Literature 37.

Fisher, Irving. 1926. “A Statistical Relation between Unemployment and Price Changes.” International Labour Review 13, no 6. Reprinted as “I Discovered the Phillips Curve.” Journal of Political Economy 81 (1973).

Friedman, Milton. 1968. “The Role of Monetary Policy.” American Economic Review 58: 1–17.

Hayek, Friedrich A. 1931. Prices and Production. London: Routledge and Sons.

Hazlitt, Henry, ed. 1960. The Critics of Keynesian Economics. Princeton, NJ: D. Van Nostrand.

———. 1959. The Failure of the “New Economics.” Princeton, NJ: D. Van Nostrand.

Keynes, John Maynard. 1924. Tract on Monetary Reform. New York: Harcourt, Brace.

———. 1971. Indian Currency and Finance. New York: Franklin.

Lucas, R.E. 1975. “An Equilibrium Model of the Business Cycle.” Journal of Political Economy 83: 1113–144.

McCallum, B.T. 1980. “Rational Expectations and Macroeconomic Stabilisation Policy: An Overview.” Journal of Money, Credit and Banking 12: 716–46.

Mises, Ludwig von. 1998. Human Action. Scholar’s ed. Auburn, AL.: Ludwig von Mises Institute.

———. 1958. “Wages, Unemployment, and Inflation.” In Planning for Freedom. South Holland, IL: Libertarian Press.

———. 1931. Ursachen der Wirtscheftskrise. Tübingen: Mohr.

Orphanides, Athanasios. 2000. “Activist Stabilisation Policy and Inflation: The Taylor Rule in the 1970s.” Working paper no. 2000–13, Board of Governors of the Federal Reserve System,Washington, DC.

Patinkin, Don 1965. Money, Interest, and Prices. 2d ed. New York: Harper and Row.

Phillips, A.W. 1958. “Relationships Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1862–1957.” Economica 25: 283–99.

- 1. Clarida, Galí, and Gertler (1999, p. 1662) state that new Keynesians reclaim the Keynesian heritage insofar as they focus on the economic implications of temporary nominal price rigidities and that they are “new” Keynesians to the extent that they rely on more recent methodological advances in macroeconomic modeling, especially those developed in real business cycle theory. Compare this with the early (“pre-Keynesian”) Keynes (1924, 1971).

- 2. This is one of the important points of departure between Austrian economists and their colleagues from the monetarist/real business cycle camp. Both groups believe that the anticipations of market participants can neutralize monetary policy in many respects. For example, if labor unions anticipate inflationary policies, the latter will not reduce unemployment. But the monetarists overstate the role of expectations to the extent that they claim that anticipations nullify any real effects of monetary policy. In their view of the long run, only unanticipated changes of the money supply can have real effects. But this opinion is fallacious because of the existence of wealth effects. For the monetarist position, see Patinkin (1965, esp. pp. 50ff.); Barro (1976, pp. 1–32); Lucas (1975, pp. 1113–144); McCallum (1980, pp. 716–46). For a discussion of neutral money from an Austrian point of view, see Mises (1998, pp. 538–40).

- 3. See Hayek (1931), for example. This insight has made it into mainstream analyses of the current crisis; see, for example, Borio and Lowe (2002).

You Might Also Like

The Search for Yield

The Search for Yield

A no-holds-barred discussion of the economy after the coronavirus shutdown and George Floyd protests. Are we facing another Great Depression? Can there be a V-shaped recovery or is this wishful thinking? What will all the new money and credit created by Congress and the Fed mean for the dollar? What kind of economic mess will Trump or Biden inherit in 2021? How far will Fed chair Powell go to keep markets propped up?

Economic Collapse Has Turned Many Europeans against the EU

Economic Collapse Has Turned Many Europeans against the EU

Since the beginning of the year, the corona crisis has monopolized news coverage to the extent that a lot of very important stories and developments either went underreported or were ignored altogether. One such example was the very surprising ruling that came out of the German Constitutional Court in early May, which challenged the actions and remit of the European Central Bank (ECB).

