Summary:

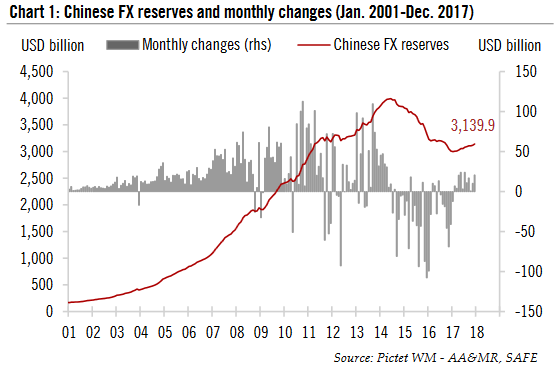

According to the Chinese State Administration of Foreign Exchange (SAFE), China’s FX reserves amounted to USD3.14 trillion at end – December 2017, up USD20.7 billion from the previous month. This marks the 11th consecutive monthly increase in Chinese FX reserves since February 2017. In full – year 2017, Chinese FX reserves increased by USD129.4 billion, in contrast with a drop of USD512.7 billion in 2015 and USD320 billion in 2016. (Chart 1). Chinese FX Reserves and monthly changes, 2001 - 2018 - Click to enlarge According to our estimates, China’s trade surplus likely contributed most to the increase in the FX reserves in December, to the tune of roughly USD19 billion. As part of Chinese FX reserves are in non

Topics:

Dong Chen considers the following as important: Chinese capital flows, Chinese economy, Chinese FX reserves, Chinese investment, Featured, Macroview, newslettersent, Pictet Macro Analysis, Swiss and European Macro

This could be interesting, too:

According to the Chinese State Administration of Foreign Exchange (SAFE), China’s FX reserves amounted to USD3.14 trillion at end – December 2017, up USD20.7 billion from the previous month. This marks the 11th consecutive monthly increase in Chinese FX reserves since February 2017. In full – year 2017, Chinese FX reserves increased by USD129.4 billion, in contrast with a drop of USD512.7 billion in 2015 and USD320 billion in 2016. (Chart 1). Chinese FX Reserves and monthly changes, 2001 - 2018 - Click to enlarge According to our estimates, China’s trade surplus likely contributed most to the increase in the FX reserves in December, to the tune of roughly USD19 billion. As part of Chinese FX reserves are in non

Topics:

Dong Chen considers the following as important: Chinese capital flows, Chinese economy, Chinese FX reserves, Chinese investment, Featured, Macroview, newslettersent, Pictet Macro Analysis, Swiss and European Macro

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

| According to the Chinese State Administration of Foreign Exchange (SAFE), China’s FX reserves amounted to USD3.14 trillion at end – December 2017, up USD20.7 billion from the previous month. This marks the 11th consecutive monthly increase in Chinese FX reserves since February 2017. In full – year 2017, Chinese FX reserves increased by USD129.4 billion, in contrast with a drop of USD512.7 billion in 2015 and USD320 billion in 2016. (Chart 1). |

Chinese FX Reserves and monthly changes, 2001 - 2018 - Click to enlarge |

|

According to our estimates, China’s trade surplus likely contributed most to the increase in the FX reserves in December, to the tune of roughly USD19 billion. As part of Chinese FX reserves are in non – USD currencies (such as the euro and British sterling etc.), the decline in the US dollar increases Chinese FX reserves reported in dollar terms. In December, the US dollar index dropped by 0.8%, which, according to our estimate, may have had the effect of boosting Chinese FX reserves by nearly USD9 billion. By contrast, changes in the value of the Chinese government’s holdings of US Treasury bonds and capital flow jointly may have depressed Chinese FX reserves by USD7.6 billion in the same month.

After the massive outflows of capital in Q3 2015 – Q1 2016 that followed China’s devaluation of its currency in August 2015, capital outlows abated quite significantly. We estimate that the total capital outflow from China in 2017 amounted to USD166 billion, compared to USD500 billion in 2016 and USD761 billion in 2015. In 2017, there were three months in which China actually posted net capital inflows, a phenomenon not observed since Q2 2014 (Chart 2).

|

Estimated net capital flows across Chinese border, Jan 2014 - Dec 2017 - Click to enlarge |

|

In our view, the decline in capital outflows primarly reflects the effectiveness of strengthened capital controls over the past two years. Measures have included cracking down on underground money transfers, restricting large overseas M&A by Chinese corporations and fixing various loopholes in the capital account transactions (such as buying investment – type insurance policies in Hong Kong using UnionPay bank cards issued in mainland China).

