“The sky is falling. The sky is falling,” they cried, as equities plunged in December. It is signaling a recession, we were told. Instead, global equities have begun the year with a strong advance. The S&P 500 gapped higher ahead of the weekend, extending this year’s rally to about 14%. It has now retraced more than 50% of the decline, not from the December high but from the record high in late September. It has rallied for four consecutive weeks. The Dow Jones Stoxx 600 gapped higher before the weekend and above a downtrend in place since September. It also appreciated for three consecutive weeks, retracing more than a third of last year’s decline. The MSCI Emerging Markets Index posted a third weekly advance and

Topics:

Marc Chandler considers the following as important: 4) FX Trends, EUR, Featured, Federal Reserve, GBP, JPY, newsletter, SPX, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

“The sky is falling. The sky is falling,” they cried, as equities plunged in December. It is signaling a recession, we were told. Instead, global equities have begun the year with a strong advance. The S&P 500 gapped higher ahead of the weekend, extending this year’s rally to about 14%. It has now retraced more than 50% of the decline, not from the December high but from the record high in late September. It has rallied for four consecutive weeks. The Dow Jones Stoxx 600 gapped higher before the weekend and above a downtrend in place since September. It also appreciated for three consecutive weeks, retracing more than a third of last year’s decline. The MSCI Emerging Markets Index posted a third weekly advance and its highest weekly close since last September.

Sentiment can swing wildly, and short-term price action does not make for the basis for policy. The Fed has been chastened for not listening to the market as if it not as temporally inconsistent as policymakers. The fixed income market isn’t better. The two-year yield reached the cyclical high in early November just shy of 3%. It fell 2.36% at the start of the year, which is a few basis points below the average effective Fed funds rate. It recovered to 2.60% ahead of the weekend.

While Powell appears to have struck the right tone with the patience and flexibility mantra, the July Fed funds futures contract has gone from pricing in nearly a 50% chance of a cut to about a 40% chance of a hike in H1. It is not that the capital markets don’t generate useful signals, but the signals require a context and a judgment.

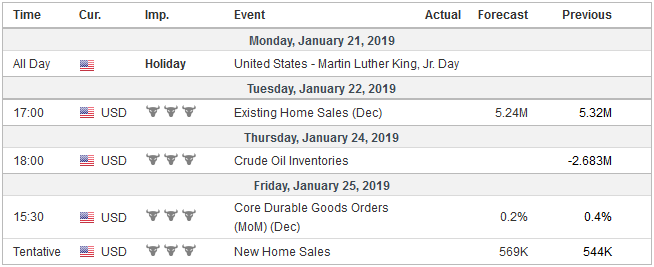

United StatesThe US economy has clearly slowed from the surge in Q2 18 and Q3 18, but the recent string of data shows little sign of an economy on the verge of a recession beginning with the employment data and services PMI to start the December data series. The regional Fed manufacturing surveys have been mixed, and the Philly Fed’s survey reported last week jumped. Weekly initial jobless claims eased more than expected. Manufacturing output jump 1.1% in December, and the takeaway here is that sentiment indicators were weaker than the actual performance. Another important point is that divergence, which we argue is a key driver for the dollar, is very much alive. Consider that in December, US industrial output was up 4% year-over-year. In the eurozone, it was 1.7% lower year-over-year in November, while the UK’s was 1.5% lower. Japan’s was 1.5% higher. |

Economic Events: United States, Week January 21 - Click to enlarge |

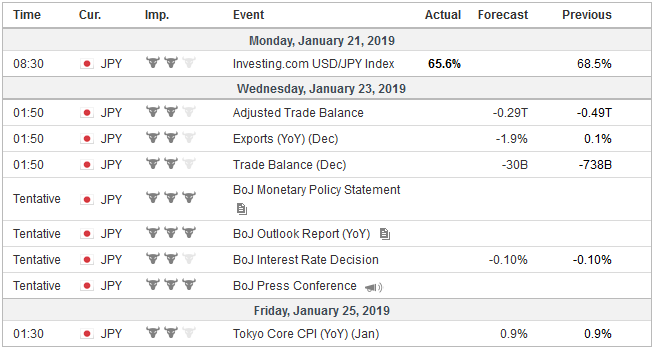

JapanNext week may push the divergence theme further. The BOJ and ECB meet. At the end of last week, Japan reported that December core CPI, which excludes fresh food and is the measure the BOJ targets slowed to 0.7% from 0.9%. Excluding both fresh food and energy, and the prices rose 0.3% year-over-year. There is some speculation that the BOJ could shave its inflation forecast. If it does, it would be seen as dovish, and perhaps trying to encourage a further unwinding of the yen’s recent gains, seemingly unrelated to macroeconomic developments. Japanese businesses and officials are more comfortable with the dollar above JPY110, but the bar to intervention is very high. Meanwhile, as the yen pulls back, the 10-year JGB yield may continue to recover after falling to negative five basis points at the start of the month. |