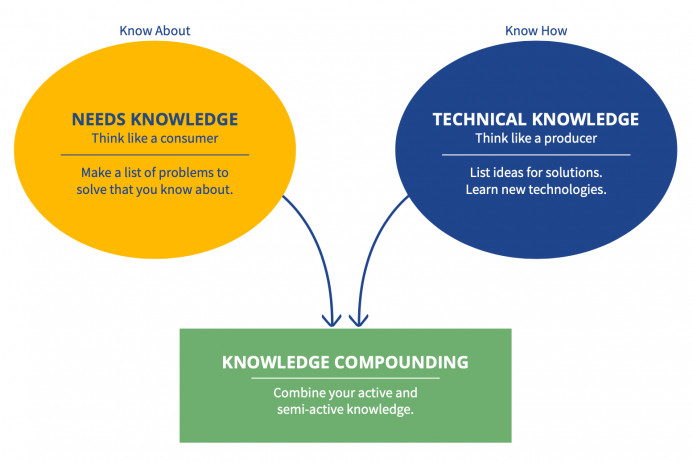

Mark Packard’s Value Learning Process: The Two Kinds of Knowledge Entrepreneurs Must Have

Mark Packard’s Value Learning Process: The Two Kinds of Knowledge Entrepreneurs Must Have

Key Takeaways and Actionable Insights. Innovation is one of the keys to business success. The world is changing at such a pace, and your customers’ preferences are changing so fast, that your business has to change at the same speed, or even faster. How to keep up is a part of the entrepreneurial challenge.

The Great Society: A Lesson in American Central Planning

The Great Society: A Lesson in American Central Planning

Most people associate the Great Society initiative with Lyndon Baines Johnson. There is very good reason for that, to be sure. As president, Johnson, the “master of the Senate,” was the driving force behind the raft of legislation that passed during his administration, the 1964 and 1965 legislation that framed and filled in his vision for a “great society” in which the blessings of postwar America’s bonanza would be shared by all.

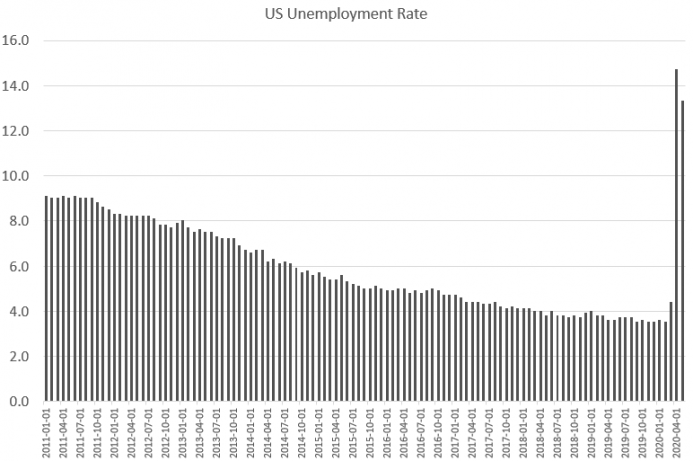

The Employment Situation Is Still a Disaster

The Employment Situation Is Still a Disaster

Last Friday, the US Bureau of Labor Statistics released new unemployment data. The report surprised many because it showed a decrease in the unemployment rate, while many observers had expected an increase.

The Scandinavian Model Won’t Work in Chile

The Scandinavian Model Won’t Work in Chile

Scandinavian welfare states continue to allure leftist onlookers across the world. The Nordic welfare model is marketed as a humane alternative to the cutthroat nature of Western capitalism. It received a massive boost when Vermont senator Bernie Sanders campaigned on emulating these countries in both of his presidential runs during 2016 and 2020.

Keynesians on the Cause of, and Cure for, Depressions

Keynesians on the Cause of, and Cure for, Depressions

[This article is part of the Understanding Money Mechanics series, by Robert P. Murphy. The series will be published as a book in late 2020.] In chapter 8 we presented Ludwig von Mises’s explanation of how bank credit expansion causes the boom-bust cycle, what is now known as Austrian business cycle theory. However, the reigning view today in both academia and the popular media is the Keynesian explanation, derived from John Maynard Keynes’s famous 1936 book The General Theory.

Inequality is Overstated—and Overrated

Inequality is Overstated—and Overrated

Whining and complaining about inequality is a growth industry. Thomas Piketty’s book (or perhaps a large virtue-signaling paperweight), about how the rich are getting richer, achieved bestseller status and is now a movie. Understanding the flaws in the wealth inequality argument is increasingly important, because the communist wing of the Democratic Party is now openly advocating a wealth tax.

Tags: Featured,newsletter