Importantly, however, the decline in capital outflows may also suggest that domestic and foreign investors’ sentiment towards China is improving.

In the first three quarters of 2017, the Chinese economy expanded by 6.9% year – over – year (y-o-y), and very likely managed full – year growth of 6.8%, significantly above the consensus forecast at the start of the year. The perceived risk of a hard landing has dropped substantially.

In the wake of the Communist Party’s 19th Congress in October, the Chinese government has made reducing financial risks one of its top priorities. More regulations have been introduced to crack down on shadow banking and to lower leverage in the financial system. Also, the government’s aggressive push to cut excess capacity in heavy industries such as steel making and coal mining is showing some initial signs of success. Thanks to the measures undertaken, and helped by the surge in nominal GDP, the debt-to-GDP ratio showed signs of stabilisation in 2017.

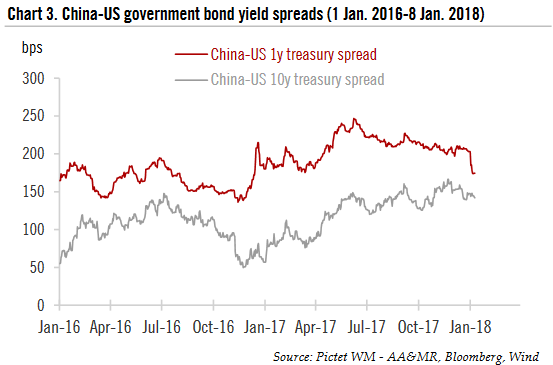

As the Chinese monetary authorities have tightened up controls on the financial sector, interest rates have risen significantly. As a result, the interest rate differential between China and the US has widened, especially at the long end. For example, the Chinese 10-year government bond yield spread over its US counterpart at 8 January 2018 was 142 basis points (bps), substantially higher than the low point of 50 bps reached at the end of November 2016. At the short end, the spread has also widened, although the gap has shrunken again since the second half of 2017 (Chart 3).

|

China - US government bond yield spreads, Jan 2016 - 2018 - Click to enlarge |

|

Rising interest rates and widening yield differentials have contributed to the Chinese yuan’s appreciation of over 6% against the dollar in 2017, one of the biggest surprises of the year, which, in turn, led to a significant improvement in sentiment. Concerns about another round of currency devaluation by the Chinese government seems to have largely dissipated.

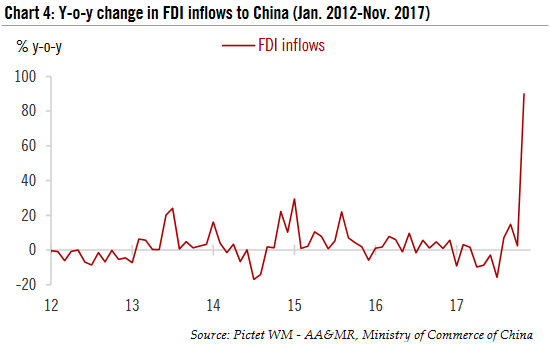

The recent surge in foreign direct investment (FDI) to China is another sign of improving sentiment. After declining on an y-o-y basis for four consecutive months, FDI to China started to pick up in August 2017. In November, the monthly inflow amounted to USD18.8 billion, the highest since data were first made available in late 2002, and 90% higher than a year before (Chart 4).

|

Y - o - y change in FDI inflow s to China , Jan 2012 - Nov 2017 - Click to enlarge |

Note that it’s quite possible that not all of the fund inflow s that fall under the category of FDI actually involve real investments. Some could be portfolio investments disguised as FDI to circumvent the restrictions on accessing China’s capital markets, which are still only partially open to foreign investors. But this still means that foreign investors are starting to become more bullish about China.

Tags: Chinese capital flows,Chinese economy,Chinese FX reserves,Chinese investment,Featured,Macroview,newslettersent