Economic Events: Japan, Week January 21 - Click to enlarge |

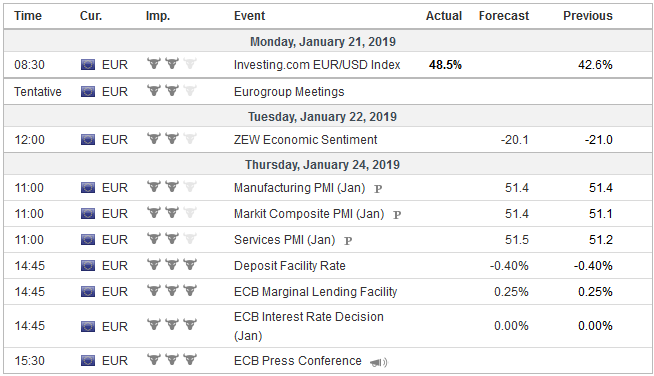

EurozoneA few hours before the ECB’s statement, the flash Markit PMIs will be reported. Economists no less than policymakers have been surprised by the weakness in Europe. The composite PMI fell in the last four months of last year. It may be difficult to see how this can happen with negative interest rates, and economists look for signals of the European aggregate demand coming in the service PMI, which is expected to tick up, while the manufacturing sector may stay soft as trade tensions and the global economic slowdown bites. The ECB’s bond-buying program has ended. There has been no noticeable market impact. Much ink was spilled debating who would buy Italian bonds but last week’s auction was oversubscribed. Peripheral benchmark premiums over Germany have narrowed at the start of the year. The challenge has shifted from managing the huge and complicated due to the Eurosystem’s structure bond-buying program to responding to the incoming data. Draghi’s speech last week to the European Parliament likely foretells the thrust of the press conference. The ECB itself seems divided, narrowly enough for the collegiate culture, that this strange creature that is neither fish nor fowl. Risks are broadly balanced but are rising to the downside. Satisficed. A rise in the composite PMI would work in Draghi’s favor, but the pressure to be credible may require a stronger comment if it falls for the fifth consecutive month. Maybe the bet is that the German auto sector will recover before the staff shaves its forecasts in March. Draghi leans heavy on the strength of the labor market. Weakness in the coming months could have a disproportionate market impact. The hawks want to wait for March and the new staff forecasts to reassess the guidance. Acknowledging that the balance of risks has shifted to the downside would seemingly require a response. Last week, Draghi warned even if the growth slowdown last longer than previously appreciated, it does not necessarily mean a recession. He may be pressed a bit more on the kind of conditions that would prompt the central bank to offer a new round of long-term refinancing operations, which we expect to be announced near mid-year. |

Economic Events: Eurozone, Week January 21 - Click to enlarge |

United KingdomThe Brexit drama enters a new act next week, and the tension builds to the next climax the following week when the House of Commons will vote on the Plan B that Prime Minister May will propose on January 21. She ruled out the idea of a remaining in the single market, though the DUP who is responsible for ensuring that she survived the vote of confidence, would consider for limiting the backstop. It is difficult to see how any alternative to the negotiated Withdrawal Bill would allow for an orderly exit at the end of March. After May survived the vote of confidence, sterling rallied to two-month highs against the euro and the dollar (~GBP0.8765 and $1.30 respectively). The near-term risk-reward may have turned. A postponement of the divorce has already helped fuel sterling’s recent gains. A softer rather than harder exit appears necessary to cobble a majority. In some ways, until the Parliament’s vote on Plan B, there is little reason to chase the sterling higher these drivers. There were some ideas that meltdown in the stock market last month spurred more interest by the Trump Administration for a trade deal with China. Two stories emerged last week that fanned hopes of a favorable resolution. First was the press report that there was a discussion of US tactics ahead of China’s Vice Premier’s visit to Washington at the end of January to talk trade. The who said what and when is less material that noting that Treasury is still pushing for a more amicable approach. However, it seems to have consistently been outmaneuvered by the more nationalist wing. |

Economic Events: United Kingdom, Week January 21 - Click to enlarge |

ChinaSecond, China reportedly offered a plan to eliminate its trade surplus with the US in six-year by increasing its imports from the US by as much as $45 bln this year and increasing going forward. Reports indicated the US negotiators pushed back and wanted this achieved by 2020. A similar plan was previously rejected by Trump. The recovery in the stock market may remove some sense of urgency, and the best deal cannot be announced after the first round of talks. An increase market share conceded to US businesses must come at the expense of another country. Imports from the US would rise faster than overall imports. At the start of the 20th century, the US defend the territorial integrity of China against the Old World imperialists carving it up into spheres of influence. The long-term interest was to encourage an Open Door for investment and trade in all China. Then it was over territories and now if some version is agreed, would be over shares of China’s import market. |

Economic Events: China, Week January 21 - Click to enlarge |

The domestic US political drama about the role of Russia in the 2016 election has not been a factor that influenced the capital markets. However, the situation appears to be escalating. Recent developments include what appears to be the Trump campaign shared polling information with Russian operative. Reports suggest that he told his “fixer” Cohen to lie to Congress, but in an unusual move the Special counsel investigator’s office commented on such talk to deny it. Cohen will testify before Congress on February 7.

It will occupy an increasing amount of Trump’s time. As the legislature’s committees begin their work, the Administration may be pressed by the House of Representatives in a way it wasn’t over the past two years. The government’s partial shutdown is increasingly disruptive, and a majority blame him than the Democrats. Early March, when the debt ceiling will be reached, is the next key date. It is not a drop-dead date, as the Treasury has a several-month workaround, including more bill issuance, which in turn adds upward pressure on short-term rates amid concern about curve-inversion. Some suspect that this backdrop may encourage the willingness to get wins or dramatic moves that overshadow the poor domestic news.

Tags: #GBP,#USD,$EUR,$JPY,Featured,Federal Reserve,newsletter,SPX